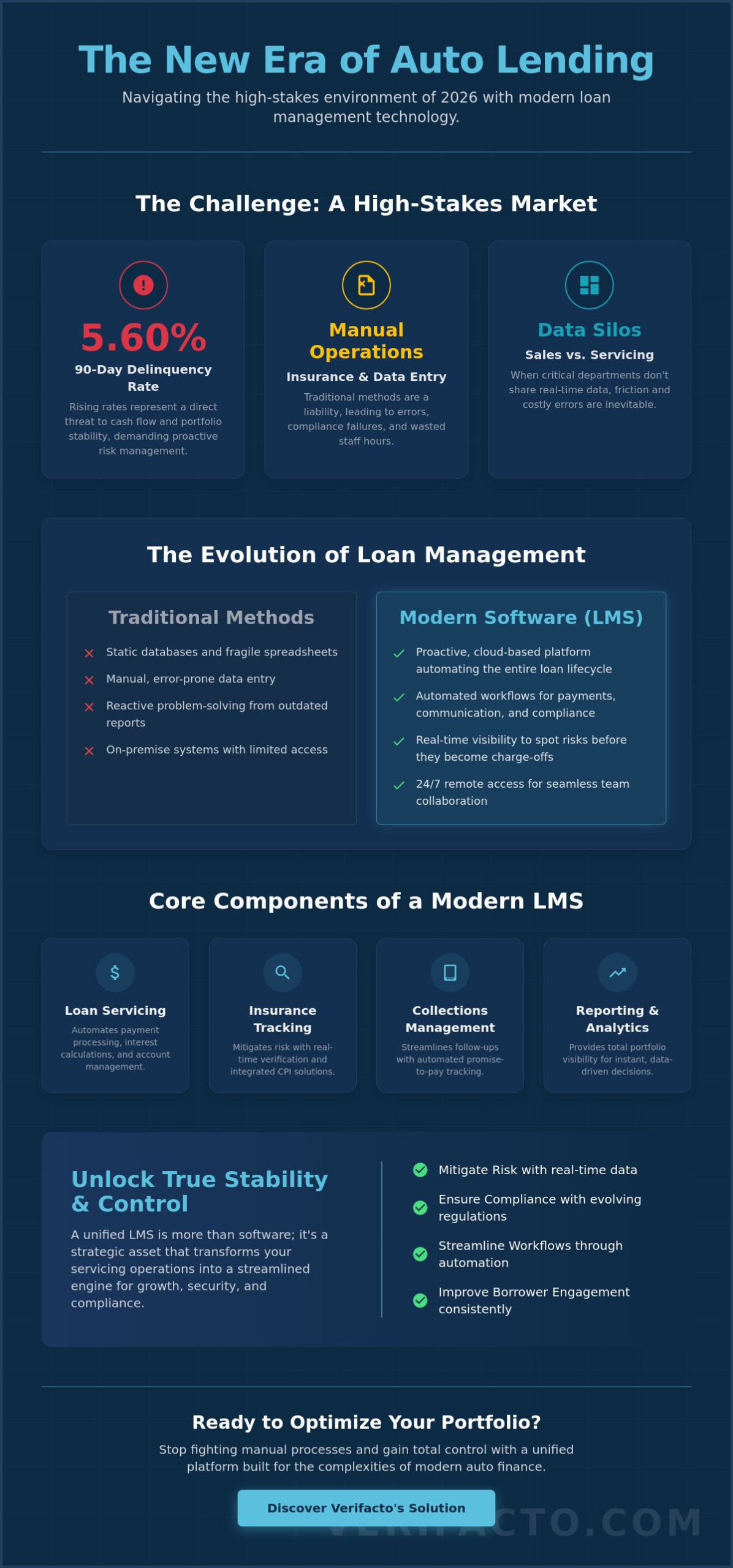

With 90-day auto loan delinquency rates hitting 5.60% in early 2026, the margin for operational error has disappeared. If you’re still fighting manual insurance verification bottlenecks or managing disjointed systems where your sales data doesn’t talk to your servicing team, you’re likely feeling the strain of rising charge-offs. It’s a high-stakes environment where traditional methods fall short of modern regulatory demands like the California CARS Act. Implementing the right auto loan management software is no longer optional for lenders who want to protect their portfolios and maintain a competitive edge.

We understand that the transition to more sophisticated technology can feel overwhelming, but it’s the only way to achieve true stability and control. This comprehensive guide promises to help you master the complexities of auto finance by showing you exactly how to select, implement, and optimize your loan management tech. We’ll preview the essential features of a unified system, from automated borrower communication to real-time portfolio visibility. By the end of this guide, you’ll have a clear strategy to reduce risk, ensure compliance with the latest IRS reporting rules, and turn your servicing operations into a streamlined engine for growth.

Key Takeaways

- Understand how modern auto loan management software has evolved from a static database into a proactive, cloud-based engine that automates the entire loan lifecycle.

- Discover how cloud-based architecture and automated communication triggers enable seamless remote collaboration and consistent borrower engagement.

- Learn to mitigate your highest risk by replacing manual insurance verification with real-time tracking and integrated CPI solutions.

- Identify the critical steps for a successful implementation, starting with a strategic audit of your current manual bottlenecks and data silos.

- Explore the operational advantages of a unified platform that syncs sales and servicing data to provide total portfolio visibility.

What is Auto Loan Management Software in 2026?

In 2026, auto loan management software isn’t just a digital ledger for tracking payments. It’s a sophisticated, cloud-based platform designed to automate the entire lifecycle of a vehicle loan, from the moment the contract is signed to the final payoff or repossession. Lenders have abandoned the static databases and fragile spreadsheets of the past because they simply can’t keep up with the volatility of a $1.67 trillion market. Modern systems move beyond simple record-keeping; they act as proactive guardians of your capital. This transformation is driven by the need for speed and the reality that manual data entry is a liability.

This technology is essential for maintaining portfolio liquidity. In an era where 90-day delinquency rates have climbed to 5.60%, every day a payment is late or a vehicle is uninsured represents a direct threat to your cash flow. A modern LMS provides the real-time visibility needed to spot these risks before they become charge-offs. Much like Fleet management software coordinates the complex logistics of vehicle maintenance and cost tracking for large fleets, an LMS coordinates the financial logistics of your collateral. It ensures that every asset is accounted for, properly insured, and performing according to the contract terms.

The Core Components of a Modern LMS

A robust system isn’t a single tool but a suite of integrated modules designed for speed. Loan servicing modules handle the heavy lifting of payment processing and interest calculation, ensuring accuracy even as rates fluctuate. Collections management tools have evolved to include automated promise-to-pay tracking, which reduces the manual workload on your staff and keeps communication consistent. Finally, integrated reporting dashboards provide a bird’s-eye view of portfolio health. This allows you to make data-driven decisions in seconds rather than waiting for month-end reports that are already outdated by the time they’re printed.

Why Independent Lenders Need Specialized Software

Independent lenders and “Buy Here, Pay Here” operators face unique challenges that traditional bank software often ignores. The industry has shifted from simple car sales to sophisticated finance models that require precision. Managing high-risk subprime portfolios means you don’t have room for error. You need automation to handle the high volume of borrower touchpoints and insurance verifications without ballooning your administrative headcount. Specialized auto loan management software allows you to meet strict state-level compliance requirements, such as the California CARS Act, without slowing down your operations. It provides the stability you need to grow your portfolio while keeping your risk profile under control.

The Mechanics of Modern Auto Lending Technology

Modern auto loan management software relies on a cloud-based architecture that provides 24/7 access to your portfolio from any location. This shift away from on-premise servers isn’t just a matter of convenience; it’s a strategic move to ensure data integrity across your entire team. When your sales and servicing departments work from the same real-time data, you eliminate the friction that leads to costly errors. Integrated payment processing further strengthens this foundation by supporting ACH, credit cards, and online portals, ensuring that borrowers have no excuses when it’s time to pay.

Security and compliance are baked into the core of these systems. As state and federal regulations evolve, your software must act as a filter that prevents illegal fees or mismanaged disclosures. Aligning your operations with the CFPB’s auto finance examination procedures is far simpler when your platform automatically logs every borrower interaction and payment change. This level of transparency protects your business from the “junk fee” scrutiny introduced by recent legislation like the New York FAIR Business Practices Act. It provides the security you need to operate in high-stakes environments without fear of regulatory pushback.

Streamlining the Servicing Workflow

Manual data entry is the enemy of scale. By automating recurring payments, you remove the human element that often results in misapplied funds or missed deadlines. Using modern technology for auto finance companies allows you to look beyond simple payment history to predict potential delinquency before it happens. This proactive approach simplifies payoff calculations and title release processes, moving vehicles through the lifecycle with minimal friction. If you’re looking to upgrade your current setup, exploring a unified Verifacto LMS can provide the streamlined workflow your team needs to handle higher volumes with less effort.

Automated Borrower Communication

In 2026, the most successful lenders use multi-channel communication to stay top-of-mind. Automated SMS and email triggers send reminders before a payment is due, which significantly reduces the need for aggressive collection calls later. These templates allow you to maintain a professional, partner-like tone that encourages borrower cooperation rather than defensiveness. By setting up automated touchpoints for upcoming and late payments, you ensure that no borrower falls through the cracks due to a busy schedule or simple forgetfulness. This systematic approach transforms collections from a reactive burden into a predictable, automated process that preserves the borrower relationship.

Mitigating Risk with Real-Time Insurance Tracking & CPI

The greatest threat to your portfolio isn’t just a borrower who misses a payment; it’s a vehicle that becomes a total loss while uninsured. While many lenders obsess over payment schedules, they often overlook the fact that their collateral is only as valuable as its insurance coverage. Relying on manual verification is a dangerous game. It involves a “nightmare” of faxes, phone calls to agents, and stacks of paper that are outdated by the time they’re filed. In 2026, sophisticated auto loan management software eliminates this vulnerability by integrating real-time insurance tracking directly into the servicing workflow.

Moving away from intermittent manual audits toward a framework of mitigating risk in auto lending ensures that you’re never in the dark about your assets. Instead of waiting for a repo agent to discover a lapsed policy, the system identifies coverage gaps the moment they happen. This shift from reactive to proactive management transforms the lender from a passive observer into a reliable guardian of their capital. It provides the security needed to navigate high-risk portfolios without the constant anxiety of an uninsured loss. By automating these checks, you free your team to focus on growth rather than chasing down insurance binders.

How Real-Time Insurance Tracking Works

This technology operates through continuous data feeds from insurance carriers, monitoring the status of every borrower’s policy in your portfolio. When a policy is canceled or lapses, the system generates an immediate alert. This early detection allows for faster intervention, reducing the need for aggressive auto loan default management later on. You can address the issue while the borrower is still communicative, rather than waiting until the vehicle is damaged or missing. It’s a precise, automated way to maintain the integrity of your collateral without increasing your staff’s workload.

The Role of CPI in Asset Protection

Collateral Protection Insurance (CPI) serves as the ultimate safety net when a borrower fails to maintain their own coverage. When your auto loan management software detects a lapse, it can trigger an automated notification process to the borrower, providing ample warning before force-placed insurance becomes necessary. If the gap remains, the system can automatically apply CPI to the account, ensuring the vehicle stays protected. This seamless integration ensures that your portfolio’s value remains stable, regardless of borrower negligence. It’s a strategic advantage that turns a potential total loss into a manageable, protected risk.

How to Evaluate and Implement an LMS Platform

Evaluating your options for auto loan management software is a high-stakes decision that dictates your operational efficiency for years. You must move beyond surface-level feature lists and look at how the technology actually solves your daily operational hurdles. We recommend a four-step process to ensure you select a platform that acts as a partner rather than just another vendor. Start by auditing your current manual bottlenecks; look specifically for data silos where your sales team and servicing team aren’t sharing real-time information. If your staff is manually re-entering data from the dealer system into the loan system, you’ve identified your first major liability.

Once you’ve identified the gaps, prioritize features like cloud based loan management system accessibility. In 2026, on-premise solutions are a relic of the past that limit your team’s ability to collaborate remotely and respond to borrower needs in real time. Next, evaluate the vendor’s support and training infrastructure. You shouldn’t need a robust internal IT team to manage your portfolio. The software should be intuitive enough for your collectors and managers to use with minimal friction. Finally, execute a phased data migration plan. Avoid the “big bang” approach; instead, migrate your data in segments to ensure business continuity and verify that every balance and interest calculation remains accurate during the transition.

Key Features to Look For

The most effective platforms offer seamless integration between the DMS and LMS environments, ensuring that when a deal is closed, the servicing lifecycle begins instantly without manual intervention. Look for robust reporting capabilities that satisfy both GAAP standards and the latest regulatory compliance requirements. Your software must be able to scale with you; if you double your portfolio size, you shouldn’t have to double your headcount. Scalability is the true test of a modern system’s value.

Overcoming Implementation Anxiety

Many lenders hesitate to switch because they fear the downtime associated with new technology. However, cloud-based systems offer a significantly faster ROI than legacy software because they require no hardware investment and offer immediate updates. Success starts with training your team to embrace streamlining auto finance operations with DMS integrations. When your staff sees how automation reduces their repetitive tasks, buy-in happens naturally. Measure your success by tracking the reduction in your cost-per-loan serviced; this metric will prove the value of your investment within the first few months of operation. If you are ready to modernize your workflow, get started with a modern LMS solution that prioritizes your growth.

Optimizing Your Portfolio with Verifacto’s Unified LMS & DMS

The true Verifacto advantage lies in bridging the gap between the showroom floor and the servicing desk. While most competitors treat the Dealer Management System (DMS) and the Loan Management System (LMS) as separate entities requiring complex API configurations, Verifacto provides a unified cloud-based platform. This integration eliminates the friction that typically occurs when sales data doesn’t align with servicing reality. When your team operates from a single environment, you remove the lag time and data entry errors that often lead to missed collection opportunities or compliance oversights. It’s a “no-nonsense” approach to auto loan management software that prioritizes operational speed and capital protection.

Leveraging built-in payment processing within this unified framework accelerates your cash flow immediately. You don’t have to wait for third-party reconciliations or deal with disjointed reports. Verifacto acts as your seasoned advisor in a high-stakes market, providing the tools to manage the entire loan lifecycle with precision. By consolidating your tech stack, you transform your business from a reactive operation into a proactive, data-driven enterprise. This is how modern lenders maintain stability even when economic pressures on borrowers increase.

Why Integration Beats Disjointed Systems

Fragmented systems create technical debt. Managing multiple software vendors means dealing with different support teams, varying update schedules, and potential points of failure. Verifacto provides one source of truth for borrower data, payment history, and insurance status. This clarity improves the borrower experience by ensuring that every interaction is based on accurate, up-to-the-minute information. A single, clear communication channel reduces confusion and builds trust, which is essential for maintaining high repayment rates in subprime portfolios. You gain total visibility into your portfolio health without the headache of manual data consolidation.

Take Action: Future-Proof Your Lending Operations

Modernizing your tech stack today is a competitive necessity. With auto lending fraud exposure reaching $10.4 billion in 2025, you can’t afford to rely on legacy tools that leave you vulnerable. Verifacto’s integrated insurance tracking and CPI solutions provide an unfair advantage by protecting your collateral automatically. You shouldn’t have to choose between growth and security. Our platform is designed to handle the high-volume requirements of 2026 lenders while maintaining the strict risk mitigation standards your portfolio requires. The time to streamline your operations and reduce your charge-offs is now. Schedule a demo to see how Verifacto can transform your servicing department into a high-efficiency engine for growth.

Modernize Your Lending Strategy for 2026

The lending landscape in 2026 demands a shift from reactive recovery to proactive protection. We’ve explored how moving away from manual bottlenecks and disjointed systems is the only way to stay ahead of rising delinquency rates. By implementing a unified auto loan management software, you gain the real-time visibility needed to secure your collateral and maintain steady cash flow. Transitioning to a cloud-based architecture isn’t just about efficiency; it’s about building a resilient foundation that can handle the pressures of a shifting regulatory environment.

Verifacto provides the sophisticated tools you need to act as a reliable guardian of your capital. Our cloud-based platform integrates LMS and DMS capabilities, offering real-time insurance tracking and automated borrower communication to eliminate the friction in your daily operations. You don’t have to navigate these high-stakes challenges alone. Streamline your auto finance operations with Verifacto today and take control of your portfolio’s growth. The path to a more secure, optimized lending business starts with the right technology. We’re ready to help you transform your operations into a high-efficiency engine for success.

Frequently Asked Questions

What is the difference between an LMS and a DMS in auto finance?

A DMS handles the front-end sales, inventory management, and contract printing, while an LMS manages the back-end servicing, payment processing, and collection lifecycle. Think of the DMS as the tool used to close the deal and the LMS as the system that protects the investment until the final payoff. Using a unified platform ensures that borrower data moves from the sale to the servicing phase without the errors caused by manual re-entry.

Can auto loan management software help reduce my delinquency rates?

Yes, this technology reduces delinquency by using automated communication triggers to keep borrowers engaged before a payment is missed. The software identifies accounts that are deviating from their typical payment patterns, allowing your team to intervene with proactive solutions. By keeping your loan top-of-mind through SMS and email reminders, you create a consistent payment culture that naturally lowers the number of accounts sliding into late-stage delinquency.

How does automated insurance tracking save money for lenders?

Automated tracking saves money by eliminating the administrative hours spent on manual verification and by preventing uninsured total losses. Instead of your staff calling agents to confirm coverage, the system monitors carrier data feeds in real time. This early detection allows you to address lapses before an accident occurs. It transforms a labor-intensive “nightmare” into a streamlined process that protects your collateral and reduces the need for expensive recovery efforts.

Is cloud-based loan management software secure enough for sensitive data?

Modern cloud platforms provide high-level security through advanced encryption and multi-factor authentication that typically surpass the capabilities of on-premise servers. These systems are designed specifically to meet financial data standards, ensuring that borrower PII and payment records remain protected. Regular, automated security updates mean your auto loan management software stays ahead of emerging cyber threats without requiring your team to manage complex IT infrastructure or manual patches.

Do I need special hardware to run modern auto loan management systems?

No, you don’t need any specialized hardware because these systems are cloud-based and accessible through a standard web browser. You can manage your entire portfolio using existing computers, laptops, or tablets with a reliable internet connection. This accessibility allows your team to collaborate from different locations and eliminates the need for expensive on-site servers, cooling systems, or dedicated IT maintenance staff to keep the software running smoothly.

How long does it typically take to implement a new LMS platform?

A typical implementation takes between 30 and 90 days, depending on the complexity of your data and the size of your portfolio. The process involves a structured audit of your current records, system configuration, and staff training. By using a phased migration plan, you can move your data in segments. This methodical approach ensures business continuity so that your daily collections and borrower servicing operations continue without interruption during the transition.

What are the compliance benefits of using specialized auto finance software?

Specialized software automates the creation of audit trails and ensures that every borrower disclosure meets current regulatory standards. It helps you stay aligned with shifting state and federal rules by logging every interaction and payment change automatically. This systematic approach reduces the risk of human error that leads to “junk fee” violations or illegal collection practices. It provides the documentation you need to pass audits and defend your business against legal challenges.

How does CPI integration work within the loan management system?

CPI integration works by automatically identifying coverage lapses and triggering a notification sequence to the borrower before force-placing a policy. If the borrower fails to provide proof of insurance within the required timeframe, the auto loan management software adds the premium to the loan balance. This ensures that your collateral is never left unprotected. The entire process is handled within the system, providing a seamless safety net that maintains the value of your portfolio.