For independent and BHPH auto dealers, the Dealer Management System (DMS) is the engine of the business. Yet, understanding its true cost can feel like deciphering a complex code. Between base subscriptions, per-user fees, and a labyrinth of add-on modules, the “starting at” price rarely reflects the final bill. In 2026, the conversation is shifting from a simple monthly fee to the Total Cost of Ownership (TCO)—a calculation that includes not just the software, but the hidden costs of inefficiency it’s meant to solve.

This guide dissects the modern DMS pricing landscape, exposes the hidden fees that inflate your budget, and provides a clear framework for evaluating quotes. More importantly, it reveals how the right platform can move from being a cost center to a profit driver by automating your most expensive manual tasks and mitigating catastrophic risk.

Decoding the 2026 DMS Pricing Landscape: Tiers, Modules, and Subscriptions

The DMS market primarily operates on three pricing models, each with distinct implications for a dealership’s budget and scalability. Understanding these structures is the first step in avoiding unexpected costs and choosing a partner that aligns with your growth.

- Flat-Fee: A single, predictable monthly price for a set package of features, often including unlimited users. This model offers budget stability, making it popular with independent dealers who want to avoid per-seat charges as they grow their team.

- Per-User: The monthly cost is calculated based on the number of active users (e.g., salespeople, finance managers, collectors). While this can seem affordable for very small teams, costs can escalate quickly as your dealership expands.

- Modular (A La Carte): This model starts with a core DMS platform at a low base price, requiring you to purchase additional “modules” for specific functions like CRM, inventory management, or BHPH loan servicing. This provides flexibility but can lead to a surprisingly high total cost once all necessary features are added.

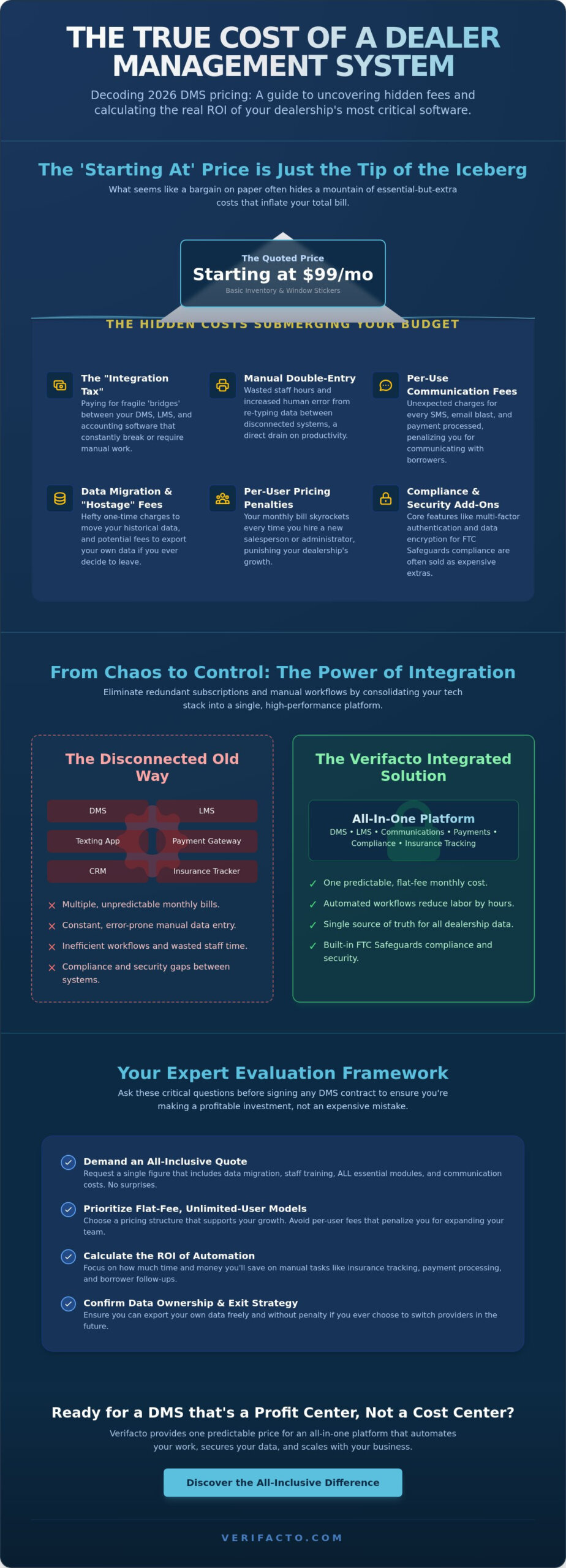

The industry is also standardizing on cloud-based SaaS (Software as a Service) models, which thankfully eliminates the high upfront cost and ongoing maintenance of on-premise servers. However, this shift has made the “Starting at $99” offer a common marketing tactic. This entry-level price often includes only the most basic inventory and sales tools, lacking the critical loan management, collections, and compliance features a modern finance-focused dealership needs to operate profitably. (Management Information System)

Flat-Fee vs. Per-User Pricing: Which Scales Better?

For a growing dealership, the choice between flat-fee and per-user pricing has significant long-term financial consequences. A per-user model penalizes growth; hiring a new salesperson or collector directly increases your monthly software bill. In contrast, a flat-fee structure with unlimited users encourages expansion. You can add staff to drive sales and improve collections without worrying about a corresponding rise in your DMS overhead. This makes flat-fee models inherently more scalable for ambitious independent and BHPH dealers.

Modular Add-ons: The ‘A La Carte’ Trap

Modular pricing presents itself as customizable, but it’s a double-edged sword for growing dealerships. While you only pay for what you need initially, critical functions are often walled off as expensive add-ons. For a BHPH dealer, the core DMS is useless without the BHPH/LMS module. A sales-focused lot can’t function effectively without a CRM module. These “optional” components are, in reality, non-negotiable, and their combined cost can far exceed that of an all-in-one platform.

The Hidden Costs: Beyond the ‘Starting At’ Sticker Price

The monthly subscription is just the tip of the iceberg. The true cost of a DMS is often buried in a host of secondary fees and operational drains that vendors rarely advertise. Identifying these potential expenses during the evaluation process is crucial for creating an accurate budget and avoiding a negative return on investment.

- The Integration Tax: Many dealers are forced to pay for multiple, disconnected systems—a DMS for sales, an LMS for loans, and separate tools for communication or payment processing. The cost to build and maintain “bridges” between these systems, both in fees and manual double-entry labor, can be substantial.

- Implementation and Onboarding: Migrating your existing customer and vehicle data into a new system is rarely free. Some vendors charge thousands for data migration, and the “down time” during staff training represents a real, if hidden, operational cost.

- Payment Processing Fees: If payment processing isn’t truly integrated into the DMS, you’re not only paying a third-party provider but also creating reconciliation headaches. The percentage points and transaction fees can significantly impact the profitability of each loan payment.

- Automated Communication Costs: Features like automated SMS payment reminders or email blasts are powerful, but they often come with per-message or volume-based fees that are not included in the base subscription price.

The True Cost of Data Migration

Switching to a new DMS can feel daunting, and some vendors capitalize on this by charging hefty setup and data migration fees. Before signing any contract, ask pointed questions: How much will it cost to import my entire history from my old system? How long will the process take? And critically, what are the export fees or data ownership policies if I ever decide to leave? Your data is one of your most valuable assets; ensure you can access and move it without being held hostage. (cost-benefit analysis)

Transactional Fees and Third-Party Integrations

Beyond your subscription, a DMS often acts as a gateway to other pay-per-use services. Pulling credit reports, vehicle history reports (Carfax/AutoCheck), and using e-signature services all incur small but frequent charges that add up. Furthermore, connecting to external lenders or other platforms may require paying for API access. An integrated platform like Verifacto, which combines DMS and LMS, eliminates the need for many of these costly third-party bridges and the “double-entry” labor that comes with them.

Calculating ROI: How an Integrated LMS/DMS Pays for Itself

In 2026, the smartest dealers don’t just look at the DMS as an expense; they evaluate it as an investment. The right platform doesn’t just cost money—it generates returns by automating high-cost labor, mitigating financial risk, and increasing collection efficiency. The ROI isn’t just about saving a few hundred dollars on a subscription; it’s about adding thousands to your bottom line.

- Labor Arbitrage: An employee spending hours a week manually calling customers for insurance proof or payment reminders is a significant labor cost. Automation replaces this expensive manual work with an efficient, scalable system.

- Risk Mitigation ROI: For a BHPH dealer, a single uninsured vehicle involved in a total-loss accident can wipe out the profit from a dozen other deals. Integrated tools like automated insurance tracking and Collateral Protection Insurance (CPI) are not features; they are capital preservation strategies.

- Collection Efficiency: Making it easier for borrowers to pay directly impacts your cash flow. Automated reminders, self-service payment portals, and integrated processing reduce delinquency and the labor required to chase late payments.

- The ‘One System’ Advantage: Consolidating your DMS, LMS, payment processor, and communication tools into a single platform eliminates redundant subscription fees and simplifies your entire tech stack.

The Financial Impact of Automated Insurance Tracking

Consider a portfolio of 200 active loans. Manually verifying insurance on each vehicle quarterly can consume dozens of staff hours. An automated system does this in real-time, instantly flagging uninsured policies. This not only saves hundreds in monthly labor costs but also closes the “uninsured gap,” the dangerous period where a vehicle is unprotected. This proactive risk management can be the difference between a profitable portfolio and a series of devastating write-offs.

Boosting Collection Rates with Integrated Payments

Every bit of friction in the payment process increases the likelihood of delinquency. Forcing a borrower to call during business hours or mail a check is inefficient. A DMS with an integrated, self-service payment portal allows customers to pay 24/7 from their phone. When combined with automated SMS reminders that include a direct payment link, dealers consistently see a measurable reduction in 30-day delinquency rates and a significant decrease in time spent on manual collection calls.

A Framework for Evaluating DMS Quotes and Contracts

When you’re comparing DMS options, it’s easy to get lost in feature lists and sales pitches. Use this five-step framework to cut through the noise and make a decision based on total value, not just the sticker price.

- Audit Your Current Stack: List every piece of software you currently pay for (DMS, LMS, CRM, payment processor, SMS tool, etc.). This reveals your true current TCO and identifies redundant fees you can eliminate with an integrated system.

- Request a ‘Total Cost’ Quote: Ask vendors for a 12-month quote that includes all the modules and features you need to run your specific business model. Make sure it itemizes setup fees, data migration, and any per-transaction costs.

- Evaluate Automation Depth: Does the system truly automate the entire workflow for critical tasks like insurance tracking and collections? Can it manage CPI placement without requiring a separate third-party tool? The deeper the automation, the higher the labor savings.

- Check for Contract Lock-ins: Be wary of vendors demanding long-term, multi-year contracts. A company confident in its product and support should be willing to offer a more flexible month-to-month or annual agreement.

- Factor in the ‘Support Premium’: Is live, US-based support included in the price? Is comprehensive onboarding and training provided, or is it an extra charge? Good support is invaluable during the transition period and beyond.

Questions to Ask Sales Reps Before Signing

- Is your payment processing a true, single-platform integration, or are you just referring me to a separate processing company?

- What is the specific cost for automated SMS and email communications, and how is it billed?

- Do you offer a pricing model that eliminates the monthly DMS subscription fee by consolidating it with payment processing?

- Are there any data export or “exit fees” if I decide to migrate to a different platform in the future?

Verifacto: A New Pricing Model for a More Profitable Dealership

The traditional DMS pricing model is fundamentally broken for the modern dealer. You’re asked to pay a hefty monthly subscription fee, only to be charged again for essential services like payment processing and risk management. Verifacto challenges this paradigm with a revolutionary approach designed to align our success with yours.

We provide our fully integrated, cloud-based DMS/LMS platform at no additional monthly subscription cost.

Instead of juggling a DMS bill and a separate merchant services bill, you consolidate. Our revenue comes from the payment processing you’re already paying for—often at a more competitive rate. This allows you to reallocate the money you were spending on a DMS subscription directly back into your business, all while getting a more powerful, efficient, and integrated system.

Built-In vs. Bolted-On: The Verifacto Integration Difference

With Verifacto, critical functions aren’t expensive, “bolted-on” afterthoughts. They are core to the platform. True integration means your sales, loan servicing, payment, and insurance data all live in one secure system. This single source of truth eliminates costly data entry errors, improves compliance, and gives you a real-time, 360-degree view of your entire operation. There is no “integration tax” because there are no integrations to tax.

Protecting Your Collateral and Your Bottom Line

Our platform was built from the ground up to protect the assets of auto finance professionals. Real-time, automated insurance tracking is seamlessly woven into the loan servicing workflow. When an uninsured vehicle is detected, the system facilitates the placement of Collateral Protection Insurance directly within the platform. This proactive risk management transforms your DMS from a simple record-keeping tool into an active defense for your portfolio. Stop paying a subscription for software that just manages your business; partner with a platform designed to protect and grow it.