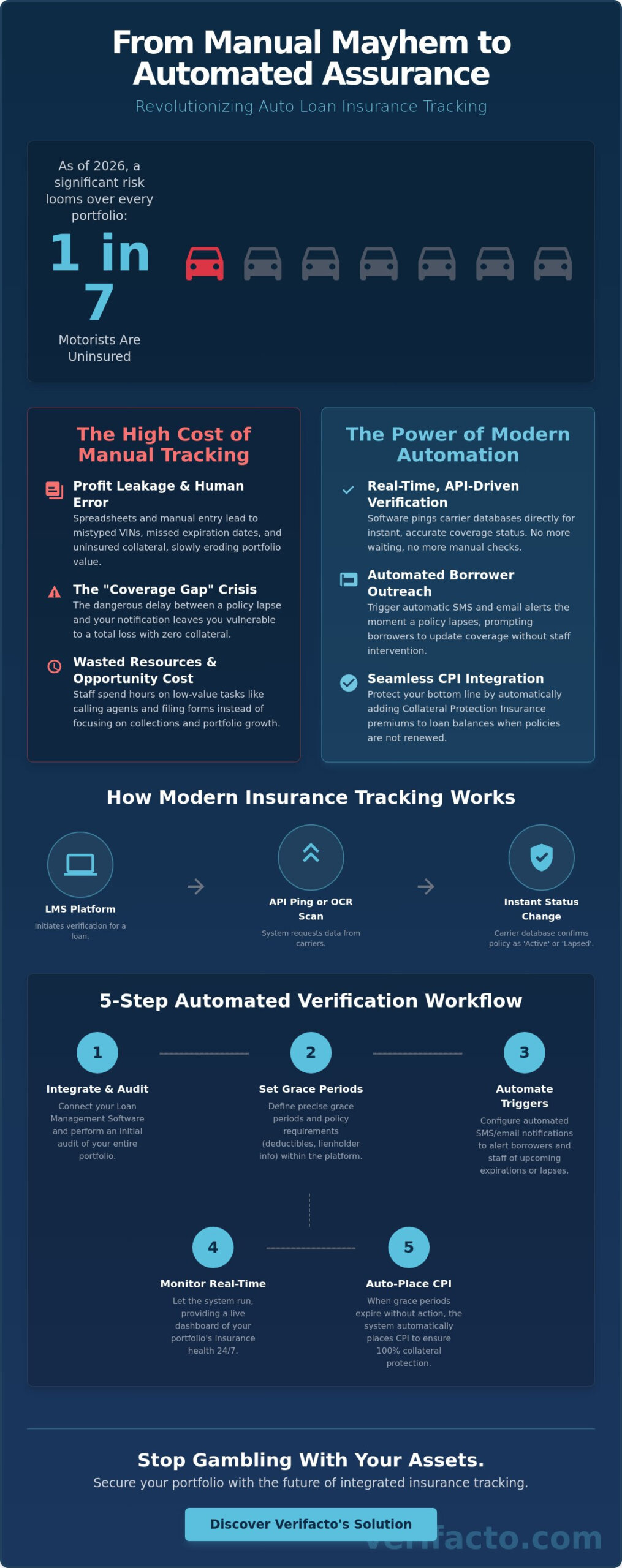

Did you know that 1 in 7 motorists on the road are driving without insurance as of May 2026? With the national average cost for full coverage auto insurance reaching $2,932 this year, the temptation for borrowers to let their policies lapse has never been higher. You’ve likely felt the frustration of manual data entry errors or the anxiety of the “total loss trap” where a destroyed vehicle leaves you with zero collateral. Relying on outdated spreadsheets to manage these risks is a gamble your business can’t afford to take.

It’s time to modernize your approach. Discover how to eliminate manual paperwork and protect your collateral using real-time insurance tracking in loan management software. By integrating these tools directly into your workflow, you’ll gain instant visibility into your entire portfolio and reduce overhead costs. This guide explores the transition from slow, manual verification to API-driven automation, ensuring a seamless move to CPI solutions when coverage fails. Learn how to turn insurance tracking from a support task into a powerful data layer that secures your bottom line and keeps your operations moving at full speed.

Key Takeaways

- Stop profit leakage by identifying why manual insurance verification fails to scale in high-volume lending environments.

- Leverage real-time insurance tracking in loan management software to replace slow spreadsheets with instant, API-driven data feeds.

- Streamline borrower outreach with automated SMS and email triggers that prompt coverage updates without manual staff intervention.

- Protect your bottom line by integrating CPI solutions that automatically add premiums to loan balances when policies lapse.

- Implement a proven five-step workflow to audit your portfolio and set precise grace periods within your management platform.

The High Cost of Manual Insurance Tracking for Auto Lenders

Manual insurance tracking is more than just a back-office nuisance; it’s a significant drain on your dealership’s profit margins. In a high-volume Buy-Here-Pay-Here (BHPH) environment, the sheer scale of monitoring hundreds or thousands of policies makes spreadsheets obsolete. When your team relies on manual data entry, they’re prone to “leakage”—the slow erosion of portfolio value caused by uninsured collateral. Every vehicle on the road without active coverage represents a potential total loss that your business will have to absorb. By failing to utilize modern insurance tracking in loan management software, you’re essentially gambling with your assets.

The opportunity cost of manual labor is equally damaging. When talented staff members spend their afternoons filing ACORD forms and calling insurance agents, they aren’t focusing on high-value tasks. You should be reallocating that human capital toward active collections and portfolio growth. Shifting away from paperwork allows your team to be proactive rather than reactive, turning a defensive support task into a streamlined operational advantage.

The ‘Coverage Gap’ Crisis in Auto Finance

The coverage gap is the dangerous window of time between a borrower’s policy cancellation and the moment you actually find out about it. In the volatile market of 2026, where insurance premiums have spiked to an annual average of $2,932, borrowers are more likely than ever to let policies lapse to save cash. If a vehicle is stolen or totaled during this gap, the lender is left with a worthless asset and a borrower who cannot pay. Real-time data is the only way to close this window. Without it, you lack the speed required to initiate Seguro de Protección Colateral (CPI): before a disaster occurs, leaving your capital completely exposed.

Operational Friction and Human Error

Human error is the silent killer of manual verification systems. A single mistyped VIN or a missed expiration date in a spreadsheet can lead to false positives or, worse, a failure to track a high-risk account. Manual systems also suffer from notification fatigue. When staff members are overwhelmed by a mountain of follow-ups, they often miss the critical warning signs of a pending cancellation. This friction directly impacts your bottom line by improving collection efficiency for auto loans through the removal of administrative distractions. When you integrate insurance tracking in loan management software, you eliminate the “lost in the shuffle” excuse and ensure that every policy is monitored with machine precision.

Inaccurate data also creates compliance landmines. Sending a lender-placed insurance notification based on a typo or an outdated record can lead to legal friction and regulatory scrutiny. Precision isn’t just about protecting the car; it’s about protecting the business from the liability of improper CPI placement. A robust approach to lender placed insurance management provides the audit trail and accuracy needed to navigate these high-stakes requirements safely. Automation ensures that every notice is triggered at the correct interval and every record is defensible during a regulatory review.

How Modern Insurance Tracking in Loan Management Software Works

Modern insurance tracking in loan management software is a high-speed data exchange that removes the need for manual phone calls and paper checks. Instead of waiting for a physical letter from an insurance agent, the software uses Application Programming Interfaces (APIs) to “ping” carrier databases. This allows your system to verify coverage status, deductible limits, and lienholder accuracy in seconds. For carriers that still rely on physical mail, modern systems use Optical Character Recognition (OCR) and Document AI to scan policy declaration pages and transform them into actionable digital records instantly.

This technology relies on an event-driven architecture. The moment a policy status changes from “active” to “lapsed” or “cancelled” at the carrier level, a digital signal travels to your LMS. This triggers an immediate alert, allowing you to act before the collateral is at risk. It’s a proactive shield that ensures your data is never more than a few minutes old.

Real-Time Verification vs. Batch Processing

In the past, lenders relied on weekly batch reports to catch uninsured borrowers. This delay created a massive “Friday afternoon” risk where a vehicle could be totaled over the weekend without the lender even knowing the policy had lapsed. The 2026 standard has moved toward instantaneous pings. This shift is a cornerstone of mitigating risk in auto lending by providing a proactive data layer that never sleeps. It ensures that your portfolio remains protected every hour of the week, not just when a report is generated.

The Integration Bridge: DMS to LMS to Carrier

Effective automation requires a seamless flow of information. It starts in your Dealership Management System (DMS) during the initial sale and flows into the tracking module of your LMS. This creates a “single source of truth” where borrower contact info, VIN data, and insurance status live in one place. Understanding how to track auto insurance on a loan portfolio at scale requires this native integration. Without it, you’re stuck managing two different systems that don’t talk to each other.

Lenders must also stay aligned with guidelines from the Consumer Financial Protection Bureau to ensure borrower communications and CPI placements remain compliant. By bridging the gap between carriers and your internal records, you eliminate data silos and reduce operational friction. If you want to stop chasing paperwork and start protecting your assets, integrating your LMS with a real-time tracking solution is the most decisive move you can make.

Must-Have Automation Features for Your LMS Platform

Identifying an insurance lapse is only half the battle. To truly protect your portfolio, your system must act on that data without waiting for a manual prompt. When you evaluate insurance tracking in loan management software, look for tools that move beyond passive monitoring and into active resolution. The most effective platforms in 2026 prioritize speed and accuracy through features like Carrier Direct-Connect. This technology establishes a digital handshake with insurance providers, confirming coverage details without forcing the borrower to act as a middleman for paperwork. It removes the friction of waiting for “dec-pages” to arrive by mail.

Modern lenders also require high-level visibility to stay ahead of regulatory requirements. Your automation suite should include:

- Compliance Reporting Dashboards: Generate one-click audits for state and federal reviews to prove you followed all legal notice periods.

- Mobile-First Verification: Allow borrowers to snap a photo of their insurance card and upload it directly into the LMS for instant OCR validation.

- Carrier Direct-Connect: Bypass the borrower entirely by pulling real-time status updates from thousands of insurance databases.

Intelligent Communication Workflows

Borrowers are more likely to respond when you meet them where they live: on their phones. Multi-channel communication using SMS, email, and integrated IVR increases response rates by ensuring your message isn’t buried in a physical mailbox. Automation allows you to set an escalation ladder, starting with “soft” reminders and moving to “hard” legal notices as the grace period expires. Modern LMS automation doesn’t just track data; it executes a communication strategy that preserves the borrower relationship. By keeping the tone helpful and professional, you reduce the likelihood of a borrower feeling harassed while still maintaining strict collateral standards.

Seamless CPI Placement and Billing

When a borrower fails to provide proof of insurance, the transition to lender-placed coverage must be instantaneous. The software should automatically calculate the required premium and apply it to the loan balance according to your predefined rules. This “force-placed” mechanism ensures there’s never a day where your asset is unprotected. Just as importantly, the system should handle automated refunds the moment a borrower provides proof of underlying insurance. This level of precision is a key part of integrated payment solutions for dealers, as it keeps the borrower’s ledger accurate and prevents billing disputes. When tracking and billing live in the same ecosystem, you eliminate the data silos that lead to financial leakage and borrower frustration.

5 Steps to Automate Your Insurance Verification Workflow

Transitioning to an automated system requires a strategic roadmap rather than a “set it and forget it” mentality. You can’t simply flip a switch and expect perfect results if your underlying data is messy. Following a structured implementation plan ensures that your insurance tracking in loan management software performs at its peak from day one. By moving through these five steps, you’ll replace manual friction with a high-speed digital loop that protects every asset in your portfolio.

- Step 1: Audit for Data Cleanliness. Scrub your current portfolio for VIN accuracy and updated borrower contact info. If the software doesn’t have the correct VIN, it can’t ping carrier databases effectively.

- Step 2: Define Your Rules. Establish your “If/Then” logic within your LMS settings. Set your grace periods and decide exactly when automated notifications should trigger.

- Step 3: Connect the System. Link your LMS to your integrated tracking service. This creates the digital bridge that allows real-time status updates to flow directly into your borrower ledgers.

- Step 4: Automate Inbound Channels. Set up a dedicated portal for carrier and borrower uploads. This removes your staff from the document-handling loop by allowing OCR technology to process incoming data.

- Step 5: Manage by Exception. Shift your team’s focus away from routine checks. They should only intervene when the software flags an account on the “Exceptions Report” for manual resolution.

By implementing insurance tracking in loan management software, you move from a reactive posture to a proactive one, ensuring no lapse goes unnoticed for more than a few hours.

Phase 1: Data Sanitization and Rule Setting

The biggest threat to automation success is “garbage in, garbage out.” Your system’s logic is only as good as the data it processes. This is where understanding what is DMS becomes critical. Your DMS must feed 100% accurate collateral data into the tracking module to prevent false alarms. When setting your rules, align with 2026 industry standards by establishing grace periods between 10 and 15 days. This provides a fair window for borrowers to fix lapses while still protecting your interests.

Phase 2: Launching the Automated Loop

Don’t roll out automation to your entire portfolio at once. Run a pilot program on a small segment, such as new loans from the last 30 days. This allows you to refine your notification triggers and train staff to handle their new roles as exception managers instead of data entry clerks. Once you’ve polished the process, optimize your workflow with Verifacto’s automated insurance tracking to secure your entire operation and eliminate the “total loss trap” for good.

Verifacto: The Future of Integrated Insurance Tracking & CPI

Native integration is the dividing line between modern efficiency and administrative chaos. Most third-party “bolt-on” tracking services operate in a vacuum, requiring constant manual syncing between your loan data and their monitoring portal. Verifacto eliminates this friction by embedding insurance tracking in loan management software as a foundational component. When you open a borrower’s loan ledger, you aren’t just looking at their payment history; you’re seeing their real-time insurance status, deductible limits, and carrier details. This centralized visibility ensures that your team never makes a collection or repossession decision based on outdated information.

Our platform is designed specifically for the high-velocity world of auto lending and Buy-Here-Pay-Here (BHPH) dealerships. While generic management systems try to be everything to everyone, Verifacto focuses on the “no-nonsense” requirements of collateral protection. By automating the transition from a standard policy to a CPI solution, we ensure your assets are protected without adding a single minute of manual work to your day. It’s about maintaining control over your portfolio without the burden of constant oversight.

The Verifacto Advantage: DMS + LMS + Tracking

The power of Verifacto lies in its cloud-based ecosystem. By housing your DMS, LMS, and insurance tracking in one place, you remove the possibility of data mismatches. Information flows instantly from the initial sale to the tracking module, creating a seamless audit trail. This integration is particularly valuable for billing accuracy. Our built-in payment processing handles CPI premium collection automatically, ensuring that insurance costs are accurately reflected in the borrower’s balance without manual ledger adjustments. It’s a closed-loop system that preserves your capital and your time.

Results-Oriented Risk Mitigation

Investing in a modern tracking infrastructure isn’t just about convenience; it’s about measurable ROI. By eliminating the “total loss trap” mentioned in our guide, you significantly lower your charge-offs and protect your most valuable assets. You’ll see fewer manual hours spent on the phone with carriers and 100% compliance with state and federal notification requirements. Using insurance tracking in loan management software turns a defensive necessity into a strategic advantage.

The future of lending is automated, secure, and data-driven. Don’t let manual paperwork erode your profit margins or expose your portfolio to unnecessary risk. It’s time to transition your operations to a platform that works as hard as you do. Schedule a demo of Verifacto’s Insurance Tracking today and take full control of your collateral protection strategy.

Secure Your Portfolio with Automated Precision

The 2026 lending market leaves no room for manual oversight or data silos. You’ve seen how manual verification erodes profit margins and how real-time API pings eliminate the dangerous “coverage gap” before it results in a total loss. By moving to a system that prioritizes native insurance tracking in loan management software, you replace administrative friction with a proactive shield for your collateral. This transition ensures that your team focuses on growth rather than chasing paperwork.

Verifacto provides a cloud-based DMS and LMS integration that brings your dealer, loan, and insurance data into a single, actionable ledger. With real-time carrier pings and automated CPI placement and refunds, your operation stays protected without adding complexity to your daily workflow. This isn’t just about saving time; it’s about securing the long-term stability of your entire portfolio and ensuring 100% compliance across every account. You don’t have to choose between speed and security when you have the right technology in place.

Streamline your risk management with Verifacto’s integrated insurance tracking.

Take the decisive step toward a modernized and secure lending environment. You’ve got the roadmap to eliminate manual paperwork; now it’s time to put that automation to work for your bottom line.

Frequently Asked Questions

How much time can I really save by automating insurance verification?

Automation typically reduces manual administrative labor by 70% to 90% for most auto lenders. Instead of spending hours calling carriers and filing physical policy documents, your team only intervenes when the system flags a specific exception. This shift allows you to reallocate dozens of staff hours every week toward active collections and portfolio growth.

Will automated tracking work with all insurance carriers?

Modern systems utilize a multi-layered approach to ensure 100% coverage across all providers. High-speed APIs handle direct communication with major national carriers for instant updates. For smaller or regional providers, the software uses Document AI and OCR technology to scan and verify policy declaration pages with machine precision.

What happens if a borrower provides proof of insurance after CPI is placed?

The system handles this transition through an automated refund process. Once the software verifies that underlying coverage was active during the period in question, it calculates the unearned premium and credits the borrower’s ledger. This ensures the loan balance remains accurate and prevents the billing friction often associated with manual credit adjustments.

Is automated insurance tracking compliant with state lending regulations?

Built-in insurance tracking in loan management software is designed to follow the strict notice timelines required by state and federal regulators. The system automatically triggers the necessary “soft” and “hard” notices at the correct intervals. It also maintains a comprehensive digital audit trail, making it easy to prove compliance during a regulatory review.

Do I need to hire a third-party service, or is it built into my LMS?

While some lenders use “bolt-on” third-party tools, the most efficient approach is native integration within your LMS. Verifacto builds this tracking directly into the platform to eliminate the need for manual data syncing. This creates a single source of truth where insurance status and loan data live in the same ecosystem.

How does the software handle ‘non-standard’ or high-risk insurance carriers?

The software treats non-standard carriers with the same level of scrutiny as any other provider. It extracts critical data points such as deductible limits and lienholder naming to ensure the policy meets your specific risk requirements. If a policy fails to meet your predefined standards, the system immediately flags the account for your team to review.

Can I customize the text and frequency of the automated reminders?

You have full control over the communication ladder and the messaging used for borrower outreach. You can define the length of the grace period, choose between SMS or email delivery, and edit the specific wording of every notice. This customization allows you to maintain a professional relationship with your borrowers while enforcing strict collateral standards.

What is the typical ROI for a mid-sized auto lender switching to automated tracking?

Most lenders see a rapid return on investment through the combination of reduced charge-offs and lower operational overhead. By eliminating the risk of a total loss on an uninsured vehicle, the system protects your most valuable assets. Implementing insurance tracking in loan management software typically pays for itself within the first few months of deployment by stopping financial leakage. For a deeper dive into compliance timelines and force-placed notice requirements, review the lender placed insurance management operational reference guide to ensure your workflow meets the latest 2026 regulatory standards.