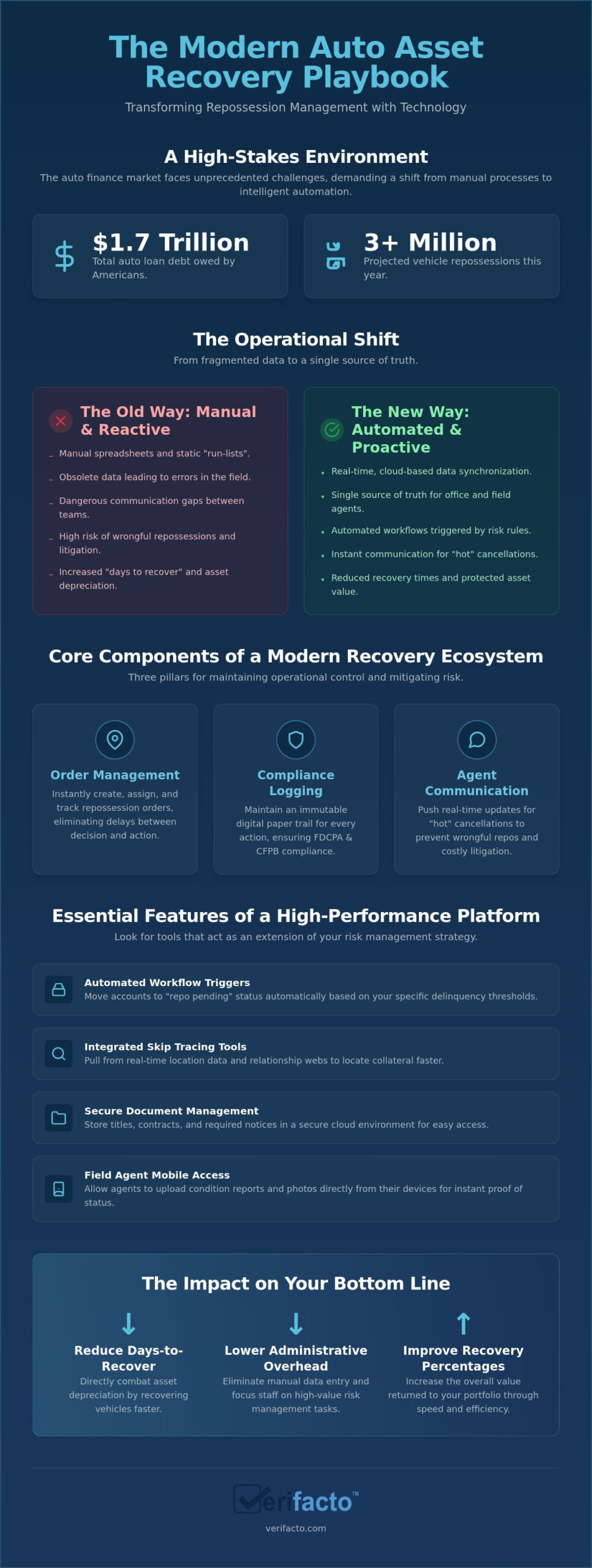

Americans now owe nearly $1.7 trillion in auto loan debt, and with repossessions projected to exceed 3 million vehicles this year, your recovery department is likely feeling the strain. It’s a high-stakes environment where a single compliance error or a day of lost communication can cost thousands. Implementing a robust repossession management software isn’t just about finding the car; it’s about building a proactive command center that protects your portfolio before the tow truck is even dispatched.

You’ve likely dealt with the frustration of uninsured collateral at the time of default or the high cost of physical recovery when a simple notification might have cured the loan. We understand that these operational hurdles create unnecessary anxiety for even the most seasoned lenders. This guide provides a comprehensive look at how modern software streamlines asset recovery, ensures 100% compliance with state and federal laws, and automates borrower outreach to prevent defaults. We’ll show you how to reduce days-to-recovery and maintain total control over your assets in a volatile market.

Key Takeaways

- Learn how to transition from manual spreadsheets to real-time, cloud-based data synchronization to ensure your recovery team always has the most current account information.

- Discover the essential features of high-performance repossession management software, including automated workflow triggers that flag delinquent accounts based on your specific risk rules.

- Understand the critical link between real-time insurance tracking and asset recovery to prevent the “double loss” of a defaulted loan on an uninsured or totaled vehicle.

- Identify the core differences between lender-centric and agent-centric platforms to choose a scalable solution that aligns with your specific portfolio management goals.

- Explore how integrating your LMS and DMS technology can automate borrower communications and safeguard your dealership from costly compliance litigation during the recovery phase.

What is Repossession Management Software and Why is it Critical in 2026?

Modern repossession management software is a centralized digital platform that manages the entire lifecycle of asset recovery, from the initial moment of default through the final auction. For years, lenders struggled with fragmented systems, relying on manual spreadsheets and static “run-lists” that were often obsolete by the time a field agent arrived at a location. This lag created dangerous communication gaps and increased the likelihood of errors. Today, the industry has transitioned to real-time, cloud-based data synchronization. This shift ensures that your internal collections team and your external recovery agents operate from a single source of truth at all times.

With 2026 projections suggesting completed repossessions could exceed 3 million vehicles, lender liquidity depends on speed. Market volatility means you can’t afford to let assets sit in “recovery limbo” while their value drops. Automated tools are no longer a luxury; they’re a requirement for maintaining a healthy balance sheet. By bridging the gap between your office and the field, these platforms allow you to act decisively the moment a loan enters the default phase. You gain the “no-nonsense” operational control needed to handle high-volume assignments without increasing your headcount.

The Core Components of a Recovery Ecosystem

A high-functioning recovery ecosystem relies on three specific pillars to maintain operational control and protect your dealership’s interests:

- Order Management: You can instantly create, assign, and track Repossession orders. This eliminates the delay between deciding to recover an asset and getting an agent on the job.

- Compliance Logging: The software maintains an immutable digital paper trail for every action taken. This is essential for meeting FDCPA and CFPB standards, effectively serving as your primary tool for auto finance compliance management.

- Agent Communication: Real-time updates allow for “hot” cancellations. If a borrower makes a last-minute payment, you can stop the agent immediately, preventing the “wrongful repo” scenarios that frequently trigger costly litigation.

The Impact on Your Bottom Line

Speed is the most critical factor in asset recovery. Every extra day a vehicle remains in the field is a day of lost value and increased risk. By reducing “days to recover,” you directly combat asset depreciation and improve your overall recovery percentages. These platforms also lower administrative overhead by eliminating the friction of manual data entry between your DMS and external repo tools. You stop paying your staff to move data and start paying them to manage portfolio risk. Repossession management software is an essential risk-mitigation layer for modern auto finance.

Essential Features of a High-Performance Recovery Platform

Selecting the right repossession management software requires looking beyond basic logistics. While routing and dispatch are important, a high-performance platform acts as an extension of your risk management strategy. It must provide integrated skip tracing tools that pull from real-time location data and relationship webs. This allows your team to locate collateral faster, reducing the time an asset spends depreciating in the field while it remains unrecovered.

Automation is the heartbeat of modern recovery. You should be able to set automated workflow triggers that move accounts to “repo pending” status the moment they hit your specific delinquency thresholds. This eliminates the “wait and see” approach that often leads to total losses. Additionally, a secure cloud environment for document management is non-negotiable. Storing titles, contracts, and required notices in one place ensures your agents have the legal authority they need to act. Field agents also require mobile accessibility. They need to upload condition reports and high-resolution photos directly from their devices to provide instant proof of asset status and condition.

Data Integration: Why Siloed Systems Fail

Many lenders make the mistake of using separate software for loan servicing and recovery. This disconnect is where errors happen and costs skyrocket. Your auto loan management software should feed data directly into your recovery orders without manual intervention. If a borrower makes a payment at 2:00 PM, the repo order must be cancelled by 2:01 PM. A lack of synchronization often leads to “wrongful repos,” which are a primary source of legal friction.

Failure to sync this data in real time creates massive legal liability. You must respect consumer rights in vehicle repossession to avoid “breach of peace” claims or wrongful seizure lawsuits. When your systems talk to each other, you protect your dealership from the reputational and financial damage of a botched recovery. If you’re looking to unify these processes, exploring an integrated LMS and DMS solution is the most effective way to close these operational gaps and ensure your data remains accurate.

Reporting and Analytics for Portfolio Health

Data-driven lenders use their recovery platform to analyze more than just individual assignments. You need to track agent performance metrics like recovery rates, average fees, and time-to-pickup. This allows you to allocate your most difficult assignments to your most efficient partners, maximizing your return on investment. It’s about moving from reactive fire-fighting to proactive portfolio management.

Beyond agent metrics, use geographic hotspots to identify where defaults are spiking. This intelligence helps you adjust your lending criteria in specific regions to mitigate future risk before it impacts your bottom line. Compliance auditing also becomes a streamlined task rather than a week-long project. Instead of digging through filing cabinets, you can generate one-click reports for regulatory examinations, proving that every notice was sent and every law was followed during the recovery process.

The Critical Link Between Insurance Tracking and Asset Recovery

A missed payment is only half the battle. The true nightmare for any lender is the “Double Loss” scenario: a borrower defaults on their loan while simultaneously letting their insurance lapse on a vehicle that ends up totaled. When this happens, you aren’t just losing the interest; you’re losing the underlying collateral itself. High-performance repossession management software must integrate insurance monitoring to close this gap. By identifying high-risk accounts the moment a policy cancels, you can act weeks before the account hits the 60-day delinquency mark.

Real-time insurance tracking acts as an early warning system. Industry data suggests that borrowers often stop paying their insurance premiums before they stop paying their car notes. Automated systems detect these lapses and trigger immediate borrower notifications. This “soft” collection touchpoint often resolves the issue before a physical recovery becomes necessary. If the borrower fails to provide proof of coverage, your system should automatically transition the account into your recovery workflow, ensuring you never have an uninsured asset on the road.

Preventative Management via Insurance Monitoring

Understanding what is collateral protection insurance is vital for any lender looking to mitigate risk. CPI serves as a leading indicator for repossession risk; if a borrower can’t afford insurance, they likely can’t afford the vehicle. Verifacto’s platform creates a seamless synergy between insurance tracking and recovery management. When a lapse is detected, the system doesn’t just send a letter. It updates the account status in real time, allowing you to deploy CPI as a financial buffer while you evaluate the next steps in the recovery process.

Mitigating Risk During the Recovery Phase

Risk doesn’t end once the repo order is assigned. You must ensure the vehicle remains protected while it’s in the possession of a third-party agent or sitting in a storage lot. Compliance with Federal Trade Commission guidelines is essential here to protect your dealership from liability during the transition. If an agent recovers a vehicle in a damaged condition, having an integrated system allows you to file insurance claims immediately, preserving the asset’s liquidation value.

Automated insurance verification reduces the probability of uncollateralized charge-offs by ensuring every active loan is backed by a verifiable policy or an active CPI placement. This proactive approach transforms your repossession management software from a simple tracking tool into a comprehensive risk-mitigation engine. It’s about protecting your portfolio from the unpredictable realities of the 2026 market.

Choosing the Right Software: Logistics vs. Portfolio Management

Choosing the right repossession management software requires a clear understanding of your operational goals. Many platforms on the market are agent-centric, focusing on the tactical needs of the tow truck driver. While these are useful for the field, they often lack the sophisticated financial controls that a lender requires. You need a platform built for portfolio management that provides a high-level view of your risk while allowing for granular control over individual assignments. It’s the difference between managing a truck and managing a multi-million dollar asset pool.

Scalability is a critical litmus test for any solution you consider. Your software should support your growth, whether you’re managing 50 cars or 5,000. In 2026, the stakes for data security are higher than ever. SOC2 compliance and robust data encryption are no longer optional features; they are foundational requirements. If a platform can’t guarantee the safety of your borrower’s data, it poses a significant threat to your dealership’s reputation and legal standing. You need a partner that understands the “no-nonsense” requirements of modern data protection.

The All-in-One Myth vs. Strategic Integration

Don’t be fooled by the promise of a single tool that handles every aspect of your business. The most effective strategy involves specialized integration. Your recovery software must communicate seamlessly with your DMS to ensure that your data is always current. This connectivity is essential for improving collection efficiency auto loans, allowing you to resolve delinquency through communication before resorting to repossession. When you calculate the ROI of your software, look beyond the monthly subscription fee. Consider the thousands of dollars saved through reduced charge-offs and avoided legal fees.

User Experience and Training

Software is only as good as the people who operate it. A steep learning curve can stall your recovery efforts and frustrate your staff. Rapid adoption requires an intuitive interface and a provider that offers proactive, partner-like support. You shouldn’t have to figure it out on your own. Your recovery workflow must also be customizable. Every state has unique laws regarding asset recovery, and your software should allow you to bake those rules directly into your automated processes. This level of tailoring ensures you remain compliant while moving at the speed of the market.

To see how a truly lender-centric platform can protect your assets, schedule a demo of Verifacto’s integrated technology today.

Verifacto: Streamlining Repossessions Through Integrated LMS and DMS Technology

Verifacto’s cloud-based platform removes the friction that traditionally stalls recovery efforts. By integrating the LMS and DMS into a single command center, the system eliminates the dangerous lag between a missed payment and a recovery order. This is repossession management software designed for the high-stakes realities of 2026. It gives you the power to act with precision, ensuring your recovery agents always have the most accurate data at their fingertips.

Dealers face constant regulatory pressure, and the transition from default to recovery is the most legally sensitive phase of the loan. Verifacto leverages auto finance compliance management tools to shield your business from litigation. Every action is logged, and every required notice is tracked, creating an airtight digital defense. This level of oversight is essential for maintaining stability in a market where a single compliance error can trigger a costly CFPB investigation.

While most tools focus solely on the “hunt,” Verifacto prioritizes the “cure.” Our Automated Borrower Communication uses SMS and email to resolve delinquencies before a tow truck is ever dispatched. This proactive approach saves thousands in recovery fees and preserves the borrower relationship. It represents a strategic shift from reactive chasing to proactive resolution. Verifacto acts as a reliable guardian for your portfolio, providing mastery-driven technology built for environments where security and speed are paramount.

The Verifacto Advantage for Independent Dealers

Built-in payment processing is a game-changer for independent dealers. If a borrower makes a last-minute payment to cure their delinquency, the system can immediately halt the recovery order. This prevents wrongful repossessions and the legal nightmares that follow. Our real-time dashboard provides a 360-degree view of your collateral status, modernizing the Buy Here Pay Here (BHPH) experience with no-nonsense tools. You stop guessing and start knowing exactly where your assets stand at any given moment.

Next Steps: Modernizing Your Recovery Strategy

Auditing your current default-to-repo timeline is the first step toward operational efficiency. You need to identify where communication breaks down and where data becomes siloed. Transitioning to a cloud-based system doesn’t have to mean operational downtime. It’s about upgrading your infrastructure to meet the demands of a modern portfolio. By automating the transition from insurance lapse to recovery, you protect your liquidity and your peace of mind.

Ready to secure your collateral? Explore the Verifacto Platform today.

Future-Proof Your Asset Recovery Strategy

Managing a high-volume portfolio in 2026 requires moving beyond reactive, manual processes. By integrating your loan servicing with real-time insurance tracking, you eliminate the visibility gaps that lead to uncollateralized charge-offs. This proactive approach ensures you identify high-risk accounts weeks before they require physical recovery. Choosing the right repossession management software is about more than just finding vehicles. It’s about building a resilient, data-driven command center that protects your dealership’s bottom line and ensures 100% compliance.

Verifacto has been a leader in the industry since 2014, providing a cloud-based LMS/DMS integration that streamlines every phase of the loan lifecycle. Our platform offers real-time insurance tracking and automated borrower communication to help you resolve delinquencies before repossession is even necessary. You don’t have to navigate these operational challenges alone. With the right tools and a partner-like advisor, you can reduce days-to-recovery and maintain total control over your assets in any market environment.

Optimize Your Recovery Workflow with Verifacto

Frequently Asked Questions

What is the difference between repossession management software and skip tracing?

Skip tracing is a tactical process focused specifically on locating a missing borrower or vehicle through data mining and public records. In contrast, repossession management software serves as the overarching operating system for the entire recovery lifecycle. It handles order assignment, agent communication, and compliance logging. While skip tracing finds the asset, the software ensures the recovery is legal, documented, and integrated with your loan management system.

How does repossession software help with CFPB compliance?

The software automates the creation of an immutable digital paper trail for every action taken on an account. This includes date-stamped logs of borrower notifications and agent updates, which are essential during a CFPB audit. By enforcing specific communication windows and ensuring all required state and federal notices are sent, the platform reduces the risk of violations related to unfair or deceptive practices.

Can I integrate repossession management with my existing DMS?

Yes, leading platforms are designed to synchronize directly with your Dealer Management System (DMS) to eliminate manual data entry. This integration ensures that when a payment is posted in the DMS, the recovery status is updated instantly across all channels. Using a unified system prevents the “silo effect” where recovery agents act on outdated information, which is a primary cause of wrongful repossession claims.

How much does repossession management software typically cost?

Pricing for these platforms varies based on your portfolio size and the specific features required, such as integrated insurance tracking or automated messaging. Most industry providers utilize either a monthly subscription fee or a per-transaction recovery fee model. You should evaluate the cost against the potential savings from reduced charge-offs and lower legal fees. Contact a provider directly to receive a tailored quote based on your volume.

Does the software communicate directly with recovery agents?

Modern platforms facilitate instant, two-way communication between your internal team and field agents via cloud-based portals or mobile apps. Agents can upload condition reports and photos immediately upon recovery, while you can send “stop” orders the moment a borrower cures their default. This real-time link is critical for operational speed and preventing the physical recovery of vehicles after a last-minute payment has been processed.

What happens if a borrower pays while the vehicle is being repossessed?

If a borrower makes a payment while an agent is in the field, the software triggers an immediate cancellation alert to the agent’s mobile device. This rapid synchronization is vital for avoiding wrongful repossession litigation. Because the system links your payment processing directly to the recovery order, the agent receives the stop-work notification in seconds, protecting your dealership from significant legal and reputational damage.

How does insurance tracking reduce repossession costs?

Insurance tracking identifies high-risk accounts before they reach deep delinquency, allowing for earlier “soft” interventions. By monitoring for policy lapses in real time, you can place Collateral Protection Insurance (CPI) to protect your financial interest. This early detection often allows you to resolve the issue through automated communication, avoiding the high physical costs associated with a full repossession and subsequent vehicle liquidation.

Is cloud-based repossession software secure for sensitive borrower data?

Cloud-based repossession management software uses enterprise-grade encryption and SOC2 compliance to protect sensitive borrower information. Unlike legacy paper-based systems or local spreadsheets, cloud platforms offer superior security through multi-factor authentication and role-based access controls. This ensures that only authorized personnel can view sensitive data, significantly reducing the risk of data breaches or unauthorized access to your portfolio records.