We understand that managing rising delinquencies while navigating new regulations like the California CARS Act feels like a constant uphill battle. It’s frustrating to deal with unprotected collateral simply because of poor communication or outdated systems. This guide will help you identify the specific tools needed to automate your collections and protect your bottom line. You’ll learn how to evaluate platforms based on their ability to provide a unified dashboard, real-time insurance monitoring, and automated borrower notifications. We’ll provide a clear roadmap to help you modernize your operations and scale with confidence in this challenging economic environment.

Key Takeaways

- Modernize your operations by moving from fragmented manual ledgers to a unified, cloud-based auto loan servicing platform that integrates the entire post-funding lifecycle.

- Discover how automated borrower communication and integrated payment processing can drastically reduce administrative overhead and streamline your collections workflow.

- Identify the critical risk-mitigation tools needed to protect your collateral from the multi-million dollar liability of lapsed insurance coverage.

- Learn how to manage a seamless data migration to the cloud, ensuring your team is fully trained on automated workflows without disrupting daily operations.

- Understand the competitive advantage of a unified LMS and DMS dashboard that offers real-time visibility into your portfolio’s health and insurance status.

What is an Auto Loan Servicing Platform and Why Does Integration Matter?

An auto loan servicing platform is a centralized, cloud-based system designed to manage every aspect of a vehicle loan once the deal is funded. In the high-interest environment of 2026, lenders can’t afford to treat servicing as a passive administrative task. It’s no longer just about tracking balances; it’s about deploying a proactive engine that automates collections and mitigates risk before losses occur. Loan servicing has evolved from simple payment collection into a complex operational strategy that requires real-time data to protect your capital.

A modern auto loan servicing platform functions as a unified hub that synchronizes payment processing, risk mitigation, and borrower communication into a single, actionable stream. For lenders, the core objectives are clear: reduce delinquencies, ensure compliance with shifting state regulations, and protect the physical collateral. Achieving these goals requires more than just a digital ledger. It requires a system that understands the relationship between a borrower’s payment behavior and their insurance status.

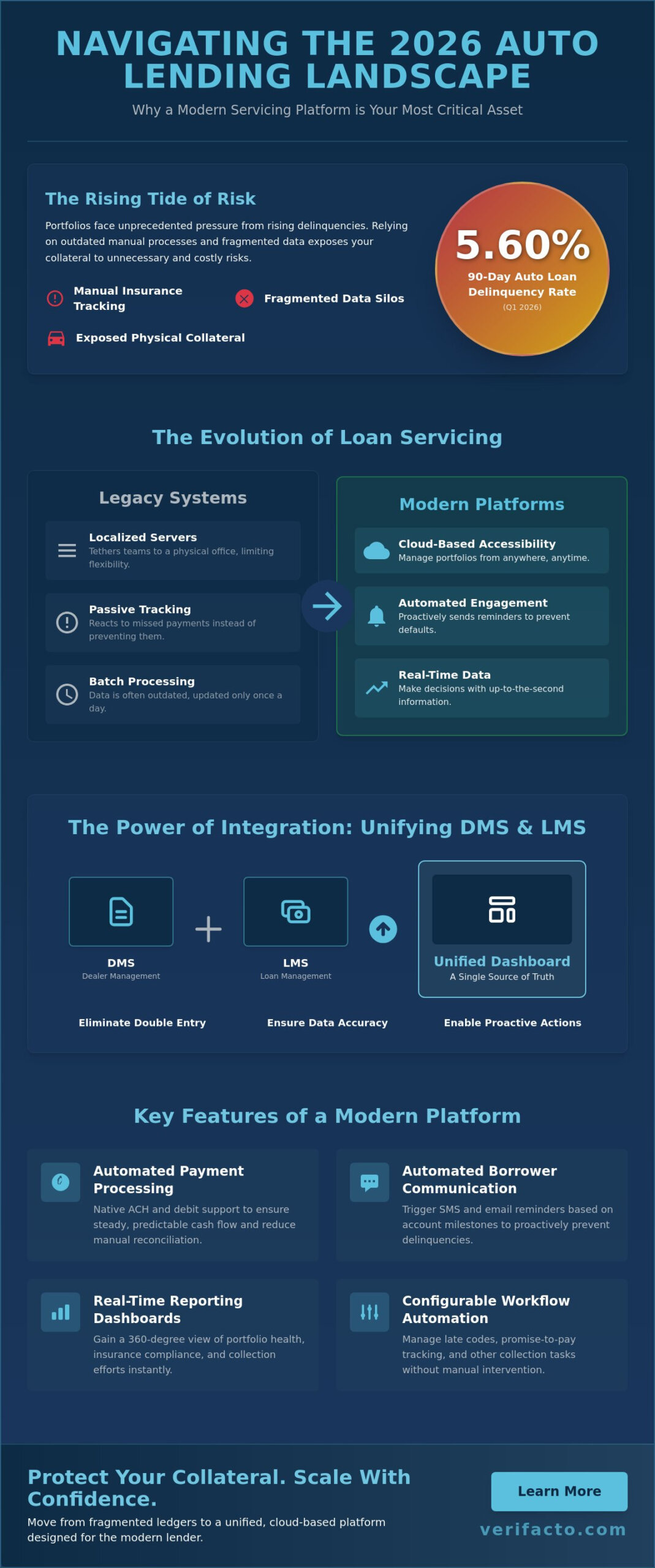

The Evolution of Loan Servicing Technology

The industry has moved away from localized servers that tethered teams to a physical office. Modern 2026 standards demand cloud-based accessibility that allows remote teams to manage portfolios from anywhere. Passive tracking, where a collector only reaches out after a missed payment, is now obsolete. Instead, technology enables automated borrower engagement, sending reminders before the due date to prevent defaults. While legacy systems relied on batch processing that only updated once a day, today’s platforms provide real-time data visibility, ensuring you’re never making decisions based on old information.

DMS vs. LMS: Why You Need Both in Sync

The transition from the sales floor to the servicing department is often where errors occur. Utilizing robust auto loan management software (LMS) alongside your Dealer Management System (DMS) ensures that data flows seamlessly without manual intervention. When these systems are in sync, you eliminate the “double entry” that plagues many independent dealers. This integration is vital for portfolio health because it maintains a single source of truth for every account. By connecting your DMS and LMS, you ensure that insurance updates, payment history, and borrower contact details are always current, reducing operational overhead and preventing costly communication gaps.

True integration means your auto loan servicing platform isn’t just receiving a data export once a week. It means the two systems communicate constantly. This level of synchronization allows for immediate action, such as triggering an automated notification the moment a borrower’s insurance policy lapses or a payment fails. This proactive approach is the only way to scale lending operations safely in a volatile market.

Key Features to Evaluate in a Servicing Platform

Choosing the right auto loan servicing platform isn’t about checking boxes on a generic feature list. It’s about selecting a tool that transforms your back office from a cost center into a risk-mitigation engine. In 2026, the distinction between a passive ledger and an active platform lies in its ability to automate the human elements of the lending business. Borrowers must be able to clearly identify their auto loan lender or servicer through consistent, branded touchpoints. Without this clarity, payment delays and borrower confusion become inevitable hurdles to your growth.

High-impact features to prioritize include:

- Automated payment processing with native ACH and debit support to ensure steady cash flow.

- Built-in borrower communication tools like SMS and email reminders that trigger based on specific account milestones.

- Real-time reporting dashboards that provide a 360-degree view of portfolio health and insurance compliance.

- Configurable workflow automation to manage late codes and promise-to-pay tracking without manual intervention.

Streamlining Collections with Automation

Efficiency is defined by how little manual effort your team spends on routine follow-ups. By focusing on improving collection efficiency auto loans, you can pivot your staff toward high-risk accounts while software handles the standard reminders. Automated SMS alerts sent three days before a due date keep the payment top-of-mind for the borrower. When a customer makes a commitment, promise tracking ensures no one slips through the cracks. The system monitors the deadline and alerts your team the moment a promised payment fails to materialize.

Modern Payment Solutions for 2026

Your liquidity depends on how easily your customers can pay you. Implementing integrated payment solutions for dealers removes the friction that often leads to defaults. Your auto loan servicing platform should support diverse preferences, including recurring ACH and branded online portals. If a borrower has to call your office during business hours to make a payment, you’re creating a barrier to your own revenue. Digital-first experiences are the standard. Offering a seamless, one-click payment environment encourages on-time behavior and builds long-term borrower trust.

True integration goes beyond simple data syncing; it requires your DMS and LMS to speak the same language in real-time. This prevents the double-entry errors that drain staff productivity and lead to compliance risks. If you want to see how a unified system can protect your collateral and scale your operations, view our integrated servicing solutions to see these features in action.

Risk Mitigation: Built-in Insurance Tracking and CPI

The most significant threat to your portfolio’s stability isn’t necessarily a missed payment; it’s the sudden loss of collateral that has no active insurance coverage. Manual insurance verification is a multi-million dollar liability for lenders who still rely on outdated spreadsheets and reactive phone calls. An advanced auto loan servicing platform must bridge the gap between loan management and real-time insurance status to prevent these catastrophic losses. This proactive approach aligns with the expectations found in the CFPB Examination Procedures, which emphasize the need for rigorous oversight of collateral protection and risk management practices.

Risk mitigation in 2026 requires more than just a ledger. It requires a system that alerts you the moment coverage drops, allowing you to take action before an accident occurs. By integrating insurance data directly into your servicing workflow, you transform your back office from a reactive department into a proactive risk-mitigation engine. This level of oversight ensures that your capital remains protected throughout the entire loan lifecycle.

Automating the Insurance Verification Loop

Lenders often fall into the trap of trusting the insurance binder provided at closing. However, policies can be canceled or lapse within days of the vehicle leaving the lot. Continuous coverage monitoring moves your operation beyond that initial “binder at closing” phase. An integrated auto loan servicing platform triggers automated borrower alerts the moment missing or canceled insurance is detected. This drastically reduces the “gap time” between a policy lapse and lender awareness, ensuring you’re never the last to know when your collateral is exposed.

The Value of Integrated CPI Solutions

When borrowers fail to maintain their own coverage, you need a reliable safety net. Understanding what is collateral protection insurance (CPI) is essential for any modern lender. Built-in CPI solutions allow you to place coverage on the collateral automatically when a lapse is detected. This ensures your interest is protected without requiring manual intervention from your staff. From a compliance standpoint, automated systems provide a clear audit trail of notifications and placements, reducing the legal risks associated with manual tracking and inconsistent enforcement.

By treating insurance tracking as a core pillar of your servicing strategy, you secure your assets and streamline your operations simultaneously. The result is a more resilient portfolio that can withstand the physical risks of the road while maintaining high standards of regulatory compliance.

Implementation: Transitioning to a Modern Servicing Platform

Moving to a new auto loan servicing platform often triggers anxiety about data loss and operational downtime. You shouldn’t let the fear of a messy transition keep you tethered to a legacy system that’s draining your efficiency. A structured implementation plan ensures that your portfolio moves into the cloud without losing a single borrower note or payment record. Transitioning is an opportunity to scrub your data, refine your workflows, and set a foundation for scalable growth in 2026.

Success depends on mapping your existing portfolio to the new environment with precision. Beyond the technical move, your team needs to understand how to leverage automated workflows rather than fighting against them. Staff training should focus on exception management, where employees only intervene when the software flags a specific issue. This shift in mindset allows your agency to handle higher loan volumes without a linear increase in headcount. Scalability is the ultimate goal. Your platform must handle 100 loans as easily as 10,000, providing the same level of oversight and security at every stage.

Steps for a Seamless Data Migration

Data integrity is the bedrock of your lending operation. Before the move, audit your current records for accuracy. Clean data prevents “garbage in, garbage out” scenarios that can lead to collection errors or compliance gaps. We recommend a phased rollout rather than a “big bang” approach. Start by migrating a small segment of your portfolio to verify that historical payment records and borrower notes import correctly. This testing phase allows you to resolve mapping issues before moving the bulk of your active loans, minimizing business disruption and protecting your cash flow.

Maintaining Compliance During the Switch

Regulations don’t pause while you upgrade your tech stack. You must verify that your new platform meets the rigorous 2026 standards for data privacy and consumer protection. Consult our auto finance compliance management guide to perform a thorough audit of your new software. Your platform should automatically handle state-specific lending regulations, such as those required by the California CARS Act, without manual configuration for every deal. Ensure that the system creates permanent, unalterable audit trails for all borrower communications. These digital footprints are your best defense during regulatory examinations or legal disputes.

Implementation is the bridge between your current limitations and your future potential. If you’re ready to leave manual processes behind and secure your portfolio with modern automation, contact our implementation team to start your migration plan today.

The Verifacto Solution: A Unified LMS and DMS for 2026

Verifacto provides the technological foundation required to navigate the high-stakes lending environment of 2026. While other providers offer fragmented tools that require complex workarounds, we’ve built a unified auto loan servicing platform that bridges the gap between sales and long-term portfolio management. By integrating Verifacto DMS and Verifacto LMS into a single cloud-based ecosystem, we eliminate the data silos that lead to communication breakdowns and unprotected collateral. This isn’t just about record-keeping; it’s about providing a command center for your entire operation.

Our solution treats Insurance Tracking and CPI Solutions as core pillars of the platform rather than optional add-ons. This ensures that your risk mitigation strategy is active from the moment a loan is funded. With Automated Borrower Communication and built-in Payment Processing, you can manage the full lifecycle of every account without switching between different software providers. This level of synchronization creates a seamless experience for both your team and your borrowers, fostering the trust and transparency needed to maintain high recovery rates.

Why Lenders Choose Verifacto for Risk Management

The primary advantage of the Verifacto ecosystem is the power of real-time visibility. Having your loan data and insurance status in a single dashboard allows you to spot vulnerabilities before they become losses. By automating routine tasks like insurance verification and payment reminders, many industry professionals using our tools report up to a 40% reduction in manual labor requirements. This efficiency gain allows independent dealers to scale their portfolios significantly without needing to hire additional staff. Our partners consistently find that having a “reliable guardian” in their tech stack provides the stability they need to grow in a volatile market.

This focus on operational health often leads lenders to audit their entire software environment for hidden costs. Using an AI-native platform like LicenseIQ to discover and recover wasted spend on Microsoft 365 licenses is another way modern firms are protecting their bottom line while scaling their business.

Getting Started with Your Modernized Platform

We believe that every lending operation has unique requirements, which is why we emphasize a partner-like approach to implementation. You won’t just receive a login and a manual. Instead, our team works with you to map your specific workflows and ensure a smooth transition from your legacy systems. We provide the support necessary to turn our automation features into tangible business outcomes for your agency. The best way to understand how these tools can protect your capital is to see them in action with your own data and processes.

Ready to protect your portfolio and eliminate the friction in your back office? Schedule a Verifacto demo today to see how our unified platform can transform your lending operations for 2026.

Secure Your Portfolio for the Future of Lending

The landscape of 2026 requires more than just reactive management; it demands a proactive engine that safeguards your assets while streamlining your operations. You’ve seen how a unified auto loan servicing platform eliminates the dangerous gaps between sales and servicing. By integrating real-time insurance tracking and automated borrower communication directly into your workflow, you move from a state of constant anxiety to one of total control.

Manual tracking and fragmented systems are no longer sustainable in a market with rising delinquency rates. It’s time to trade operational friction for a cloud-based solution that grows with your volume and enforces compliance automatically. Protecting your collateral doesn’t have to be a manual burden. With the right technology, you can automate the routine and focus your expertise on strategic growth.

Ready to transform your back office into a high-efficiency risk-mitigation engine? Streamline your portfolio with Verifacto’s integrated servicing platform today. Our solution offers built-in real-time insurance tracking, seamless cloud-based LMS/DMS integration, and automated borrower communication tools designed for modern lenders. Take the decisive step toward a more secure and profitable future.

Frequently Asked Questions

What is the difference between a DMS and an auto loan servicing platform?

A Dealer Management System (DMS) primarily focuses on the inventory and sales side of the transaction, while an auto loan servicing platform manages the post-funding lifecycle. The DMS handles the deal structure and paperwork. The servicing platform takes over to automate payments, monitor insurance, and handle borrower communications. Using an integrated system ensures data flows seamlessly between these two distinct phases without manual entry.

Can I track borrower insurance in real-time with a servicing platform?

Yes, real-time insurance tracking is a core feature of a modern auto loan servicing platform. Unlike legacy systems that rely on manual checks, these platforms monitor policy status continuously. You receive an immediate alert if a borrower’s coverage lapses or a policy is canceled. This allows you to take action, such as placing CPI, before your collateral is exposed to an accident without protection.

How does an auto loan servicing platform help with compliance?

These platforms standardize your processes to ensure every borrower receives the same disclosures and notifications required by law. Automated audit trails record every SMS, email, and payment attempt, which is vital for defending your practices during an examination. Modern systems also incorporate logic for state-specific regulations, like the California CARS Act, to help you stay compliant without manual oversight for every individual account.

Is it difficult to migrate my existing loan portfolio to a new platform?

Migration isn’t a hurdle when you follow a structured data mapping process. While moving years of historical data requires precision, a phased rollout minimizes business disruption. You start by auditing your current records and migrating a small batch to verify accuracy. This methodical approach prevents the data loss that lenders often fear, allowing you to transition to a more efficient environment without losing your portfolio’s history.

Do I need separate software for borrower text messaging?

You don’t need separate messaging software if you choose a platform with built-in borrower communication. Integrated tools allow you to trigger automated SMS or email reminders based on specific account events, such as a missed payment or an insurance lapse. This keeps all records in one place and ensures your collectors aren’t jumping between different apps to reach a borrower, which significantly improves operational speed.

How does integrated payment processing affect my cash flow?

Integrated payment processing accelerates your cash flow by removing the friction between the borrower and your bank account. By supporting ACH, debit cards, and online portals directly within the platform, you make it easier for customers to pay on time. Automated systems also handle recurring payments, which reduces the number of manual follow-ups your team needs to perform and ensures a more predictable stream of revenue.

What is the ROI of switching to an automated servicing system?

The ROI comes from three primary areas: reduced delinquency, lower labor costs, and collateral protection. Automating routine tasks can reduce manual labor by up to 40%, allowing your staff to focus on high-risk collections. Additionally, preventing even a single total-loss vehicle through real-time insurance tracking can save your agency thousands of dollars. These efficiencies combine to create a more resilient and profitable lending operation.

Can a small dealership afford an enterprise-grade servicing platform?

Modern cloud-based platforms are designed to be scalable, making them accessible to independent dealerships and large finance companies alike. The cost of the software is typically offset by the reduction in repossession fees, staff hours, and unprotected losses. Small dealers often see the biggest impact because automation allows a lean team to manage a growing portfolio with the same precision as a large enterprise.