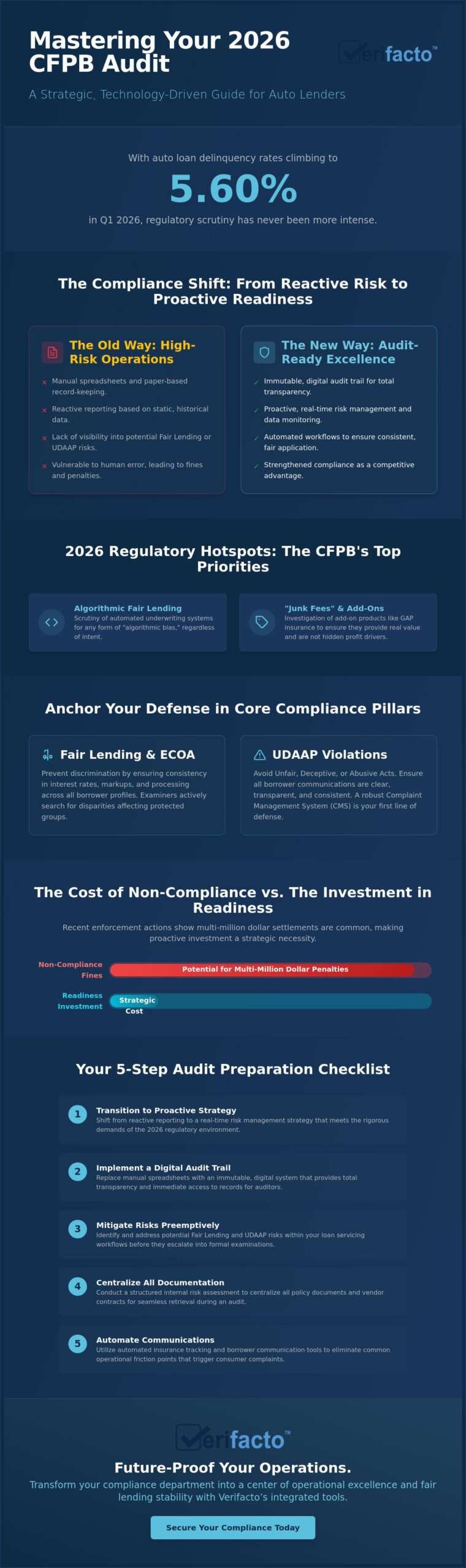

With auto loan delinquency rates climbing to 5.60% in the first quarter of 2026, the regulatory spotlight on your portfolio has never been more intense. You likely feel the pressure of maintaining perfect compliance while managing a growing segment of financially vulnerable customers. It’s a high-stakes environment where manual documentation and a lack of visibility into risk can lead to the very fines you’re working so hard to avoid. We understand that the recent shift in federal enforcement philosophy and the rise of state-level acts, like California’s CARS Act, create a complex landscape for your team to navigate.

The good news is that CFPB audit preparation for auto lenders doesn’t have to be an overwhelming manual burden. This guide provides a strategic, technology-driven approach to help you master regulatory examinations with confidence. You’ll learn how to streamline your record-keeping and secure a clean audit report through modern optimization. We’ll break down the 2026 regulatory updates, including the new Regulation Z and Regulation M thresholds, and show you how to transform your compliance department into a center of operational excellence and fair lending stability.

Key Takeaways

- Transition from reactive reporting to a proactive, real-time risk management strategy that meets the rigorous demands of the 2026 regulatory environment.

- Enhance your CFPB audit preparation for auto lenders by replacing manual spreadsheets with an immutable, digital audit trail for total transparency.

- Identify and mitigate potential Fair Lending and UDAAP risks within your loan servicing workflows before they escalate into formal examinations.

- Execute a structured internal risk assessment to centralize all policy documents and vendor contracts for immediate, seamless retrieval during an audit.

- Utilize automated insurance tracking and borrower communication tools to eliminate the common operational friction points that trigger consumer complaints.

The Evolving Landscape of CFPB Oversight for Auto Lenders in 2026

The regulatory environment has fundamentally shifted. For years, independent auto finance companies operated with significantly less oversight than traditional banking institutions. That era has ended. The Consumer Financial Protection Bureau (CFPB) has officially expanded its supervisory authority to include a broader range of non-bank auto lenders. This means CFPB audit preparation for auto lenders is now a core operational requirement rather than a periodic hurdle. It’s a proactive risk management strategy designed to protect your portfolio from the volatility of shifting federal and state standards.

In 2026, regulators have moved away from accepting static, historical reports. They now demand real-time data transparency. If your team relies on manual spreadsheets or paper files, you’re carrying unnecessary risk. Modern oversight requires the ability to demonstrate compliance at any given moment. You should view the Bureau’s “Supervisory Highlights” reports as your strategic roadmap. These publications detail the specific failures of other institutions, providing you with a clear list of what to avoid and what to optimize within your own workflows.

New Priorities: Algorithmic Fair Lending and Junk Fees

The Bureau’s focus has sharpened on the technology behind the loan. They’re actively hunting for “algorithmic bias” in automated underwriting systems. If your software inadvertently creates discriminatory patterns, your business is liable regardless of intent. Beyond underwriting, “junk fees” remain a top priority. Regulators are scrutinizing add-on products like GAP insurance and service contracts to ensure they provide actual value and aren’t just hidden profit drivers. Transparent pricing and clear fee disclosures are non-negotiable in the 2026 landscape.

The Cost of Non-Compliance vs. The Investment in Readiness

Recent enforcement actions have proven that the financial impact of non-compliance far outweighs the cost of modernizing your systems. Multi-million dollar settlements are becoming more common for lenders who fail to maintain accurate records or ignore borrower disputes. It’s time to move beyond the mindset that compliance is a “cost center.” Instead, view it as a strategic investment in your company’s longevity. Comprehensive audit readiness serves as a powerful competitive advantage for subprime lenders by building institutional trust and ensuring uninterrupted market access.

Core Compliance Pillars: Fair Lending and UDAAP Readiness

To build a resilient defense, you must anchor your operations in the two most critical pillars of federal oversight: the Equal Credit Opportunity Act (ECOA) and the prohibition of Unfair, Deceptive, or Abusive Acts or Practices (UDAAP). Effective CFPB audit preparation for auto lenders requires more than just a policy manual on a shelf. It demands proof that your lending practices are applied consistently across every borrower profile. Examiners look for disparities in interest rates, markups, and even the speed of loan processing to detect potential discrimination. If your data shows that certain protected groups are paying more for the same credit risk, your business is at immediate risk of a fair lending violation.

In the servicing phase, UDAAP risks often stem from a lack of clarity. If a borrower doesn’t understand their payment obligations or the consequences of a missed deadline, you’re vulnerable to unfairness or deception claims. Maintaining a robust Complaint Management System (CMS) is your primary defense. A well-organized CMS doesn’t just resolve issues; it acts as an early warning system, identifying operational friction before it attracts regulatory attention. According to recent 2026 Auto Finance Compliance Trends, data accuracy in collections and servicing remains a top priority for investigators. Consistent, automated borrower communication ensures that every customer receives the same disclosures at the same intervals, closing the gaps where UDAAP claims thrive.

Collateral Protection Insurance (CPI) and Compliance

Force-placed insurance is a major red flag during examinations. The Bureau frequently investigates whether lenders are adding CPI to accounts without providing adequate notice or when the borrower already has active coverage. To mitigate this risk, you must ensure total transparency. Before any premium is charged, send multiple clear notifications and consult a guide on what is collateral protection insurance to explain the cost and the borrower’s right to provide their own proof. If you want to eliminate the manual errors that lead to these red flags, automated insurance tracking can provide the real-time data you need to stay compliant.

Servicing Standards and Repossession Protocols

Documenting every interaction during the delinquency cycle is vital for successful CFPB audit preparation for auto lenders. Examiners will check if you applied grace periods and late fees consistently across your entire portfolio. Wrongful repossessions are a significant liability, often caused by outdated insurance data. By utilizing real-time insurance verification, you can prove that a repossession was justified and that all legal notices were delivered on time. This level of precision shows examiners that your business operates with integrity and control, turning a potential liability into a documented strength.

Technology’s Role in Audit Defense: Manual vs. Automated Precision

Manual record-keeping is no longer a viable option for high-growth lenders. Relying on fragmented spreadsheets or physical folders creates significant vulnerabilities during a regulatory review. It’s difficult to prove consistency when your data is scattered across different departments. In contrast, CFPB audit preparation for auto lenders becomes a seamless, defensible process when you utilize a cloud-based auto loan management software. This technology creates an immutable audit trail, tracking every modification and user action in real time. It eliminates the risk of human error or data tampering by providing objective, unalterable proof of your compliance efforts.

Data silos are the enemy of a clean audit report. When your Loan Management System (LMS) and Dealer Management System (DMS) don’t communicate, information gets lost in the gaps. Centralizing these data streams ensures that every document, from the initial credit application to the final payment receipt, is linked to the borrower’s master file. This level of organization allows you to grant examiners “read-only” access to your system. Instead of spending weeks digging through filing cabinets, examiners can find exactly what they need in minutes. This transparency builds immediate trust and significantly accelerates the review timeline, allowing your team to return to normal operations faster.

Automating Borrower Communications for Compliance

Automated systems ensure that every borrower receives mandated disclosures without exception. You cannot rely on staff to remember every notification requirement in a high-volume environment. By automating these workflows, you maintain timestamped logs of every text, email, and phone interaction. These logs serve as undeniable evidence that you followed federal communication standards. It’s about removing the variable of human error from the notification cycle. Your software handles the repetitive documentation, ensuring that every “right to cure” or “notice of intent” is sent and recorded perfectly.

Real-Time Insurance Tracking as a Compliance Shield

Stale data is a major liability during an audit of your portfolio. If your insurance records are only updated once a month, you’re likely making servicing decisions based on outdated information. This leads to improper CPI placement, which is a primary trigger for regulatory action. Automated insurance verification provides a constant stream of live data, acting as a digital shield for your business. By integrating insurance monitoring directly into your LMS workflow, the system automatically pauses CPI placement if it detects active coverage. This real-time precision proves to examiners that you have the controls in place to protect borrower interests.

A Step-by-Step CFPB Audit Preparation Checklist

Rigorous CFPB audit preparation for auto lenders involves a methodical review of every operational touchpoint. You cannot afford to wait for a formal Civil Investigative Demand to begin organizing your files. Start with a comprehensive internal risk assessment that spans all departments, from sales and underwriting to collections and remarketing. This proactive deep dive allows you to identify where your daily practices might have drifted from your written policies. If you discover a gap, you have the opportunity to correct it before an examiner arrives, demonstrating that your organization is a self-correcting entity with strong internal controls.

The next phase requires absolute centralization. You must gather all current policy documents, training manuals, and vendor contracts into a single, accessible digital repository. Examiners will specifically look for evidence of “disparate impact” in your pricing and underwriting data. Use your reporting tools to analyze your portfolio for any unintentional bias that could be flagged as discriminatory. Once your data is clean, perform a mock audit to stress-test your auto finance compliance management systems. Documenting the corrective actions taken during this mock run is a cornerstone of successful CFPB audit preparation for auto lenders, as it proves your commitment to ongoing improvement. If you need to streamline this process immediately, optimize your compliance workflows with our integrated management tools.

Organizing the “Exam Room” and Documentation

Preparation extends to the physical or virtual “exam room” where you will host regulators. You should have a standard set of Information Requests (SIRs) ready for immediate delivery. This includes your organizational charts, board meeting minutes, and detailed loan logs. Organize your sample loan files to present a clear “life of the loan” narrative. This chronological story should show the examiner exactly how the loan was originated, serviced, and communicated. Train your staff to be professional and concise. They should answer the examiner’s questions accurately without providing unsolicited information that could expand the scope of the review.

Vendor Management and Third-Party Oversight

Your regulatory responsibility does not end at your office door. You are legally accountable for the actions of your third-party service providers, including repossession agents and collection agencies. Review your service level agreements (SLAs) to ensure they contain specific compliance requirements and audit rights. You must be able to prove that your vendors follow the same UDAAP and fair lending standards that you do. Third-party technology providers must be vetted for data security and regulatory adherence. Regular monitoring of vendor performance is no longer optional; it is a fundamental requirement for maintaining a clean regulatory standing in 2026.

Future-Proofing Your Operations with Verifacto’s Integrated Tools

Mastering the complexities of 2026 regulatory standards requires more than just a well-documented policy. It requires an engine that executes those policies without fail. Verifacto’s integrated environment is designed to simplify CFPB audit preparation for auto lenders by replacing fragmented systems with a unified source of truth. Our cloud-based LMS and DMS platform automates the audit trail, capturing every interaction, payment, and disclosure in real time. This level of technological transparency allows you to position your finance company as a responsible provider, proving to examiners that your operations are built on a foundation of integrity and control.

One of the most powerful shields in your defense strategy is real-time insurance tracking. As we established earlier, improper CPI placement is the primary trigger for Bureau scrutiny. Verifacto’s system eliminates this risk by providing a constant stream of verified insurance data. If a borrower’s coverage is active, our platform prevents the automated placement of force-placed insurance, protecting both your portfolio and your reputation. Coupled with our automated borrower communication tools, you can ensure 100% disclosure consistency. Every customer receives the same required notifications at the exact right time, with every message logged and timestamped for immediate retrieval during an examination.

Built-in Compliance: From Underwriting to Payoff

Precision in your financial records is non-negotiable. Verifacto’s built-in payment processing ensures that every transaction is ledgered accurately, reducing the risk of UDAAP claims related to payment misapplication. This is particularly vital for subprime portfolios where delinquency rates are higher and regulatory eyes are sharper. Our platform reduces operational friction by automating the “no-nonsense” requirements of daily management. You get the benefits of a high compliance posture without the heavy manual lift, allowing your team to focus on growth while the software maintains the security of your audit trail.

Get Ready for Your Next Examination

The regulatory landscape will continue to shift, but your readiness doesn’t have to fluctuate. Partnering with an advisor who understands the intersection of auto finance and regulatory technology gives you a significant advantage. The first step toward modernization is moving away from the “compliance as a cost center” mindset and toward a model of automated efficiency. By adopting these tools, you turn CFPB audit preparation for auto lenders from a source of anxiety into a routine operational win. It is time to secure your portfolio and streamline your record-keeping for the long term.

Schedule a demo of Verifacto’s compliant LMS/DMS platform to see how we can modernize your audit defense.

Transform Your Audit Readiness into a Strategic Asset

You’ve seen how the 2026 regulatory environment demands a shift from static reporting to real-time data mastery. Success isn’t just about surviving an examination; it’s about building a business that operates with such transparency that audits become routine. By moving away from manual spreadsheets and centralizing your documentation, you eliminate the visibility gaps that lead to unintentional non-compliance. A proactive stance ensures your team is always prepared for scrutiny without disrupting daily operations.

Effective CFPB audit preparation for auto lenders requires a partner that bridges the gap between operational efficiency and regulatory security. You can’t afford the risks of stale insurance data or inconsistent borrower disclosures. Secure your portfolio with Verifacto’s compliant LMS and Insurance Tracking to gain total control over your audit trail. Our platform provides real-time insurance tracking to prevent wrongful CPI placement and maintains automated borrower communication logs for absolute disclosure consistency. An integrated LMS and DMS environment ensures that every loan narrative is complete and defensible. Take the first step toward a cleaner audit report and a more resilient business today. Your path to modern compliance starts with the right technology.

Frequently Asked Questions

What is the most common reason auto lenders fail a CFPB audit?

The most common reason for failure is the inability to provide a complete and consistent audit trail. Lenders often have strong written policies but fail to demonstrate that those policies are followed in every transaction. This lack of proof, often caused by fragmented manual data silos, makes it impossible to defend against claims of unfair or discriminatory practices during a review.

How much time do auto lenders typically have to prepare for a CFPB exam?

Auto lenders typically receive 30 to 60 days of advance notice before a scheduled supervisory examination begins. While this seems like a reasonable window, the volume of data requested is often staggering. Successful CFPB audit preparation for auto lenders relies on having these records organized and accessible long before the initial notification arrives to avoid operational panic.

Does the CFPB supervise small, independent “Buy Here Pay Here” dealers?

The CFPB officially supervises “larger participants” in the auto finance market, which generally includes those with at least 10,000 annual originations. However, smaller “Buy Here Pay Here” dealers aren’t immune to oversight. The Bureau maintains enforcement authority over all providers of consumer financial products. State attorneys general also frequently use CFPB standards to conduct their own local investigations into smaller operations, making it essential for every lender to maintain high compliance standards.

What is a “Civil Investigative Demand” (CID) and how is it different from an audit?

A Civil Investigative Demand (CID) is a formal administrative subpoena used during an enforcement investigation rather than a routine supervisory audit. While a standard audit is a proactive check of your compliance health, a CID indicates that the Bureau already suspects a specific legal violation. Responding to a CID is far more adversarial and requires immediate legal and technical coordination to manage the high stakes.

How can automated insurance tracking reduce my regulatory risk?

Automated insurance tracking reduces risk by eliminating the manual errors that lead to wrongful Collateral Protection Insurance (CPI) placement. Examiners view force-placed insurance as a high-risk area for UDAAP violations. Real-time verification ensures that you only apply CPI when a genuine lapse in coverage exists, providing an unalterable record of your due diligence that protects your portfolio from scrutiny.

What documents are required for a CFPB auto finance examination?

Examiners require a wide range of documents including your compliance management system (CMS) manuals, loan-level data logs, and employee training records. You must also provide samples of marketing materials, vendor contracts, and borrower correspondence. Organizing these files to show the entire “life of the loan” is a critical part of CFPB audit preparation for auto lenders to ensure a smooth review process.

Can software really replace a dedicated compliance officer?

Software cannot replace a dedicated compliance officer, but it acts as a powerful force multiplier for their efforts. A compliance officer sets the strategy and interprets the law, while software like an LMS or DMS automates the execution and documentation. This partnership ensures that your policies are applied consistently across thousands of loans without the risk of human fatigue or unintentional oversight.

How does the CFPB define “junk fees” in the context of auto lending?

The CFPB defines “junk fees” as charges that provide no actual value to the consumer or are not clearly disclosed. In the auto lending sector, this includes excessive late fees, redundant “processing” charges, and add-on products that a borrower is pressured to purchase. Regulators look for fees that appear designed to inflate profit margins rather than cover legitimate operational costs.