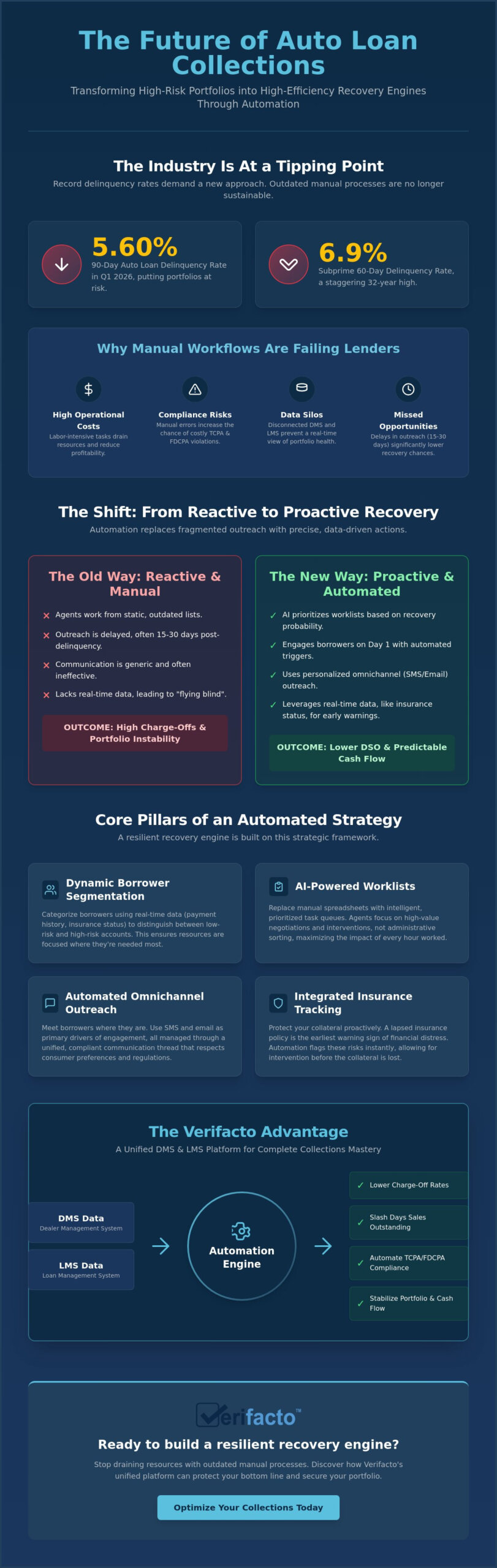

Did you know that 90-day auto loan delinquency rates hit 5.60% in the first quarter of 2026? For subprime lenders, the situation is even more critical, as 60-day delinquencies reached a 32-year high of 6.9% this past January. These record numbers mean that outdated, manual processes are no longer sustainable. If you haven’t yet shifted to auto loan collections automation, you’re likely struggling with high operational costs and the constant anxiety of TCPA or FDCPA compliance. It’s difficult to maintain control when you lack real-time visibility into borrower insurance status or payment stability.

We understand that managing these risks feels like an uphill climb. However, your collections department doesn’t have to be a drain on your resources. This guide will show you how to transform your operations into a high-efficiency recovery engine that protects your bottom line. We’ll explore how integrating insurance tracking with automated borrower communication can slash your DSO and significantly lower your charge-off rates. You’ll learn how to build a streamlined, compliant workflow that provides the stability and security your portfolio requires.

Key Takeaways

- Shift from manual, human-centric workflows to a system-led approach to reduce operational overhead and stabilize your recovery rates.

- Transform your strategy with auto loan collections automation by using dynamic segmentation to prioritize high-risk accounts and synchronize omnichannel outreach.

- Integrate real-time insurance tracking to identify early warning signs of default, allowing for proactive intervention before collateral is lost.

- Secure your operations against regulatory risk by automating communication schedules to strictly adhere to TCPA and FDCPA guidelines.

- Discover how a unified DMS and LMS platform provides a no-nonsense solution for modern lenders looking to optimize their recovery engine.

The Evolution of Auto Loan Collections: Why Manual Workflows Fail in 2026

Modern lending requires a shift from human-centric efforts to a system-led philosophy. We define auto loan collections automation as a synchronized approach to borrower engagement and risk mitigation. It isn’t just a set of tools; it’s a strategic engine that replaces fragmented, manual outreach with precise, data-driven actions. As market conditions tighten, the reliance on traditional methods has become a liability. To understand the current state of the industry, one must look at The Evolution of Auto Loan Collections and how it has transitioned from aggressive, manual tactics to sophisticated, automated workflows.

High interest rates and rising operational costs have made human-centric collection teams an expensive luxury. When your staff spends their day on administrative tasks rather than high-value negotiations, your recovery rates suffer. This inefficiency is often compounded by the “Data Silo” problem. If your Dealer Management System (DMS) and Loan Management System (LMS) don’t communicate in real time, you’re essentially flying blind. Mastery over these operational complexities requires cloud-based integration that bridges the gap between payment data and borrower communication.

The High Cost of Manual Delinquency Management

The 2026 Shift: From Reactive to Proactive Recovery

Proactive recovery is the new standard for 2026. This strategy uses specific data triggers to engage borrowers before a payment is even missed. By analyzing real-time data, you can predict borrower behavior and intervene with supportive solutions. For instance, a lapsed insurance policy is often the first sign of financial distress. Auto loan collections automation allows you to flag these risks instantly. Implementing integrated dealer management systems provides the technical foundation for this level of foresight. When your systems are unified, you move from reacting to crises to preventing them entirely, ensuring a more stable and predictable cash flow.

Core Pillars of an Automated Auto Finance Collection Strategy

Building a resilient recovery engine requires more than just software; it requires a strategic framework built on four essential pillars. The first is dynamic borrower segmentation. Not all delinquent accounts carry the same level of risk. By using auto loan collections automation, you can categorize borrowers based on real-time data like payment history and current insurance status. This allows your team to distinguish between a habitually late payer and a high-risk account where the collateral is no longer protected. When you segment your portfolio this way, you ensure that your most intensive resources are directed where they’re needed most.

The second pillar is the use of automated worklists. Traditional collection departments often rely on alphabetical lists or manual spreadsheets, which lead to agent burnout and inefficiency. Modern systems replace these with AI-prioritized tasks. Agents receive a queue of accounts ranked by the probability of recovery or the urgency of the risk. This shift empowers your staff to focus on high-value negotiations rather than administrative sorting. It’s a no-nonsense approach that maximizes the impact of every hour worked.

Omnichannel Communication: Meeting Borrowers Where They Are

In 2026, the traditional phone call is often the least effective way to reach a borrower. Most consumers now prefer digital-first interactions, making SMS and email the primary drivers of engagement. However, these channels shouldn’t exist in a vacuum. A unified communication thread is vital for maintaining Automation Ethics and ensuring your team has the full context of every conversation. Omnichannel automation is the synchronization of all digital touchpoints into one borrower profile. This level of integration prevents the fragmentation that often leads to compliance errors or frustrated borrowers.

Frictionless Payments: The “One-Click” Resolution

Outreach is only successful if it leads to a cure. If a borrower is ready to pay but faces a complicated login process or a required phone call, the window of opportunity might close. Implementing integrated payment solutions for dealers solves this problem by enabling immediate, one-click resolutions via mobile-friendly portals. When you remove the friction, you increase the likelihood of a successful transaction.

There’s also a significant psychological benefit to these tools. Many borrowers feel a sense of shame or anxiety when speaking to a collector. Self-service portals and automated ACH options allow them to resolve their delinquency privately and on their own schedule. This autonomy often leads to faster payments and lower late-stage delinquency rates. To see how these systems work together to protect your portfolio, you can explore how Automated Borrower Communication transforms the way you engage with your customers.

Protecting the Collateral: Linking Insurance Tracking to Collections

Effective auto loan collections automation doesn’t just manage conversations; it manages assets. Many platforms focus solely on conversational AI, but ignoring the vehicle’s status is a strategic mistake. A lapsed insurance policy is frequently the first indicator of financial instability. When a borrower stops paying their insurance premium, it’s a strong signal they’ll soon stop paying their loan. By integrating insurance data into your collection strategy, you gain a predictive advantage that traditional outreach lacks. It’s about moving beyond simple reminders and focusing on the underlying risk to the collateral.

This integration allows for sophisticated risk-based prioritization. Instead of working through a list chronologically, your team focuses on accounts where the collateral is exposed. An uninsured vehicle represents a total loss risk in the event of an accident or theft. Linking these data points ensures your collectors are working the highest-stakes accounts first. This transforms your recovery efforts into a surgical operation. You’re no longer just chasing payments; you’re actively guarding the value of your portfolio.

Real-Time Insurance Monitoring as a Collection Trigger

By tracking auto insurance on a loan portfolio, you create a proactive trigger for your team. The workflow is straightforward. Once an insurance lapse is detected, the system sends an automated notification to both the borrower and the collector. This immediate visibility allows for intervention before the situation escalates into a default. Maintaining insurance compliance is a direct reflection of a borrower’s overall financial stability. It’s a vital metric for any automated recovery engine that aims to be truly predictive.

Automated CPI Placement: Mitigating Financial Loss

When a borrower fails to maintain coverage, automated CPI placement acts as your final safety net. This mechanism ensures that every vehicle in your portfolio remains protected, regardless of the borrower’s actions. Automation handles the heavy lifting, from initial tracking to force-placing the policy when necessary. It’s important to follow all FDCPA guidelines when communicating these changes to borrowers. Proper notification schedules are built into the system, ensuring you remain compliant while protecting your capital. This no-nonsense approach guarantees that no vehicle is ever left vulnerable to an uninsured loss. You’re providing a layer of security that benefits both the lender and the borrower in high-stakes environments.

Navigating Compliance: TCPA, FDCPA, and Automation Ethics

Compliance isn’t just a legal checkbox; it’s the foundation of a sustainable collection strategy. When you implement auto loan collections automation, you’re essentially installing a digital guardian that never forgets a rule or misses a deadline. This proactive approach alleviates the professional anxiety associated with shifting regulatory environments. Instead of relying on manual oversight, you use system-led protocols to manage high-stakes requirements like “Time of Day” restrictions. Automation ensures your outreach only occurs during legally permitted hours, regardless of the borrower’s time zone. It’s a no-nonsense way to maintain stability while scaling your operations.

Handling “Opt-Outs” and “Stop” requests is another area where automation provides essential security. A single missed request can lead to costly litigation. Modern platforms automatically sync these preferences across all communication channels instantly. This level of precision creates a bulletproof audit trail. Every text, email, and automated call is recorded with a timestamp, providing you with the necessary documentation to defend your practices in any legal setting. You gain total control over your compliance posture without adding to your team’s administrative burden. This transparency is vital for protecting your capital and your reputation.

Mastering the TCPA in an Automated Environment

The Telephone Consumer Protection Act (TCPA) remains one of the most challenging hurdles for lenders. Rules regarding automated dialing and pre-recorded messages are strict, and the penalties for non-compliance are severe. Modern platforms manage borrower consent at scale, tracking opt-ins and opt-outs with surgical accuracy. You can’t afford to guess whether a borrower has given permission for a text message. For a comprehensive look at these requirements, review our auto finance compliance management checklist. This resource helps you safeguard your portfolio while maintaining an efficient outreach cadence.

Maintaining the “Human Touch” via Automation

Automation shouldn’t mean sounding like a robot. Effective auto loan collections automation uses templates that feel personal and supportive. The goal is to build a bridge back to payment, not to alienate the borrower. However, there are moments when a human touch is indispensable. A “Warm Handoff” occurs when the system detects a complex response or a specific risk level that requires a live agent. This balance allows you to remain assertive in your recovery efforts while providing the supportive reassurance that borrowers need during financial stress. By integrating these human elements into your automated workflow, you create a more resilient and respectful collection engine. To see how these compliant communication tools can work for your team, explore our Automated Borrower Communication solutions today.

The Verifacto Advantage: A Unified Platform for Collections Mastery

Navigating the complexities of the 2026 lending market requires a platform that does more than just track payments. Many generic collection tools fail because they operate in a vacuum, separated from the real-time data of your dealership operations. The Verifacto advantage lies in its ability to unify your workflow through a sophisticated blend of Auto Loan Management Software and a robust DMS. This integration ensures that your recovery efforts are always informed by the most current borrower and vehicle data. It’s a no-nonsense solution designed to move your department away from fragmented chaos and toward a state of operational mastery.

Our cloud-based implementation is built specifically for the high-stakes demands of the current market. Unlike legacy systems that require extensive hardware or long setup times, our platform is ready to scale with your business immediately. The inclusion of auto loan collections automation within this unified ecosystem means you can trigger outreach based on a variety of data points, from missed payments to lapsed insurance policies. While competitors might offer basic communication tools, Verifacto provides a comprehensive risk management engine that protects your capital at every stage of the loan lifecycle.

Streamlining Operations with Integrated LMS & DMS

Verifacto eliminates the friction of manual data entry between your sales and servicing teams. When a deal is closed in the DMS, the information flows directly into the LMS; this ensures that your collection agents have accurate data from day one. This transparency is a game-changer for CFOs and Portfolio Managers who require real-time reporting to make informed liquidity decisions. Additionally, our built-in payment processing allows borrowers to resolve delinquencies instantly. This closes the loop on recovery without requiring a single phone call, significantly reducing your operational overhead.

Ready to Automate Your Success?

Transforming your collections department from a cost center into a high-efficiency recovery engine is no longer a distant goal. You’ve seen how manual workflows fail in the face of rising delinquencies and how proactive, insurance-linked strategies can stabilize your portfolio. It’s time to replace professional anxiety with total control. We invite you to see our platform in action and discover how auto loan collections automation can secure your bottom line. Take the first step toward a more resilient future and Schedule a demo of Verifacto’s automated collection tools today. Modernize your portfolio management and ensure your recovery engine is built to last.

Master Your Recovery Strategy for 2026

The landscape of auto finance is changing rapidly. Relying on manual processes in a high-interest environment is a risk you don’t need to take. By adopting auto loan collections automation, you move beyond the limitations of human-centric teams and fragmented data. You’ve seen how real-time insurance tracking acts as an early warning system and why a unified LMS/DMS platform is the only way to eliminate data silos. These tools don’t just recover funds; they protect your entire portfolio from the ground up while ensuring every interaction remains strictly compliant.

It’s time to secure your operations with a partner who understands the high-stakes reality of modern lending. Verifacto provides the stability you need through cloud-based LMS/DMS integration, real-time insurance tracking with CPI solutions, and built-in compliant borrower communication. You can reduce your DSO and lower charge-off rates without sacrificing the human touch or operational control. Request a Verifacto Demo to Streamline Your Collections and see how a sophisticated recovery engine can transform your business. We’re ready to help you navigate these operational challenges with confidence and precision.

Frequently Asked Questions

How does auto loan collections automation improve recovery rates?

Automation improves recovery by ensuring immediate and consistent contact with every delinquent borrower. It eliminates the “missed windows” common in manual workflows by triggering outreach the moment a grace period ends. By using auto loan collections automation, you can prioritize accounts based on real-time risk data, ensuring your team focuses on the accounts most likely to result in a charge-off if left unaddressed.

Is automated debt collection compliant with the TCPA and FDCPA?

Yes, provided the system is built with integrated regulatory guardrails. Auto loan collections automation manages complex requirements like time-of-day restrictions and borrower consent tracking automatically. This reduces the risk of human error and provides a digital audit trail of every interaction, which is essential for defending your practices against potential legal challenges or regulatory inquiries.

Can I integrate automated collections with my existing DMS?

Integration is most effective when using a unified platform that bridges the gap between sales and servicing. Verifacto combines DMS and LMS capabilities to ensure that data flows seamlessly without manual entry. This connection allows your collection team to see the full history of the deal, including the original contract terms and real-time payment status, directly within their workflow.

What is the difference between generic collection software and auto-specific LMS?

Generic software focuses on simple communication, while an auto-specific LMS manages the unique risks associated with vehicle collateral. Auto-specific systems track vehicle-centric data points like insurance status and lienholder notifications. This specialized focus allows lenders to protect the underlying asset, which is a critical component of recovery that generic debt collection tools often ignore.

How does insurance tracking help in the collection process?

Insurance tracking serves as a primary indicator of a borrower’s financial stability. A lapse in coverage often occurs before a missed payment, providing your team with an early warning sign of potential default. By monitoring insurance in real time, you can intervene earlier in the delinquency cycle, protecting the collateral and increasing the likelihood of a successful payment cure.

What happens when a borrower opts out of automated text messages?

The system immediately halts all SMS outreach to that specific number and flags the account for alternative communication. This automated response ensures strict compliance with TCPA regulations. Your team can then shift to other approved channels, such as email or direct phone calls, without the risk of accidentally sending a prohibited text message that could lead to litigation.

Does automation replace the need for a collections team?

Automation doesn’t replace your team; it empowers them to work more efficiently. By handling repetitive administrative tasks like sending reminders and updating records, the system frees your staff to focus on high-priority negotiations. Your collectors can spend their time on complex borrower resolutions and high-risk accounts that require a personal, human touch to resolve successfully.

How long does it take to implement an automated collection system?

Implementation is efficient when using cloud-based solutions designed for modern lending. Most lenders can transition to an automated workflow within a matter of weeks. The process involves migrating your existing portfolio data and configuring your specific communication triggers. This fast-paced setup ensures you can begin optimizing your recovery engine and reducing your DSO with minimal disruption to your daily operations.