Successful subprime underwriting in 2026 isn’t about avoiding risk; it’s about pricing it with surgical precision and protecting it through automation. You likely feel the professional anxiety of managing a portfolio where 60-day delinquencies climbed into the mid-6% range late last year. It’s exhausting to watch manual underwriting slow down your team while human error allows high-risk profiles to slip through. To stay profitable and secure, you need a robust subprime auto finance software that moves faster than the market and eliminates the guesswork of borrower verification.

This guide shows you how to master data-driven strategies that slash default rates and maximize your portfolio’s performance. We’ll show you how to integrate alternative data for better risk assessment, automate collateral protection, and ensure compliance with new 2026 federal regulations. You’ll learn how to transform your underwriting from a slow, manual bottleneck into a high-speed engine for growth. By the end of this guide, you will have a clear roadmap for using technology to protect your assets while accelerating your loan approval turnarounds.

Key Takeaways

- Adopt “cash-flow underwriting” to look beyond traditional FICO scores by analyzing real-time bank statements and utility payment history.

- Improve your “speed to lead” by utilizing automated algorithmic scoring to capture subprime borrowers before they move on to a competitor.

- Implement a comprehensive subprime auto finance software to bridge the gap between aggressive underwriting and secure portfolio management.

- Extend your risk management strategy beyond the funding stage by prioritizing automated insurance tracking and continuous collateral monitoring.

- Transition from manual, error-prone workflows to an integrated DMS and LMS platform for real-time visibility and faster decision-making.

The Fundamentals of Subprime Auto Loan Underwriting in 2026

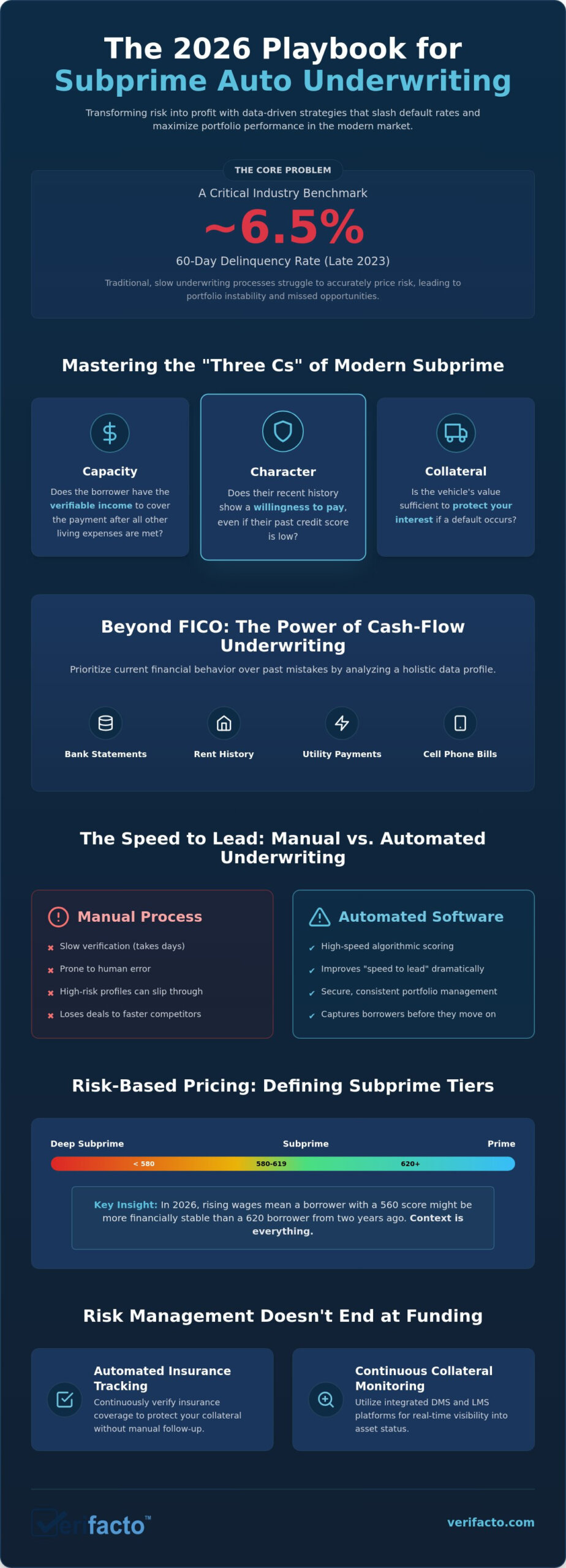

Subprime underwriting in 2026 has evolved far beyond the limitations of a three-digit credit score. It’s now a comprehensive risk assessment that looks at the borrower’s entire financial life to determine their true stability. While Subprime lending was once viewed with extreme caution, it has become a critical and highly profitable segment of the auto market. In 2026, demand for subprime financing is rising steadily. Economic volatility has pushed more consumers out of the “prime” category, but steady wage growth in key sectors like logistics and healthcare means these borrowers have the actual cash flow to support a monthly payment.

Your primary goal as a lender is to find the “sweet spot” between your buy rate and default probability. If your standards are too conservative, you lose profitable deals to more aggressive competitors. If you’re too loose, your portfolio performance suffers. Success depends on mastering the “Three Cs” of subprime:

- Capacity: Does the borrower have the verifiable income to cover the payment after all other living expenses are met?

- Character: Does their recent history show a willingness to pay, even if their past credit score is low?

- Collateral: Is the vehicle’s value sufficient to protect your interest if a default occurs?

Mastering these fundamentals requires modern subprime auto finance software that can process these variables in real time, giving you the confidence to fund deals that others might miss.

Defining the Subprime Tiers for Modern Lenders

Lenders generally categorize high-risk applicants into two main buckets: Deep Subprime (scores below 580) and Subprime (580 to 619). Deep subprime requires the most rigorous verification and often carries the highest risk of early-stage delinquency. Subprime borrowers in the 580 to 619 range often include “credit rebuilders” who are highly motivated to stay current to improve their financial standing. Risk-based pricing is the core of subprime profitability, as it allows you to adjust interest rates and terms to match the specific risk level of each tier. In 2026, rising wages mean that a borrower with a 560 score might actually be more financially stable than a 620 borrower from two years ago.

The Shift from FICO to Holistic Risk Models

Traditional credit scores often fail to capture the “willingness to pay” in high-risk segments. A medical debt or a past divorce can tank a FICO score without reflecting a borrower’s current reliability or employment stability. This is especially true for “thin-file” borrowers who lack a long credit history. They represent a massive, untapped opportunity for lenders who can verify alternative data. To scale safely, you must establish a clear “credit box.” This involves setting hard limits for disqualifying events and soft limits where your subprime auto finance software can trigger a manual review or request a higher down payment to mitigate risk.

Leveraging Alternative Credit Data for High-Risk Borrowers

Traditional credit reports often hide more than they reveal. In the subprime space, relying solely on historical data is a recipe for high delinquency. Successful lenders in 2026 are shifting toward “Cash-flow Underwriting.” This method uses real-time bank statement data to see exactly how money moves in and out of a borrower’s account. It’s a proactive approach that prioritizes current financial behavior over past mistakes.

You need a broader view of the borrower’s life. Utility payments, rent history, and cell phone bills are now essential markers of reliability. These points demonstrate daily financial discipline better than a dormant credit card account might. The CFPB Supervisory Highlights underscore the importance of accurate data handling and transparency in these high-stakes segments. Beyond just the “Ability to Pay” (ATP), you should calculate “Residual Income.” This measures what’s left after all actual expenses, including the new car payment, to ensure the loan is truly sustainable for the borrower’s lifestyle.

Verifying Income and Employment (VOI/VOE)

Speed is your greatest asset. If you take three days to verify employment manually, the borrower has already signed a deal with a competitor. Digital verification is the only way to win in a competitive market. This is especially true for gig economy workers like Uber drivers or Etsy sellers. Their income isn’t on a W-2, so you must analyze 1099 streams and deposit patterns directly. Lenders in 2026 are increasingly leaning on the “Rule of 20,” which suggests that the auto payment itself shouldn’t exceed 20% of the borrower’s gross monthly income to maintain portfolio health. By leveraging subprime auto finance software, you can automate these complex calculations instantly.

The Power of Bank Account Aggregation

Modern subprime auto finance software allows you to look inside the bank account with the borrower’s permission. You can analyze the frequency of Non-Sufficient Funds (NSF) alerts to gauge real-time financial stress. This level of visibility also helps you spot “hidden” debt obligations, such as private personal loans or “Buy Now, Pay Later” commitments, that haven’t hit the major credit bureaus yet. Identifying income volatility early allows you to structure loan terms that actually fit the borrower’s reality. To streamline these complex checks, consider how an integrated loan management system can automate these data pulls and provide a clear risk score for your team.

Manual vs. Automated Underwriting: Balancing Speed and Precision

Speed to lead is the most critical factor in the 2026 subprime market. These borrowers rarely shop at just one dealership; they’re often applying at multiple lots simultaneously to see who can get them behind the wheel first. If your team takes hours or days to crunch numbers manually, you’ve already lost the deal. Algorithmic scoring within your subprime auto finance software provides an instant verdict, allowing you to capture the borrower’s attention while they’re still on your site or lot. This isn’t just about moving fast; it’s about maintaining consistency. Humans are prone to decision fatigue and subjective bias, while an algorithm applies your specific credit box rules to every application without fail.

Some lenders hesitate to adopt full automation because of the perceived software costs. It’s time to reframe that logic. A single failed loan that ends in a messy repossession can cost your business thousands of dollars in recovery fees, legal expenses, and asset depreciation. This California Law Review analysis highlights the systemic dangers of lax underwriting and the high price of portfolio failures. Investing in advanced subprime auto finance software is essentially an insurance policy against these catastrophic losses. By auto-decisioning the cleanest 20% of your subprime applications, you can clear the administrative deck and focus your staff’s energy on the more profitable, complex files.

When to Use Human Review in the Underwriting Process

Machines are excellent at processing raw data, but they can’t always account for human context. You should reserve manual review for “exception” cases where a borrower’s story doesn’t fit a standard mold, such as a high-earner with a temporary credit dip due to medical debt. This is where underwriter’s intuition becomes a competitive advantage. Your workflow should utilize a structured “Stipulation” (Stips) process. This ensures that your team clears specific hurdles, like verifying physical proof of residence or social proof, before the loan is funded. It’s about using technology to handle the heavy lifting so your experts can focus on the nuances of borrower character.

Integrating LMS and DMS for Seamless Workflow

To win in a high-speed lending environment, your systems must communicate without friction. Understanding what is dms and how it integrates with your loan management system (LMS) is vital for operational security. This direct data flow eliminates manual entry, which is the primary source of clerical risk and costly compliance errors. Cloud-based platforms allow your team to underwrite 24/7 from any location, ensuring you never miss a lead in a competitive national market. When your DMS and LMS work in tandem, you gain real-time visibility into the entire loan lifecycle, from the initial application to the final payment.

Post-Funding Risk Mitigation: Protecting the Collateral

A common mistake in subprime lending is believing that the risk assessment ends once the contract is signed and the vehicle leaves the lot. In reality, underwriting is a continuous lifecycle that requires constant vigilance until the final payment is made. Protecting your primary interest means shifting from a static “approval” mindset to an active “monitoring” strategy. By maintaining real-time visibility over the asset, you can effectively lower the risk premium on individual loans and increase your overall portfolio yield. Modern subprime auto finance software acts as your eyes and ears, alerting you to changes in collateral status before they become expensive losses.

Insurance verification is the cornerstone of this post-funding strategy. Without full coverage, your collateral is one accident away from becoming a total loss with zero recovery. Traditional lenders often rely on manual checks that are outdated the moment they’re completed. To stay secure, you need a system that integrates directly with carrier data to provide live updates. This proactive stance allows you to intervene early, ensuring the borrower remains compliant with the terms of their agreement throughout the life of the loan.

Real-Time Insurance Monitoring

Subprime borrowers frequently face financial pressure that leads them to drop full coverage shortly after funding. This creates a massive “insurance gap” that puts your capital at risk. You can’t wait for a physical mailer to arrive to find out a policy has lapsed. Automating the “Notice of Cancellation” process via your subprime auto finance software ensures you’re notified the instant a policy is flagged for non-payment. For a deeper look at the technical steps involved in this process, read our guide on what is collateral protection insurance and how it streamlines your operations.

Implementing Collateral Protection Insurance (CPI)

Collateral Protection Insurance (CPI) serves as a vital safety net for your subprime portfolio. It allows you to approve riskier borrowers who might otherwise be declined, because you have a guaranteed mechanism to protect the underlying asset’s value. Implementing a CPI program requires careful attention to compliance, as you must navigate a patchwork of state and national regulations regarding lender-placed insurance. When managed correctly, these programs significantly reduce charge-offs and provide a layer of stability that manual tracking simply cannot match. If you’re ready to secure your portfolio with automated protection, explore our insurance tracking solutions to see the difference for yourself.

Modernizing Your Underwriting with Verifacto Subprime Auto Finance Software

Verifacto acts as the essential bridge between aggressive underwriting and safe portfolio management. In the 2026 lending environment, you can’t afford to choose between volume and security. Our integrated LMS and DMS platform provides real-time data visibility across the entire loan lifecycle, ensuring you never fly blind when assessing a high-risk applicant. By centralizing your operations, you eliminate the fragmented data silos that lead to missed risks and clerical errors. This subprime auto finance software is built to give you the stability you need to grow your portfolio with total confidence.

Success in 2026 requires a shift toward data-backed decision-making. You need a partner that understands the high-stakes nature of subprime lending and provides the tools to navigate it safely. Verifacto doesn’t just provide a database; it provides a comprehensive risk mitigation engine. From the moment an application is received to the final payment, our system works to protect your capital and optimize your yield. It is the modern solution for lenders who demand both speed and precision in their daily operations.

Streamlining Stips and Document Collection

Collecting paystubs, utility bills, and insurance documents is often the slowest part of the underwriting process. Verifacto’s automated borrower communication tools change that dynamic. You can send automated, branded requests that allow borrowers to upload their “stips” directly from their mobile devices. This drastically reduces your “time-to-fund,” which keeps your dealer partners happy and prevents borrowers from wandering to a competitor. Faster funding means more deals closed and a more efficient team. For a broader look at maintaining these assets after the deal is funded, see our strategy guide on improving collection efficiency for auto loans.

The Verifacto Advantage: Integrated Insurance Tracking

What truly sets Verifacto apart is the deep integration of insurance tracking and CPI solutions directly into the core subprime auto finance software. Most platforms treat insurance as an external plugin or a manual checklist item. We treat it as a fundamental part of your risk management box. By monitoring policy status in real time, we remove the “insurance gap” risk that often leads to catastrophic portfolio losses. You get the peace of mind that comes from a platform designed specifically for the unique requirements of high-risk auto finance. It’s time to stop guessing and start leading with a system built for protection. Modernize your underwriting with Verifacto today and take control of your portfolio’s future.

Secure Your Competitive Edge in the 2026 Subprime Market

Modern subprime lending requires a decisive shift from defensive caution to strategic precision. You’ve seen how holistic risk models and alternative cash-flow data reveal profitable opportunities that traditional credit scores often miss. By balancing automated speed with targeted human review, you can capture high-quality leads while maintaining a rigorous credit box. The risk lifecycle doesn’t end at funding; continuous collateral monitoring remains the final piece of the long-term profitability puzzle.

Implementing a specialized subprime auto finance software is the most effective way to unify these strategies into a single, high-performance workflow. Verifacto provides the security you need through real-time insurance tracking and automated borrower communication that significantly accelerates your time-to-fund. Our cloud-based LMS and DMS solutions are built specifically for the unique, high-stakes demands of auto finance professionals. You don’t have to choose between aggressive growth and portfolio stability.

Scale your subprime portfolio safely with Verifacto’s integrated LMS and DMS. It’s time to replace operational anxiety with data-backed confidence and drive your business toward a more secure and profitable future.

Frequently Asked Questions

What is the minimum credit score for a subprime auto loan in 2026?

The minimum credit score for a subprime loan typically starts at 580, though deep subprime lenders frequently fund applicants with scores as low as 450. In many cases, “thin-file” borrowers with no score at all can secure financing if they show strong stability metrics. The industry has shifted its focus from the three-digit score to current cash flow and verifiable employment history to determine creditworthiness.

How do alternative data points improve subprime underwriting accuracy?

Alternative data points improve accuracy by providing a real-time window into a borrower’s daily financial discipline. By analyzing rent history, utility payments, and cell phone bills, you can identify reliable payers who have been unfairly penalized by traditional credit models. This holistic approach reduces your default risk by verifying “willingness to pay” through consistent, non-traditional payment behaviors that FICO often ignores.

What is the difference between DTI and PTI in auto lending?

DTI (Debt-to-Income) represents the percentage of a borrower’s gross monthly income that goes toward all recurring debt payments, including housing and credit cards. In contrast, PTI (Payment-to-Income) focuses strictly on the proposed auto loan payment relative to their gross income. While DTI shows the total financial burden, PTI helps you determine if the specific vehicle payment is sustainable within the borrower’s monthly budget.

Can I automate underwriting for Buy-Here-Pay-Here (BHPH) dealerships?

You can absolutely automate underwriting for Buy-Here-Pay-Here (BHPH) operations to improve both speed and decision consistency. Implementing subprime auto finance software allows you to set “hard” and “soft” rules within your credit box, auto-approving your strongest applicants instantly. This frees your staff to focus on complex manual reviews where human intuition adds the most value to the high-risk decision process.

What are the common compliance risks when underwriting subprime loans?

Common compliance risks include “disparate impact” in risk-based pricing and failure to meet evolving state-level regulations, such as the California CARS Act. Lenders must also ensure they are accurately reporting passenger vehicle loan interest statements by the January 31, 2026, deadline. Maintaining transparent, data-backed underwriting workflows is the best way to mitigate these legal threats and ensure your portfolio remains audit-ready.

How does real-time insurance tracking lower my portfolio risk?

Real-time insurance tracking lowers risk by eliminating the “insurance gap” that occurs when a borrower drops coverage immediately after funding. Your subprime auto finance software monitors policy status 24/7 and alerts you the moment a cancellation notice is issued by the carrier. This allows you to secure the asset through CPI or proactive borrower outreach before a total loss occurs without any insurance recovery.

What is the best way to verify income for gig-economy workers?

The best way to verify income for gig-economy workers is through bank account aggregation and digital deposit analysis. Since these borrowers lack traditional W-2 paystubs, you must look at the consistency of their 1099 income streams over a 90-day period. This method provides a clear view of their “Ability to Pay” (ATP) and identifies any income volatility that might affect the loan’s long-term performance.

Is lender-placed insurance (CPI) legal for subprime loans?

Lender-placed insurance, or CPI, is legal for subprime loans as long as you adhere to specific federal and state disclosure requirements. It serves as a necessary safety net to protect your collateral when a borrower fails to maintain contractually required full coverage. Most states require you to provide the borrower with multiple notifications and the opportunity to reinstate their own policy before any CPI premium is added.