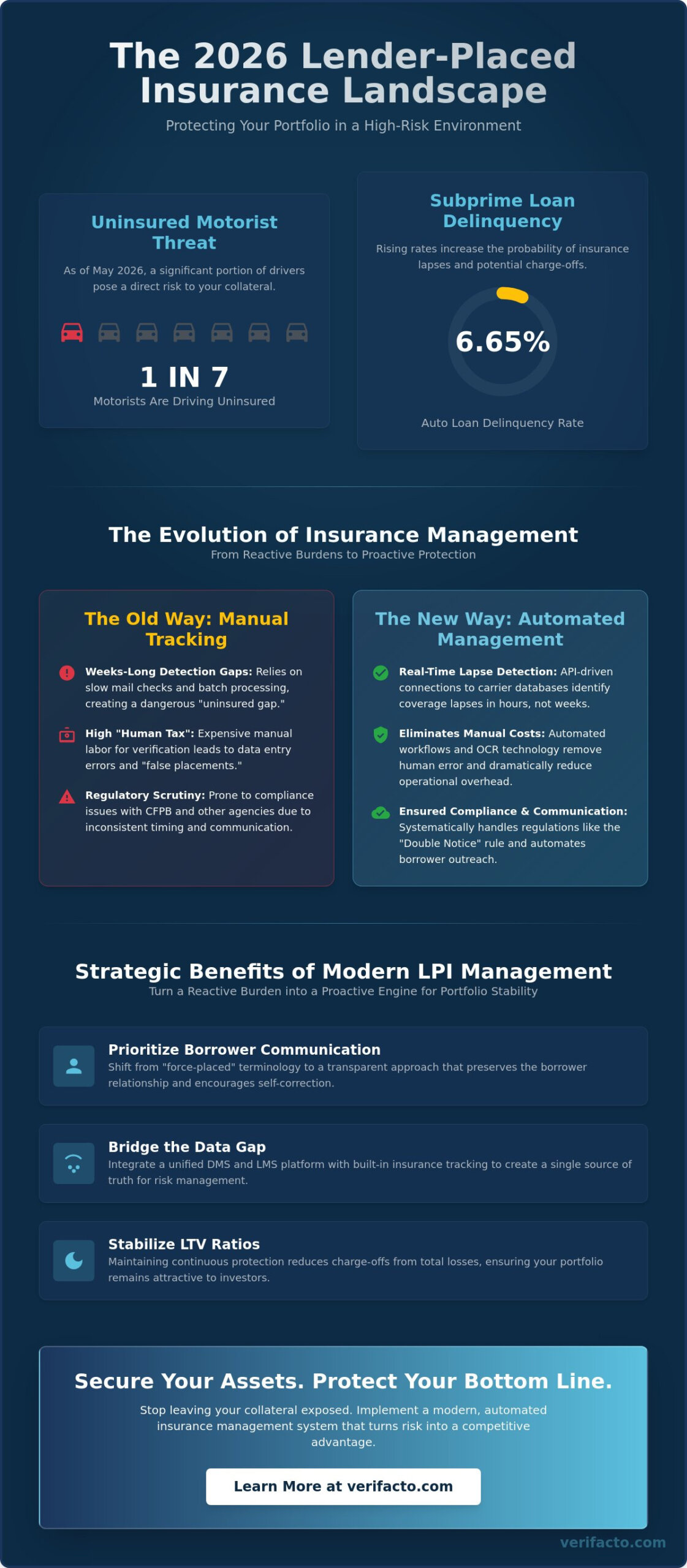

Did you know that as of May 2026, 1 in 7 motorists are driving without insurance while subprime auto loan delinquency rates have climbed to 6.65%? These numbers represent more than just market trends; they’re a direct threat to your bottom line. Effective lender placed insurance management is no longer just a back-office checkbox, it’s a critical defensive strategy for protecting your collateral in a high-stakes environment. We understand the pressure of rising replacement costs and the constant anxiety of a potential total loss due to a coverage lapse.

You’re likely tired of the high manual labor costs associated with insurance verification and the looming shadow of regulatory scrutiny regarding force-placed timing. This 2026 operational guide promises to help you master these complexities. You’ll learn how to implement a streamlined workflow that reduces charge-offs and ensures full compliance with the latest CFPB and Fannie Mae mandates, such as the new allowance for Actual Cash Value (ACV) coverage on roofs. We’ll preview the move toward real-time automation and explain how modernizing your tracking systems turns a reactive burden into a proactive engine for portfolio stability.

Key Takeaways

- Modernize your approach by understanding the shift toward transparent lender placed insurance management that prioritizes borrower communication and terminology.

- Discover how API-driven real-time tracking identifies coverage lapses in hours rather than weeks, effectively eliminating the risk of total loss on collateral.

- Calculate the “Human Tax” on your operations and learn how automated workflows remove the hidden manual labor costs of insurance verification.

- Navigate the latest CFPB regulations and the “Double Notice” rule to ensure your placement practices remain fully compliant and strategically timed.

- Bridge the data gap between loan servicing and risk management by integrating a unified DMS and LMS platform with built-in insurance tracking.

What is Lender Placed Insurance Management in 2026?

In 2026, lender placed insurance management is the systematic, data-driven monitoring of your entire portfolio’s insurance status. The industry has moved away from the aggressive “force-placed” terminology of the past. Today, the focus is on transparency and borrower communication. This shift reflects a commitment to regulatory alignment and long-term portfolio health rather than just reactive risk transfer. You’re no longer just checking boxes; you’re safeguarding the financial integrity of every asset in your care.

Manual tracking remains the single biggest vulnerability for auto finance companies. With 1 in 7 motorists driving without insurance as of June 2026, relying on spreadsheets or intermittent mail checks is a recipe for disaster. Human error in data entry often leads to “false placements,” where coverage is added to a vehicle that actually has insurance. This mistake doesn’t just annoy borrowers; it attracts intense regulatory scrutiny from the CFPB. If your team discovers a lapse weeks after it happens, you’ve already lost the window for proactive protection.

The Role of Collateral Protection Insurance (CPI)

While often used interchangeably with lender-placed insurance, Collateral Protection Insurance (CPI) offers specific advantages for the auto sector. If you’re asking what is collateral protection insurance and how it differs from standard force-placed coverage, understanding its operational mechanics is essential for managing subprime portfolios effectively. CPI solutions are particularly effective for subprime loan portfolios where delinquency rates hit 6.65% at the end of 2025. These policies allow lenders to issue coverage quickly, often on a monthly basis, ensuring that the asset remains protected even when the borrower’s financial situation is volatile. Real-time tracking is the engine that makes this possible. Without it, the administrative burden of managing individual CPI certificates can quickly outweigh the benefits of the coverage itself.

Why LPI Management is a Strategic Necessity

Uninsured collateral loss is a silent killer of annual profits. When a vehicle is totaled without active coverage, the remaining loan balance typically becomes a total charge-off. Proactive lender placed insurance management reduces the “uninsured gap,” which is the dangerous period between a policy lapse and the placement of new coverage. By maintaining continuous protection, you stabilize your loan-to-value (LTV) ratios. This consistency ensures that your portfolio remains attractive to warehouse lenders and secondary market investors who demand rigorous risk mitigation. Modernizing this process isn’t just about saving time; it’s about securing the capital you’ve deployed.

Real-Time Tracking: The Foundation of Modern Insurance Management

Batch processing is a relic of a slower era. In today’s high-velocity market, waiting thirty days for a status report on your collateral is a liability you can’t afford. Modern lender placed insurance management has evolved into an API-driven discipline that connects your loan management system directly to insurance carrier databases. This transition from static records to live data feeds means you identify coverage lapses within hours, not weeks. When a policy is canceled at noon, your system should know by the end of the business day.

Direct data feeds from national carriers eliminate the guesswork that used to plague risk departments. According to the National Association of Insurance Commissioners (NAIC), Lender-Placed Insurance serves as a vital safeguard, but its success hinges on the speed of detection. Real-time monitoring allows you to trigger automated borrower notifications the moment a lapse is confirmed. This immediate outreach often prompts the borrower to reinstate their policy before you’re forced to place expensive coverage, preserving the borrower relationship while protecting the asset.

Automating the Verification Workflow

If you want to automate insurance verification for car loans, you must move beyond manual data entry. Modern systems use custom triggers for policy expirations and cancellation alerts. For instances where digital feeds aren’t available, OCR technology can read and verify physical declaration pages with high precision. This removes the “human tax” of manual review and ensures that every piece of documentation is processed instantly. You can see how this works in practice by exploring Verifacto’s automated tracking solutions.

Maintaining Data Integrity Across the Portfolio

Accuracy is the bedrock of compliance. Learning how to track auto insurance on a loan portfolio with 100% accuracy requires a single source of truth. You must clean legacy data to remove duplicates and outdated carrier information before transitioning to an automated system. Once your data is scrubbed, the integration between your insurance tracking and loan servicing platforms ensures that every department is working from the same real-time information. This unified approach eliminates the data gap that often leads to costly administrative errors and regulatory fines.

Operational Efficiency: Manual vs. Automated LPI Workflows

Efficiency in 2026 isn’t just about working faster; it’s about eliminating the “Human Tax” that drains your profitability. Every minute an employee spends on hold with an insurance agent or manually typing policy numbers into a spreadsheet is a minute stolen from portfolio growth. Manual lender placed insurance management is inherently slow; it often takes days to process a single stack of declaration pages. This delay creates a window of vulnerability where your collateral is unprotected. Automation transforms this process, moving your team from data entry clerks to strategic risk managers.

Automation also solves the problem of false placements, which are the primary driver of borrower disputes. False placements occur when manual errors suggest a lapse where none exists. These mistakes don’t just cause administrative headaches; they can lead to damaging complaints and regulatory fines. As the Washington State Office of the Insurance Commissioner explains, Lender-placed insurance exists to protect the creditor’s interest, but it shouldn’t become a source of unnecessary conflict. Automated systems ensure that coverage is only triggered when verified data confirms it’s necessary, protecting your reputation alongside your assets.

The Pitfalls of Manual Verification

Manual verification relies on stale data. By the time a clerk reviews a physical mailer, the policy status may have already changed. This lag makes it impossible to stay current with fluctuating state regulations or specific carrier notification requirements. Additionally, the repetitive nature of manual tracking leads to high employee burnout and turnover. When your risk department is a revolving door, you’re constantly training new staff, which further compromises the accuracy and security of your insurance monitoring.

The ROI of Automated Insurance Management

The return on investment for automated systems is immediate and measurable. You’ll see direct savings from reduced headcounts and a dramatic drop in administrative errors. Beyond the balance sheet, you’ll benefit from improved borrower retention because customers stay loyal when they aren’t hit with erroneous insurance charges. It’s about building a scalable operation that grows without a linear increase in labor costs. Automated systems typically reduce the time spent on insurance verification by up to 80% compared to traditional manual methods.

Navigating Compliance and Borrower Communication in 2026

Regulatory scrutiny around lender placed insurance management has reached a peak in 2026. The CFPB continues to focus on “unfair, deceptive, or abusive” practices, specifically targeting lenders who place coverage without sufficient notice or at inflated costs. Compliance isn’t just about following the rules; it’s about maintaining the delicate balance between mitigating risk in auto lending and respecting consumer rights. When you prioritize transparency, you reduce the “sticker shock” that often triggers borrower defaults and legal disputes.

The “Double Notice” rule remains the gold standard for compliance. You must send the first notice at least 45 days before charging the borrower for coverage, followed by a second notice at least 15 days before placement. This timeline gives borrowers ample opportunity to provide proof of their own insurance. By automating these communications, you ensure that no deadline is missed and every notice is sent with surgical precision. This proactive approach prevents the administrative nightmare of reversing charges and handling angry phone calls from borrowers who were caught off guard.

Best Practices for Borrower Notifications

Don’t rely on a single letter in the mail that might get lost or ignored. Use multi-channel communication, including SMS and email, to ensure your message reaches the borrower immediately. Your notices should be clear and non-threatening, framed as a helpful reminder to maintain their required coverage rather than a penalty. Automation allows you to send these alerts the moment a lapse is detected, encouraging voluntary compliance before a forced placement becomes necessary. To see how to streamline these workflows, explore Verifacto’s automated borrower communication tools.

Audit-Ready Record Keeping

State examiners don’t just want to know that you’re compliant; they want you to prove it. A robust lender placed insurance management strategy includes maintaining a comprehensive digital trail of every verification attempt and communication sent. You should be able to generate detailed compliance reports in seconds, showing exactly when notices were delivered and what data triggered the placement. Integrating these records into your auto finance compliance management checklist ensures you’re always prepared for an audit without the last-minute scramble for paper files.

Optimizing Your Portfolio with Verifacto’s Integrated Solutions

Modernizing your operations requires more than just adding a new tool to your tech stack; it requires a fundamental shift in how your systems communicate. Verifacto DMS and Verifacto LMS provide a unified foundation where built-in lender placed insurance management isn’t an afterthought, but a core feature. By housing your document management and loan servicing within a single ecosystem, you eliminate the dangerous “data gap” that often exists between servicing teams and risk managers. When insurance data flows seamlessly into the loan record, your team makes decisions based on real-time facts rather than outdated exports or manual spreadsheets.

This integration allows for immediate action the moment a risk is identified. Our CPI Solutions and Insurance Tracking work in tandem to trigger real-time coverage placement as soon as a lapse is confirmed. You don’t have to wait for a manual review process to conclude before protecting your asset. Simultaneously, our Automated Borrower Communication system kicks into gear, sending the necessary compliant notifications across multiple channels. This dual approach ensures your collateral stays protected while you maintain a transparent, professional relationship with your borrowers.

Why True Integration Wins Over Bolt-On Software

Most competitors offer “bolt-on” insurance tracking that requires constant, often buggy data syncing between disparate platforms. This fragmented approach creates unnecessary IT overhead and introduces security risks every time sensitive data is moved between vendors. With Verifacto, you operate from a single, secure, cloud-based source of truth. Real-time visibility allows executives to monitor portfolio health through a single pane of glass, facilitating faster and more accurate decision-making. You no longer have to wait for end-of-month reports to see which vehicles are currently unprotected; the data is live, actionable, and always audit-ready.

Scaling with Confidence

As you look to expand your reach, your infrastructure must support higher-risk portfolios without increasing your vulnerability. Automated lender placed insurance management allows you to take on these more aggressive markets safely by maintaining a tight grip on collateral protection. By reducing the “cost-to-serve” per loan through automation, you maximize your profitability even when delinquency risks are higher. You can scale your portfolio with the assurance that your assets are shielded by a sophisticated, automated guardian that never sleeps. Ready to modernize? Discover how Verifacto’s integrated tracking protects your portfolio.

Secure Your Portfolio with Proactive Risk Management

The transition from reactive tracking to proactive protection is the defining shift for lenders in 2026. By embracing real-time carrier data feeds and an integrated LMS/DMS architecture, you eliminate the dangerous blind spots that lead to uninsured losses. Modern lender placed insurance management is about more than just placing policies; it’s about building a resilient operation that prioritizes accuracy and regulatory compliance. You’ve seen how automation reduces the “human tax” on your staff while ensuring that every borrower interaction is handled with precision through automated multi-channel borrower notifications.

Don’t let legacy systems and manual errors compromise your collateral’s safety. Moving toward a unified platform doesn’t just simplify your workflow; it protects your bottom line and strengthens your standing with regulators. It’s time to replace operational anxiety with the confidence of total visibility and control. Streamline your insurance tracking with Verifacto today and transform your risk management into a strategic advantage. Your portfolio deserves the security of a modern, automated guardian that never sleeps.

Frequently Asked Questions

What is the legal requirement for lender-placed insurance notices?

Lenders must provide at least two written notices to the borrower before charging for a lender-placed policy. The first notice must be sent at least 45 days before any premium charge is applied, followed by a second reminder notice at least 15 days before placement. This specific timeline is a core requirement of the CFPB to ensure borrowers have a fair opportunity to secure their own coverage and avoid unnecessary costs.

How long does a borrower have to provide proof of insurance before placement?

A borrower typically has a 45-day window from the date of the first notice to provide valid proof of insurance. While this grace period is legally mandated, your collateral remains at risk if a lapse has already occurred. Modern lender placed insurance management systems help you initiate this notice cycle the moment a lapse is detected, minimizing the time your asset sits unprotected while waiting for borrower action.

Can lender-placed insurance be cancelled once the borrower provides proof?

Yes, you must cancel the lender-placed policy and refund any overlapping premiums once the borrower provides proof of their own insurance. This cancellation is mandatory for the period where duplicate coverage existed. Automated systems make this process seamless by instantly identifying the new policy data and calculating the exact refund amount, which prevents administrative errors and helps maintain a positive relationship with your borrowers.

Is lender-placed insurance more expensive than standard auto insurance?

Lender-placed insurance is significantly more expensive than standard policies because it is underwritten on a blanket basis without considering the borrower’s individual driving record or credit history. It is a limited-coverage product designed solely to protect the lender’s interest in the collateral. Because it doesn’t offer liability or personal property protection for the borrower, it’s always in the borrower’s best interest to maintain their own private insurance policy.

How does automated insurance tracking reduce false placements?

Automated tracking reduces false placements by replacing manual data entry with real-time API feeds from major national insurance carriers. Instead of waiting for paper mail or manually calling agents, the system cross-references your loan portfolio against live carrier databases. This ensures that you only trigger the notice and placement process when the data confirms a verified lapse, virtually eliminating the human errors that lead to erroneous borrower charges.

Does lender-placed insurance protect the borrower’s equity in the vehicle?

No, lender-placed insurance does not protect the borrower’s equity or provide any liability coverage for the driver. Its primary purpose is to protect the lender’s financial interest in the asset up to the remaining loan balance. Borrowers often mistakenly believe this coverage protects them fully, so clear communication is essential to help them understand that LPI is a defensive measure for the creditor, not a comprehensive solution for the consumer.

What are the common compliance pitfalls in LPI management?

The most frequent pitfalls include failing to adhere to the 45-day notice timeline and lacking a verifiable audit trail for every placement. Lenders often struggle with “stale data” where they place coverage on a vehicle that was already insured, leading to regulatory fines. Robust lender placed insurance management requires a digital record of every communication and verification attempt to prove compliance during state or federal examinations.

Can I integrate insurance tracking with my existing dealer management system?

Yes, you can integrate sophisticated insurance tracking directly with your existing Dealer Management System (DMS) or Loan Management System (LMS). Verifacto’s unified architecture eliminates the need for manual data syncing between different software vendors. This integration ensures that insurance status is visible directly within the borrower’s loan file, creating a single source of truth that improves operational speed and reduces the risk of data gaps across your portfolio.