With subprime auto loan delinquency rates hitting a 32-year record of 6.9% in early 2026, the traditional wait and see approach to collections is officially dead. You’re likely feeling the pressure of rising defaults and the constant headache of manual insurance tracking that leads to costly errors. It’s frustrating to watch your portfolio health decline while your staff spends hours chasing missed payments through inconsistent, manual outreach. We understand that in this volatile economy, you need more than just a bigger team; you need a smarter system.

This guide will show you exactly how to transform your recovery rates by improving collection efficiency auto loans through strategic automation and real-time visibility. You’ll discover how integrating automated communication and proactive risk management into your workflow can lower delinquency rates without increasing your overhead. We’ll explore how to leverage tools like Verifacto LMS and automated insurance tracking to move from reactive chasing to a streamlined, data-driven operation that keeps your portfolio secure and your staff focused on high-priority accounts.

Key Takeaways

- Move beyond manual “dialing for dollars” by adopting data-driven prioritization that focuses your team on high-value accounts.

- Utilize automated multi-channel workflows to ensure consistent borrower communication and reduce the risk of missed payment windows.

- Recognize why real-time insurance tracking is a vital leading indicator of borrower risk and how it prevents avoidable defaults.

- Implement a modern strategy for improving collection efficiency auto loans by integrating automated reminders and built-in payment processing.

- Audit your current lending workflow to identify operational bottlenecks and replace manual tracking with streamlined, digital-first recovery tools.

The State of Auto Loan Collections in 2026

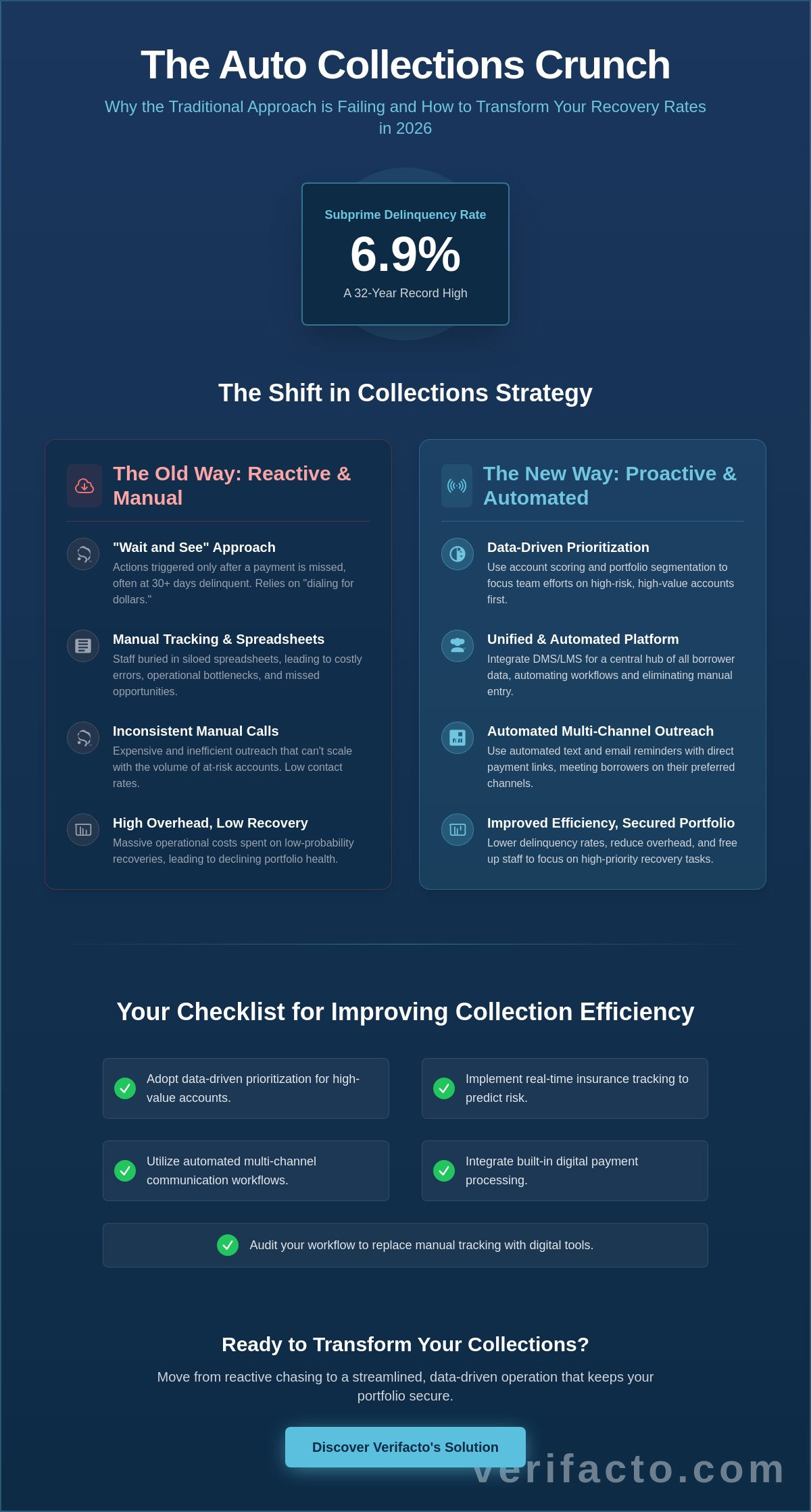

The auto lending landscape has reached a critical tipping point. In early 2026, subprime auto loan delinquency rates hit 6.9%, a 32-year high that surpasses even the peak of the Great Recession. This isn’t just a statistic; it’s a “collections crunch” that’s forcing lenders to rethink their entire recovery model. If you’re still relying on manual tracking and “dialing for dollars,” you’re fighting a losing battle against math and time. Success in this environment requires a shift toward improving collection efficiency auto loans by replacing outdated, reactive habits with proactive, data-driven systems.

Traditional methods are failing because they can’t scale with the current volume of at-risk accounts. Lenders often struggle with understanding the debt collection process as it evolves under new regulations and shifting consumer behaviors. Relying on staff to manually call every past-due borrower is expensive and inefficient. The real cost of inefficiency isn’t just the charge-off itself; it’s the massive operational overhead spent on low-probability recoveries. When your team is buried in spreadsheets, they can’t focus on the high-priority accounts that actually impact your bottom line.

The Impact of Economic Volatility on Auto Portfolios

Inflation and high interest rates, with the average 60-month new car loan rate sitting at 7.04% as of May 2026, have squeezed borrower budgets to the limit. As vehicle prices stabilize or dip, many borrowers find themselves in “underwater” loans where they owe more than the car is worth. This creates a dangerous correlation between negative equity and default probability. To protect your portfolio, you must identify “at-risk” segments before they miss that first payment. This means looking at real-time data rather than waiting for a 30-day delinquency notice to trigger action.

Why Digital Transformation is No Longer Optional

Today’s borrowers are mobile-first and expect seamless, digital interactions. They don’t want a phone call during dinner; they want a text reminder with a direct link to pay. Moving away from siloed spreadsheets to unified cloud platforms is the only way to maintain control. The role of an integrated DMS and LMS is vital here. It streamlines data flow, ensuring that payment history, insurance status, and communication logs are all in one place. By improving collection efficiency auto loans through digital transformation, you eliminate the friction that leads to missed payment windows and unnecessary defaults.

Data-Driven Strategies: The Foundation of Efficiency

Data isn’t just a byproduct of your lending; it’s the fuel for improving collection efficiency auto loans. In a market where delinquencies are climbing, you can’t afford to treat every past-due account with the same level of intensity. Relying on a “first-in, first-out” approach leads to wasted effort on borrowers who would have paid anyway, while high-risk accounts slip through the cracks. Efficiency begins when you use real-time portfolio data to dictate your daily workflow. By letting data guide your team, you ensure that every minute spent on the phone is a minute spent where the risk is highest.

Modern lenders are moving away from manual oversight and toward automated systems that flag trouble before it becomes a charge-off. This proactive stance requires a central hub where all borrower information lives. When your data is siloed, your team is flying blind. Centralizing this information allows you to spot patterns, such as a borrower who consistently pays late but always pays, versus one whose behavior has suddenly and drastically changed. Staying informed about consumer rights in debt collection is also essential as you refine these data-driven outreach strategies to remain compliant with federal standards.

Account Scoring and Portfolio Segmentation

Account scoring is a strategic tool that assigns a numerical value to each borrower based on their likelihood of default, allowing lenders to allocate resources where they are needed most. By implementing this within your LMS, you can automatically segment your portfolio into risk tiers. High-risk borrowers, such as those with multiple recent late payments or a history of insurance lapses, should trigger immediate, high-touch intervention. Conversely, low-risk borrowers might only need a simple, automated text reminder. This segmentation saves your staff hours of manual sorting and prevents the “noise” of stable accounts from distracting them from critical recovery tasks.

The Power of Integrated Payment Processing

Reducing friction is the fastest way to secure a payment. If a borrower is ready to pay, any hurdle, such as being redirected to a third-party site or having to call during business hours, increases the chance of a hang-up. Integrating your payment processing directly into your LMS ensures that once a payment is made, the account status updates instantly across your entire platform. This eliminates the common frustration of “double-calling,” where a collector calls a borrower who has already paid. It also removes the risk of manual data entry errors that occur when staff must move information between separate banking and management systems. To see how this looks in practice, you might consider how the Verifacto LMS unifies these processes into one seamless interface.

Automated Communication: Closing the Recovery Gap

Manual phone calls are no longer the powerhouse of recovery they once were. In fact, relying solely on a call-heavy strategy is a recipe for high overhead and low engagement. In 2026, borrowers are far more likely to respond to a well-timed text message or push notification than a call from an unrecognized number. By transitioning to automated multi-channel workflows, you bridge the gap between your team’s capacity and the growing volume of accounts. This shift is a cornerstone of improving collection efficiency auto loans, as it allows your system to handle routine reminders while your staff focuses on complex negotiations.

Automation doesn’t mean sacrificing compliance. With strict limits on call frequency under Regulation F, which limits collectors to seven calls per week per debt, staying within the bounds of the law is easier when your communication is systematic. Adhering to the CFPB Auto Finance Guidelines ensures your automated outreach remains professional and legally sound. By using pre-vetted templates for SMS and email, you eliminate the risk of a staff member making an unscripted, non-compliant statement during a high-pressure call. Lenders who want a comprehensive framework for compliant, modernized outreach can benefit from reviewing auto finance collections best practices to align their communication strategies with today’s regulatory and technological standards.

Implementing a Multi-Channel Outreach Strategy

Timing is everything in recovery. A reminder sent seven days before a due date is far more effective than a collection call made seven days after a missed payment. SMS often outperforms phone calls for subprime segments because it provides a non-confrontational way for borrowers to acknowledge their debt. When you use Automated Borrower Communication, you can personalize these templates to maintain a partner-like tone. This approach treats the borrower as a client who needs a nudge rather than a target to be chased, which often leads to higher self-cure rates.

Borrower Portals and Self-Service Solutions

True efficiency comes from empowering borrowers to solve their own problems. Online portals allow your clients to manage payments, view balances, and update contact information 24/7 without ever speaking to a representative. This self-service culture drastically reduces inbound call volume for routine inquiries, freeing your team to handle high-priority accounts. These portals are also excellent tools for collecting updated insurance information. By making it easy for borrowers to upload documents or pay via built-in processing, you remove the friction that often leads to delinquency. This proactive management is essential for improving collection efficiency auto loans in a digital-first market.

Proactive Risk Management: The Insurance Factor

Many lenders overlook the strongest predictor of account failure: the insurance lapse. When a borrower stops paying their auto insurance premium, it’s rarely an isolated incident. It’s often the first domino to fall in a financial crisis. By integrating real-time Seguimiento de Seguros into your daily operations, you gain a massive head start on your recovery efforts. This proactive approach is a game-changer for improving collection efficiency auto loans because it flags high-risk accounts weeks before they actually hit the delinquency report.

Waiting for a 30-day past-due notice to take action is a reactive strategy that costs you money. Automated systems change the dynamic by alerting you the moment a policy is cancelled or non-renewed. This allows your team to reach out with a supportive, problem-solving tone while the borrower still has the vehicle and a chance to rectify the situation. It shifts the conversation from a hostile collection call to a helpful reminder about maintaining compliance with their loan agreement. This early visibility is the difference between a simple correction and a total loss. Understanding how to reduce charge-offs in auto finance starts with closing exactly these kinds of visibility gaps before a missed payment becomes a permanent write-off.

Real-Time Insurance Tracking as an Early Warning System

Monitoring coverage status allows you to identify high-risk accounts early, often before a payment is even missed. When a policy lapses, your system should automatically trigger a notification to both the staff and the borrower. Insurance tracking protects the lender’s lien position by ensuring the collateral remains covered against physical damage or loss throughout the life of the loan. This visibility eliminates the manual “busy work” of calling agents or checking carrier websites. Your staff can finally stop acting as administrative clerks and start acting as strategic recovery specialists.

Mitigating Risk with CPI Solutions

When a borrower fails to maintain their own coverage, CPI Solutions provide a vital safety net. Implementing lender-placed insurance isn’t just about protecting the asset; it’s about maintaining the health of your entire portfolio. Compliance and transparency are essential in CPI administration to avoid regulatory friction and maintain borrower trust. Verifacto’s insurance tracking streamlines this entire verification process, ensuring that you only place coverage when absolutely necessary. This level of precision protects your interests without placing undue burden on your clients. To see how these tools work together to protect your bottom line, explore our Insurance Tracking and CPI Solutions today.

The Ultimate Checklist for Improving Collection Efficiency

Transforming your recovery rates requires a methodical approach. You can’t fix every operational leak at once, but you can follow a proven path to stability and growth. This checklist provides the tactical steps necessary for improving collection efficiency auto loans by moving from manual guesswork to automated precision. Use these steps to audit your current workflow and implement the tools that protect your bottom line.

- Step 1: Audit your current LMS/DMS data for accuracy and integration. Ensure your borrower profiles, contact information, and loan balances are consistent across all platforms.

- Step 2: Automate your first-tier payment reminders. Set triggers to send SMS or email notifications seven days prior to the due date to encourage self-curing.

- Step 3: Implement real-time insurance monitoring for the entire portfolio. Link your insurance tracking directly to your collection alerts so a policy lapse triggers immediate outreach.

- Step 4: Deploy a digital payment portal to remove friction. Give borrowers a 24/7 self-service option with built-in payment processing to capture funds the moment they’re available.

- Step 5: Establish a weekly reporting rhythm. Track recovery rates, delinquency buckets, and staff productivity to identify where the system needs refinement.

Phase 1: Operational Cleanup and Integration

The foundation of efficiency is clean data. Start by consolidating your borrower records into a single cloud-based platform like the Verifacto LMS. When your data is fragmented across different spreadsheets or legacy systems, your team loses time searching for answers instead of securing payments. Verify that your payment processing is linked directly to your loan balances. This ensures that when a borrower pays through the portal, the account status updates across the DMS and LMS instantly. Once your data is unified, you can set up automated borrower communication triggers that handle routine follow-ups without manual intervention.

Phase 2: Continuous Monitoring and Optimization

A static strategy won’t survive the 2026 market. You must constantly refine your account scoring models based on monthly performance data. If certain risk tiers are showing higher-than-expected defaults, adjust your outreach frequency accordingly. Auditing your insurance verification workflows is also critical. Speed is the priority here; the faster you identify a lapse, the faster you can deploy CPI Solutions or contact the borrower to rectify the situation. This proactive cycle allows you to scale your operations and manage a larger portfolio without adding additional headcount. By improving collection efficiency auto loans through this iterative process, you build a resilient lending business that can withstand economic volatility.

Secure Your Portfolio with Future-Ready Collection Strategies

The 2026 auto lending market demands a departure from the labor-intensive, reactive methods of the past. Success now hinges on your ability to spot risks before they lead to defaults and to communicate with borrowers through the channels they actually use. By centralizing your data and integrating real-time insurance tracking, you move from a state of constant firefighting to a streamlined, predictable recovery operation. This transition is the key to improving collection efficiency auto loans without ballooning your operational costs.

You’ve seen how automated communication and proactive risk management can transform your recovery rates while reducing the burden on your staff. Now is the time to replace fragmented spreadsheets with a unified system that provides total portfolio visibility. Streamline your collections with Verifacto’s integrated LMS & DMS platform today. Our solution provides real-time insurance tracking and CPI solutions, automated borrower communication tools, and a comprehensive cloud-based integration designed for modern lenders. You have the roadmap to better portfolio health, and we have the tools to help you get there. Let’s start building a more secure and efficient future for your lending business.

Frequently Asked Questions

What is the most effective way to improve auto loan collection efficiency?

The most effective way is shifting from reactive manual calling to proactive, data-driven automation. By integrating your DMS and LMS data, you can prioritize accounts based on risk scoring rather than simple due dates. This ensures your team spends their limited time on high-stakes recoveries while automated tools handle routine reminders for stable accounts. It’s about working smarter with the data you already have.

How does automation help in reducing auto loan charge-offs?

Automation reduces charge-offs by identifying and acting on risk signals before they escalate into defaults. For example, an automated system can flag an insurance lapse or a missed payment window immediately, triggering instant multi-channel outreach. This speed allows you to intervene while the borrower is still reachable and the vehicle is accessible, preventing small delays from becoming permanent losses that hurt your bottom line. Lenders looking for a deeper operational framework can explore the complete 2026 guide on how to reduce charge-offs in auto finance for additional strategies tailored to today’s market conditions.

Is text messaging compliant for auto loan collections?

Yes, text messaging is compliant provided you adhere to the Telephone Consumer Protection Act (TCPA) and FDCPA guidelines. You must obtain proper consent and offer clear opt-out options for every borrower. Using Automated Borrower Communication tools helps maintain compliance by ensuring every message follows pre-approved templates and respects federal communication frequency limits, protecting your business from costly legal errors.

How does insurance tracking impact the collections process?

Insurance tracking acts as an early warning system for potential payment defaults. When a borrower allows their policy to lapse, it often signals financial distress that will soon affect their loan payment. By monitoring coverage in real-time, you can initiate contact earlier. This protects your lien position and encourages the borrower to maintain compliance with their contract before they fall into severe delinquency.

What are the benefits of an integrated LMS and DMS for collections?

An integrated LMS and DMS eliminates data silos that cause operational friction and errors. When your management systems talk to each other, payment updates, insurance status, and contact history are visible in a single interface. This unity is vital for improving collection efficiency auto loans because it prevents collectors from calling borrowers who have already paid or using outdated contact information that wastes time.

How often should I send automated payment reminders to borrowers?

A common best practice is to send reminders seven days before the due date, on the due date, and three days after a missed payment. This cadence keeps the obligation top of mind without becoming intrusive. Automated systems allow you to customize this frequency based on the borrower’s risk tier, ensuring higher-risk accounts receive more persistent outreach while low-risk accounts enjoy a lighter touch.

Can I improve collection efficiency without hiring more staff?

You can absolutely improve your efficiency without increasing headcount by leveraging technology to handle repetitive tasks. Automation manages the bulk of first-tier communication and data entry, which allows your existing staff to focus exclusively on high-priority negotiations. This approach scales your operations and improves your portfolio health by maximizing the productivity of your current team through streamlined, cloud-based workflows.

What role does a borrower portal play in reducing delinquency?

A borrower portal reduces delinquency by removing the barriers that prevent on-time payments. Providing a 24/7 self-service platform allows borrowers to pay, view balances, and update insurance information at their convenience. This autonomy is essential for improving collection efficiency auto loans because it captures payments that might otherwise be delayed by limited business hours or long hold times on the phone.