With the ACH network processing 35.2 billion payments in 2025, electronic transfers have become the primary engine of modern lending. However, as of June 22, 2026, Nacha requires all originators to implement risk-based fraud monitoring, making it essential to refine your approach to ACH processing for auto finance. You’ve likely struggled with high credit card processing fees and manual entry errors that drain your team’s time. It’s difficult to maintain a steady growth trajectory when unpredictable cash flow and late manual payments create constant operational friction.

You deserve a system that works as hard as you do. This guide will help you master the mechanics of ACH to stabilize your cash flow, slash transaction costs, and fully automate your loan portfolio. We’ll explore the latest 2026 regulatory shifts and show you how to integrate recurring payments directly into your LMS. By the end of this reference, you’ll have a clear roadmap to replace manual hurdles with a modern, high-speed payment infrastructure that protects your bottom line and simplifies your daily operations.

Key Takeaways

- Identify the specific SEC codes required for installment loans to ensure every transaction meets current NACHA regulatory standards and avoids processing delays.

- Compare the total cost of ownership between card payments and ACH processing for auto finance to maximize your portfolio’s profit margins.

- Implement a robust return management framework that automates NSF handling and protects your cash flow from unpredictable payment failures.

- Discover how integrated LMS and DMS platforms remove the risks associated with manual data entry and fragmented payment silos.

- Strengthen your compliance foundation by securing valid digital authorizations that protect your business against disputes and chargebacks.

Understanding ACH Processing in the Auto Finance Ecosystem

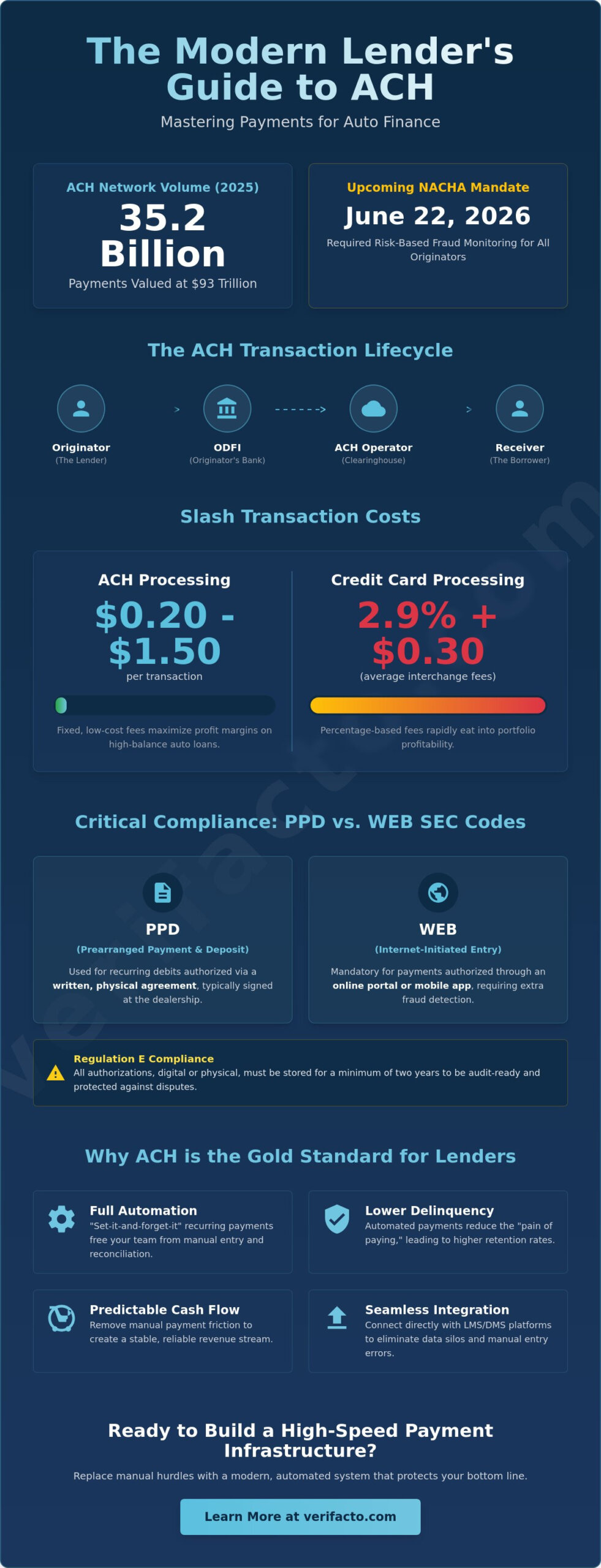

ACH processing for auto finance serves as the operational heart of the modern installment loan industry. It is a batch-based electronic system that moves funds between bank accounts, bypassing the friction of physical checks and the high overhead of card networks. The ACH Network, overseen by Nacha, acts as the central clearinghouse for these transactions in the United States. In 2025 alone, this network processed over 35 billion payments valued at $93 trillion. For auto lenders, this infrastructure provides a reliable way to secure recurring, fixed-interval payments. Transitioning to integrated payment solutions for dealers allows your business to move away from manual reconciliations and embrace a digital-first workflow that prioritizes speed and accuracy.

Key Participants in the ACH Process

Every transaction involves a specific chain of communication. As the lender, you are the Originator. You hold the authority to initiate the payment request based on the borrower’s permission. Following the June 2026 Nacha updates, originators now carry a heightened responsibility to maintain documented fraud monitoring processes. Your bank acts as the Originating Depository Financial Institution (ODFI), which batches your requests and sends them to the ACH operator. On the other side, the Receiving Depository Financial Institution (RDFI) accepts the request and debits the Receiver, which is your borrower. Managing this loop effectively requires clear communication and a firm grasp of borrower authorizations to prevent disputes.

Why ACH is the ‘Gold Standard’ for Auto Lenders

Cost efficiency remains the most compelling reason to prioritize ACH. While credit card transactions often carry high interchange fees that eat into your margins, ACH processing for auto finance typically costs between $0.20 and $1.50 per transaction. For high-balance auto loans, these savings scale rapidly across a large portfolio. Beyond the math, there is a powerful psychological advantage to automation. Set-it-and-forget-it recurring payments reduce the “pain of paying” for the borrower, which lead to higher retention and lower delinquency rates. By removing the manual touch requirement for every monthly installment, you free your team to focus on high-level portfolio management rather than chasing individual checks or processing manual card entries. This shift creates a more stable, predictable cash flow that supports long-term business growth.

The Technical Architecture of Modern Auto Loan ACH

Mastering the technical backbone of ACH processing for auto finance is what separates high-performing lenders from those stuck in manual operational cycles. At its core, the system relies on Standard Entry Class (SEC) codes to define how a transaction is authorized and initiated. These codes aren’t just administrative labels; they dictate the legal and technical requirements you must follow to remain compliant. For auto lenders, the two most critical codes are PPD and WEB. Understanding when and how to deploy each ensures your portfolio remains secure and your dispute risk stays low.

SEC Codes: PPD vs. WEB

PPD, or Prearranged Payment and Deposit, is the traditional standard for auto loan servicing. It’s used when a borrower provides a written, physical authorization for recurring debits, typically during the car-buying process at the dealership. In contrast, WEB (Internet-initiated Entry) is mandatory if the borrower authorizes a payment through an online portal or a mobile application. Because WEB transactions carry a higher inherent risk, Nacha mandates specific fraud detection and account validation steps for these entries. Regardless of the code used, your authorization storage must align with Regulation E, which provides the legal framework for electronic fund transfers and protects consumers against unauthorized debits. Maintaining digital or physical copies of these authorizations for at least two years is a non-negotiable requirement for audit readiness.

The Settlement Timeline and Cash Flow Impact

The lifecycle of an ACH transaction moves through a structured sequence of file transmission and settlement. It begins when your system generates a batch file and transmits it to your bank. The ACH Operator then clears these transactions and routes them to the borrower’s financial institution. While standard processing typically takes one to two business days, Same-Day ACH has become a strategic asset for modern lenders. It allows you to process late payments or recovery installments with much higher velocity. If a borrower makes a payment by the morning cutoff, the funds can settle by the end of the same business day, providing an immediate boost to your liquidity.

Managing these batch files manually is a recipe for error and delay. Modern dealer management systems eliminate this friction by automating the generation of NACHA-formatted files directly from your loan records. This integration ensures that every transaction uses the correct SEC code and settlement window without requiring a single keystroke from your staff. If you’re looking to tighten your operational loop, it’s time to explore how Verifacto’s built-in payment processing can turn your technical architecture into a competitive advantage.

ACH vs. Alternatives: Optimizing Cost and Collection Speed

Choosing the right payment rail is a strategic decision that directly dictates your portfolio’s profitability. While many lenders default to credit or debit cards for their perceived speed, the long-term financial drain is often overlooked. High interchange fees and frequent chargebacks can quietly erode the margins of even the most robust loan books. By shifting to ACH processing for auto finance, you trade variable, percentage-based costs for a predictable, flat-rate model that scales with your growth. This transition doesn’t just save money; it provides a deeper level of data that card networks simply can’t match.

The True Cost of Payment Processing

Card networks thrive on interchange fees that often range from 1.5% to 3.5% per transaction. On a typical $500 car payment, you could lose up to $17.50 every single month to the processor. In contrast, industry data for 2026 shows that specialized ACH providers offer rates between $0.20 and $0.50 per transaction. For a lender managing a 500-unit portfolio, this cost difference is staggering. Moving those 500 monthly payments from card to ACH can save your business thousands of dollars in annual overhead. Beyond the direct fees, you must account for the labor costs of manual entry and error correction. Automated ACH batches eliminate the “human touch” requirement, allowing your team to focus on high-value tasks rather than reconciling manual receipts.

Reliability and Dispute Management

Dispute risks represent a major vulnerability in auto lending. Card networks often favor the consumer in chargeback scenarios, leaving lenders to fight uphill battles against “friendly fraud.” ACH operates under a different set of rules. While borrowers can still contest a debit, the NACHA framework requires more specific grounds for a dispute, making it harder to “game” the system than a simple credit card chargeback. Additionally, ACH return codes provide a predictive window into borrower behavior. A card decline is a binary “no,” but an ACH return tells a story. Codes like R01 (Insufficient Funds) or R03 (No Account/Unable to Locate Account) serve as early warning signs of financial distress.

Leveraging these return codes is a key component of improving collection efficiency for auto loans. Instead of waiting for a total default, you can use automated payment reminders for car loans to trigger immediate outreach the moment a return is flagged. This proactive approach turns your payment system into a risk mitigation tool. When you integrate ACH processing for auto finance into your core workflow, you gain the stability of a “set-it-and-forget-it” system that protects your cash flow while providing the transparency needed to manage a high-volume portfolio with confidence. For Buy Here Pay Here dealers specifically, pairing this approach with a disciplined BHPH cash flow management strategy is essential to keeping liquidity healthy when subprime delinquency rates are elevated.

Best Practices for Compliant ACH Implementation

Compliance isn’t just a hurdle; it’s the framework that protects your portfolio from legal volatility. In 2026, the regulatory environment for ACH processing for auto finance has sharpened its focus on fraud prevention and consumer clarity. Maintaining auto finance compliance management requires more than just a signed document. It demands a systematic approach to record-keeping and borrower communication that stands up to audit scrutiny. If you change a payment amount, for instance, you must provide the borrower with written notice at least 10 days before the scheduled transfer. Failing to automate these notices is a high-risk gamble that can lead to costly disputes and potential regulatory fines.

The 4 Pillars of ACH Authorization

A compliant program starts with a rock-solid authorization. First, you must present terms in a clear and conspicuous manner so the borrower understands exactly what they’re signing. Second, you must provide a straightforward revocation procedure. Borrowers need a clear, documented path to cancel their authorization as mandated by federal law. Third, identity verification is now a critical pillar under the June 2026 Nacha rules. You must implement risk-based fraud monitoring to ensure the account belongs to the person authorizing the debit. Finally, you must store these records securely for at least two years. The burden of proof always rests on the lender during a dispute, so digitized, easily accessible records are essential.

Managing Returns and Re-presentment

Handling returns efficiently prevents your cash flow from stalling. When a transaction fails, you’ll receive a return code that tells you exactly why. R01 indicates insufficient funds (NSF), while R02 means the account is closed, and R04 signals an invalid account number. Each code requires a different operational response. For NSF items, Nacha allows you to re-present the transaction up to two additional times within 180 days of the original authorization. However, you can’t simply hammer an account with repeated attempts. Sophisticated lenders use their LMS to automate a switch to alternative payment methods or trigger immediate borrower outreach after the second return. This proactive stance keeps your delinquency rates low and reduces the $2 to $5 fees typically associated with each return occurrence.

Stay ahead of regulatory shifts by using Verifacto LMS with built-in payment processing to automate your compliance and return management today.

Scaling Your Portfolio with Integrated ACH Solutions

Operating with siloed payment systems is one of the most significant risks to a growing loan book. When your payment processor doesn’t “talk” to your ledger, you’re forced to rely on manual exports and CSV uploads. This fragmented approach is a breeding ground for errors. A single missed entry or a misaligned decimal point can lead to incorrect late fees, frustrated borrowers, and regulatory headaches. To truly scale, you must move beyond basic ACH processing for auto finance and adopt a system where the transaction and the loan record exist in the same ecosystem. True mastery over your portfolio requires a unified view that links every dollar collected to the status of the collateral it secures.

The Power of True Integration

Integrated LMS and DMS platforms transform your back office from a reactive cost center into a proactive growth engine. When a payment settles via ACH, an integrated system like Verifacto’s LMS automatically updates the borrower’s ledger in real time. This eliminates the need for manual reconciliation and ensures your data is always audit-ready. Automation also extends to borrower relations. Instead of your team spending hours on the phone, the system can trigger Automated Borrower Communication the moment a payment is initiated or returned. This immediate feedback loop keeps borrowers informed and reduces the “manual touch” requirement that often bottlenecks high-volume portfolios. By removing human error from high-stakes financial environments, you protect both your reputation and your bottom line.

Future-Proofing with 2026 Technology

As we move through 2026, the industry is shifting toward predictive delinquency management. Modern lenders no longer just react to missed payments; they use data to anticipate them. By leveraging AI to analyze borrower history, you can identify the optimal ACH pull dates that align with a borrower’s actual cash flow patterns. This precision significantly reduces NSF returns and stabilizes your monthly revenue. Furthermore, the most sophisticated operations link their ACH processing for auto finance directly to Insurance Tracking and CPI Solutions. If a payment fails and the borrower’s insurance also lapses, the system flags the account for immediate risk mitigation. This holistic view of the payment-to-collateral lifecycle allows you to manage risk with surgical precision rather than broad, expensive strokes.

The days of managing payments in a vacuum are over. To maintain a competitive edge, you need a platform that treats payment processing as a core component of risk management. Modernize your payment processing with Verifacto’s integrated platform to secure your cash flow and automate your path to portfolio growth.

Take Command of Your Portfolio’s Financial Future

The shift toward digital-first lending isn’t just a trend; it’s a fundamental change in how high-performing portfolios operate. By mastering ACH processing for auto finance, you position your business to absorb the 2026 regulatory changes while simultaneously slashing the high interchange fees associated with card networks. You’ve seen how technical architecture and integrated systems turn payment data into a predictive tool for delinquency management. Now is the time to bridge the gap between your payment processing and your collateral security.

Efficiency comes from a unified ecosystem where your ledger, your borrower communications, and your insurance tracking work in perfect synchronization. This level of automation doesn’t just reduce human error; it creates the stability you need to scale with confidence. You have the tools and the technical knowledge to transform your cash flow into a strategic asset that supports long-term growth.

Streamline Your Auto Finance Operations with Verifacto’s Integrated Payments and leverage built-in processing, real-time insurance tracking, and automated borrower communication tools. Your path to a more secure and profitable portfolio starts today.

Frequently Asked Questions

What is the difference between Same-Day ACH and standard ACH for auto loans?

Same-Day ACH clears on the same business day it’s initiated, provided it meets bank cutoff times, while standard ACH typically settles in one to two business days. This speed makes Same-Day ACH ideal for urgent late-payment recovery or same-day loan fundings. Standard processing remains the cost-effective choice for scheduled monthly installments. Both options use the same NACHA framework but differ in settlement velocity and associated bank fees.

How many times can I re-present an ACH payment if it returns for NSF?

You can re-present an ACH payment up to two additional times after the initial return for insufficient funds (R01) or uncollected funds (R09). These attempts must occur within 180 days of the original authorization date. It’s best practice to coordinate these attempts with the borrower’s known pay schedule to increase the likelihood of success. Repeated failures after the second re-presentment should trigger an immediate shift to alternative collection strategies.

Is a written signature required for ACH authorization, or can I do it online?

Both written signatures and digital authorizations are legally valid, though they require different SEC codes for compliance. Use the PPD code for physical, wet-ink signatures captured at the dealership. For online portals or mobile apps, you must use the WEB code. Since 2021, Nacha requires account validation for all first-time WEB transactions to prevent fraud in ACH processing for auto finance.

What are the most common ACH return codes auto lenders should know?

Auto lenders should prioritize monitoring R01, R02, R03, and R04 return codes. R01 signifies insufficient funds, while R02 indicates a closed account. R03 and R04 both point to account data errors, such as an invalid account number or an inability to locate the bank record. Recognizing these codes early allows your team to distinguish between a borrower’s temporary financial hurdle and a potential fraud attempt.

How does ACH processing integrate with my existing DMS or LMS?

Integrated ACH processing for auto finance eliminates manual data entry by syncing your payment gateway directly with your loan records. When a borrower signs their contract, the LMS captures the authorization and schedules the recurring batch files automatically. This connection ensures that every payment settles directly against the borrower’s ledger without requiring manual reconciliation. It turns your DMS into a real-time financial dashboard.

What are the NACHA compliance requirements for storing borrower bank data?

Nacha mandates that all sensitive bank data, including routing and account numbers, must be encrypted both at rest and during transmission. You must also implement strict access controls to ensure only authorized personnel can view or handle this information. Following the 2026 fraud monitoring updates, you’re required to have documented processes for detecting and reporting suspicious activity within your stored data environment.

Can I pass ACH processing fees on to the borrower in my state?

The ability to pass ACH fees to a borrower depends entirely on state-specific usury laws and the language in your retail installment contracts. Many states prohibit charging a convenience fee for the only available payment method. You should consult with local legal counsel to ensure your fee structure doesn’t violate consumer protection statutes or the terms of your original lending agreement.

How do I handle an ACH dispute from a borrower?

To resolve a dispute, you must provide a valid copy of the borrower’s authorization to your bank within the timeframe requested by the RDFI. If you can’t produce a compliant authorization, the bank will likely reverse the transaction. Maintaining digitized, easily searchable records in your LMS is the best way to handle these claims quickly and protect your portfolio from unauthorized transaction disputes.