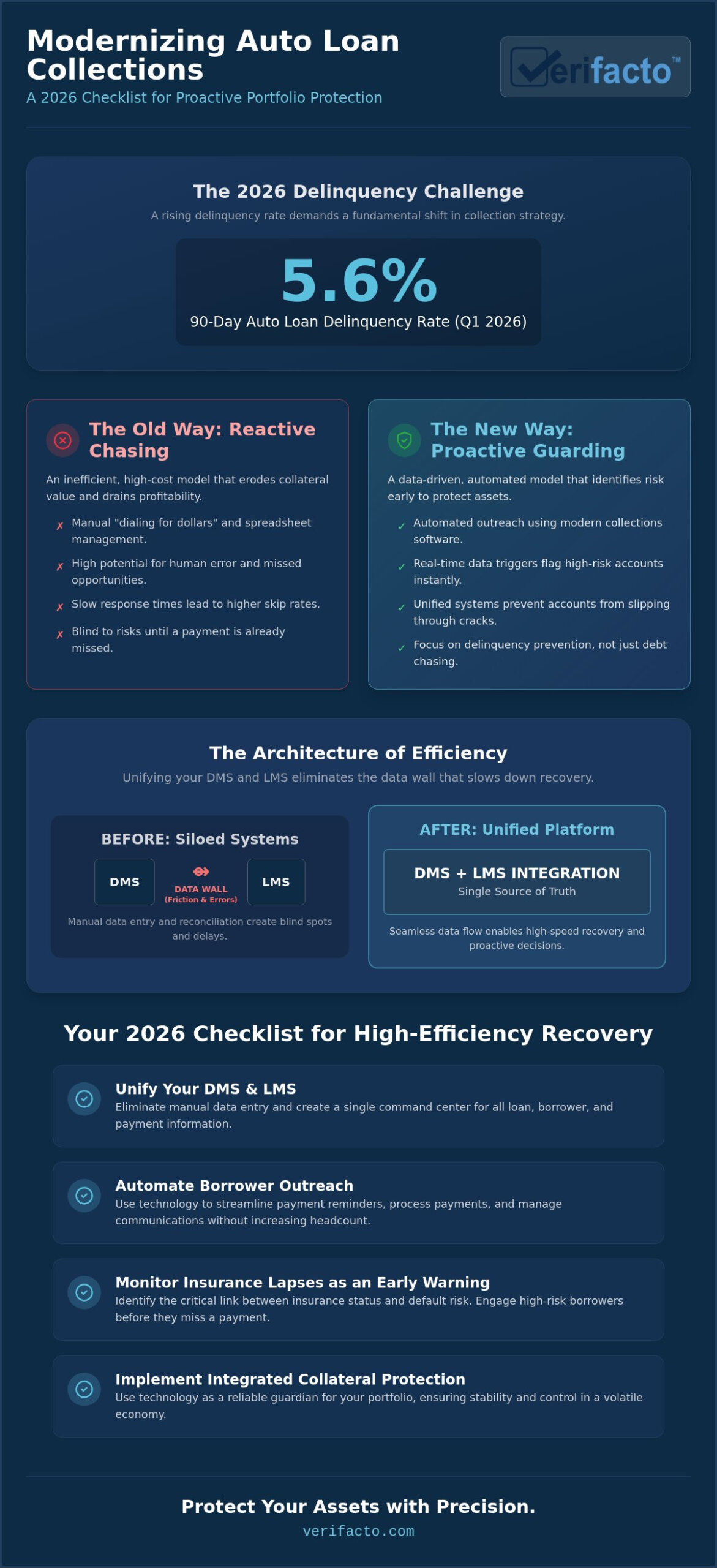

With the 90-day auto loan delinquency rate hitting 5.6% in the first quarter of 2026, lenders are facing a level of portfolio risk that manual outreach simply can’t handle. It’s a high-stakes environment where traditional methods are falling short. You already know that chasing payments through spreadsheets and manual phone calls is a losing battle. It’s slow, prone to human error, and often leaves you blind to the status of your collateral until it’s too late. To stay ahead, you need modern auto loan collections software that acts as a guardian for your portfolio, identifying risks before they turn into losses.

We agree that the old way of “dialing for dollars” is inefficient in a volatile economy where insurance lapses often precede a default. This strategic checklist promises to show you how to modernize your recovery workflows, leverage real-time insurance data, and reduce delinquencies using automated lending technology. We’ll walk through the specific tools you need to gain real-time visibility into portfolio risk and streamline your payment processing for a more secure, stable bottom line. It’s time to move beyond reactive recovery and start protecting your assets with precision.

Key Takeaways

- Understand why the 5.6% delinquency rate in 2026 requires a shift from reactive chasing to proactive, data-driven recovery strategies.

- Discover how modern auto loan collections software eliminates operational friction by unifying your DMS and LMS into a single, high-speed command center.

- Identify the critical link between insurance lapses and defaults to engage high-risk borrowers before they miss a single payment.

- Implement a 2026-ready checklist that automates borrower outreach and streamlines payment processing without increasing your headcount.

- Learn how integrated collateral protection acts as a reliable guardian for your portfolio, ensuring stability and control in a volatile economy.

Understanding Collection Efficiency in the 2026 Auto Finance Market

Collection efficiency is the definitive metric of your recovery department’s health. It’s measured as the ratio of recovered debt to the total cost of your recovery operations. If you’re spending $500 in labor and overhead to recover $600, your efficiency is dangerously low. In the first quarter of 2026, the 90-day auto loan delinquency rate reached 5.60%, a figure that has forced lenders to rethink their entire approach. You can’t rely on the old ways of “debt chasing” anymore. The industry is moving toward a “portfolio guarding” strategy where the goal is to prevent the delinquency before it starts.

Manual processes are the primary cause of the recovery gap. When your staff relies on spreadsheets or outdated notes, they lose the critical window of opportunity to engage a borrower. This lag time drains dealership profitability and leaves your collateral exposed. To maintain a competitive edge, you must transition to a proactive model that uses data triggers to flag high-risk accounts instantly. High-performing lenders now use auto loan collections software to automate these early warnings, ensuring no account slips through the cracks.

The High Cost of Inefficient Collections

The true cost of a missed payment goes far beyond the face value of the installment. Hidden costs like labor hours, opportunity costs, and rapid vehicle depreciation create a compounding financial drain. Every hour your team spends on manual outreach is an hour they aren’t spending on high-value portfolio management. The debt collection process is time-sensitive; the longer a vehicle remains in the hands of a non-paying borrower, the higher the skip rate becomes. Inefficient collections do not just lose money; they erode the collateral value that secures the loan. When you act slowly, you’re essentially watching your asset’s value evaporate in real-time.

Why Digital Transformation is the 2026 Standard

Legacy desktop software is no longer viable in a fast-paced lending market. These systems are often siloed, making it impossible to see the full picture of a borrower’s behavior. In contrast, modern cloud based dealer management systems provide a centralized brain for your entire operation. Cloud accessibility allows your team to stay agile, whether they’re in the office or managing a national portfolio from the field. Real-time data is the fuel for split-second collection decisions. By adopting auto loan management software, you eliminate the friction between sales and servicing. This integration ensures that your auto loan collections software has the most accurate, up-to-date information to protect your assets and stabilize your cash flow.

The Architecture of Efficiency: Integrating DMS and LMS

Efficiency in a lending environment isn’t just about how hard your collectors work; it’s about how well your systems communicate. Most lenders struggle with a “data wall” between their Dealer Management System (DMS) and their Loan Management System (LMS). This friction slows down recovery and creates blind spots that lead to missed opportunities. When these systems are siloed, your team is forced to jump between tabs, manually reconcile ledgers, and guess which borrower needs a call first. By integrating these functions, auto loan management software serves as the central brain for your recovery operations, ensuring that data flows without interruption.

As auto loan delinquency rates remain a primary concern for portfolio health, the speed of your data transfer becomes a critical competitive advantage. A single source of truth for borrower contact info and payment history eliminates the “recovery gap” mentioned previously. When your systems are unified, you remove the need for manual data entry, which is the primary bottleneck in operational speed. Every minute spent re-keying a borrower’s phone number is a minute lost that could have been spent securing a commitment to pay. Modern auto loan collections software removes these hurdles, allowing your team to focus on high-impact communication rather than administrative busywork.

Verifacto LMS & DMS: A Unified Workflow

Verifacto DMS and Verifacto LMS work in tandem to create a seamless interface for your staff. This integration means that when a deal is closed in the DMS, the servicing data is instantly available in the LMS without any manual intervention. One of the most significant advantages is the built-in payment processing. When a borrower makes a payment, the ledger updates in real-time across the entire platform. This level of accuracy builds collector confidence and prevents “collections amnesia.” You don’t want your team calling a borrower to demand a payment that was already made five minutes ago. Real-time updates protect your professional reputation and ensure that your outreach is always based on the most current facts.

Automated Workflows vs. Manual Errors

Manual errors are the silent killers of dealership profitability. In a high-volume environment, it’s easy for small mistakes to snowball into total collateral loss. The three most common manual errors include using outdated phone numbers, missing the end of a grace period, and losing track of updated insurance documents. Automated triggers within the LMS solve this by ensuring no delinquent account is ever overlooked. These triggers can send automated reminders via text or email the moment a payment is missed or an insurance policy lapses. This level of automation allows a smaller team to manage a larger, high-performance portfolio with total precision. If you’re ready to streamline your operations, moving toward an integrated, automated system is the most effective path forward.

Insurance Tracking: The Early Warning System for Collections

Predicting a default before it happens is the “holy grail” of auto finance. While most lenders wait for a missed payment to trigger a collection call, high-efficiency portfolios look for earlier indicators. Data shows that a borrower who stops paying for their auto insurance is three times more likely to stop paying for the vehicle itself. This correlation makes insurance status the ultimate early warning system. By integrating real-time insurance tracking into your auto loan collections software, you gain the ability to see a crisis forming weeks before the ledger shows a delinquency.

Traditional “file checking” is a reactive, manual process that leaves your collateral exposed. Waiting for a paper notice from an carrier is too slow for the 2026 market. Modern lenders use CIMS™ (Continuous Insurance Monitoring System) to receive instant digital updates when a policy is canceled or non-renewed. This technology allows you to act as a guardian for your portfolio, reaching out to the borrower to resolve the coverage gap before the situation escalates into a total loss. Maintaining a clear line of communication during these events is critical, and all outreach should remain compliant with the Fair Debt Collection Practices Act (FDCPA) to protect your business from legal risk.

Predictive Delinquency: The Insurance Indicator

The psychology of a struggling borrower is predictable. When a household budget tightens, the bills that don’t result in immediate service loss are often the first to go. Since a lapse in insurance doesn’t immediately stop the car from starting, it’s frequently cut before the car payment. Tracking these lapses allows your collectors to reach out with a helpful, partner-like tone. Instead of a confrontational debt collection call, the conversation starts with a proactive check on the vehicle’s protection. This data allows you to prioritize your daily collection queue, focusing your team’s energy on the accounts with the highest probability of imminent default.

Mitigating Risk with Automated CPI

Even with the best outreach, coverage gaps will occur. This is where collateral protection insurance (CPI) acts as a critical safety net. Moving from manual lender-placed insurance to automated CPI solutions removes the administrative burden from your staff. Verifacto’s auto loan collections software uses insurance tracking triggers to send automated notifications to borrowers regarding their coverage status. If the borrower doesn’t provide proof of insurance within the required timeframe, the system can automatically initiate CPI placement. This no-nonsense approach ensures your assets are protected 24/7 without requiring a single manual entry from your team, allowing you to maintain stability even in a volatile economy.

The 2026 Checklist for Improving Collection Efficiency

Efficiency in a high-stakes lending environment is never an accident; it’s the result of a deliberate, structured framework. While selecting the right auto loan collections software is a critical first step, your operational success depends on how you deploy that technology. In a market where delinquencies are projected to remain high, you need a no-nonsense roadmap to protect your assets. Follow this five-step checklist to transform your recovery department into a high-performance engine.

- Step 1: Audit your data integrity. Verify borrower phone numbers and email addresses at the point of origination. If your data is wrong from day one, your automation will fail.

- Step 2: Implement multi-channel automated borrower communication. Reach borrowers where they actually spend their time: on their phones.

- Step 3: Deploy self-service payment portals. Reduce inbound call volume and remove friction by allowing borrowers to resolve balances 24/7 without speaking to an agent.

- Step 4: Set up automated payment reminders. Send a gentle notification three days before the due date to catch “accidental” delinquencies before they happen.

- Step 5: Integrate real-time insurance monitoring. Use data triggers to flag high-risk accounts the moment coverage drops, giving you a head start on recovery.

Mastering Multi-Channel Outreach

The 2026 market is mobile-first. Relying solely on traditional voice calls is a recipe for low contact rates and high labor costs. SMS and email notifications often see significantly higher engagement rates because they respect the borrower’s time while providing a direct path to payment. However, compliance remains paramount. Ensure your auto loan collections software includes built-in guardrails for TCPA and FDCPA regulations. Using automated notifications for grace period reminders is a powerful way to catch well-intentioned borrowers who simply forgot their due date, keeping them in good standing without manual intervention.

Frictionless Payment Processing

Every additional click in the payment process is an opportunity for a borrower to change their mind. This is why integrated payment solutions for dealers are critical for modern recovery. By offering ACH and recurring payment options, you stabilize your monthly cash flow and reduce the burden on your staff. A “one-click” payment link embedded in an SMS can dramatically increase same-day recovery rates. It moves the borrower from “I’ll do it later” to “done” in seconds. If you are ready to modernize your recovery workflow, focusing on these frictionless touchpoints will yield the fastest results for your portfolio.

Securing Your Portfolio with Verifacto Technology

Verifacto’s integrated platform is the definitive answer to the 2026 efficiency crisis. By combining the DMS, LMS, and real-time insurance tracking into a single ecosystem, we eliminate the blind spots that lead to defaults. This is more than just auto loan collections software; it’s a comprehensive system designed to protect your capital. The platform acts as a reliable guardian, monitoring your collateral 24/7 without the need for additional headcount. You gain mastery over complex operational hurdles because this modern auto loan collections software identifies risks, like insurance lapses, before they become financial losses. The no-nonsense requirements of daily operations demand a system that doesn’t just record history, but predicts the future. Verifacto’s CIMS™ technology provides that foresight, turning insurance data into actionable intelligence.

The competitive advantage lies in having CPI solutions and insurance tracking built directly into the core LMS. Most lenders are forced to use third-party plugins that don’t talk to their ledger, creating data lag and reconciliation nightmares. Verifacto removes this friction entirely. When you modernize your tech stack today, you aren’t just improving this month’s recovery; you’re safeguarding tomorrow’s margins against economic volatility. This proactive stance ensures your business remains stable even when national delinquency rates fluctuate. It’s about maintaining stability and control in a high-stakes environment where every percentage point of recovery counts.

Beyond Recovery: Building Long-Term Portfolio Value

Efficient collections do more than just recover cash; they build long-term portfolio value. If you plan to seek future funding or sell your portfolio, your recovery rates and data integrity are the first things investors examine. By reducing charge-offs through early intervention strategies powered by CIMS™, you demonstrate a level of control that manual shops can’t match. This shift moves your team from the role of a “collector” to that of a “portfolio manager.” You’re no longer just chasing debt; you’re optimizing an asset class. Better data leads to better decisions, which ultimately leads to a more attractive and bankable portfolio for your business.

Getting Started with Verifacto

Implementation is a no-nonsense process tailored for independent and BHPH dealers. We understand that you need to stay operational during the transition, so our team ensures a smooth migration of your existing data. Verifacto also supports auto finance compliance management, giving you built-in guardrails to navigate changing regulations safely. This security allows you to scale your operations without scaling your anxiety. Don’t let manual errors or rising delinquency rates erode your hard-earned profits. Take the first step toward a more secure future and schedule a demo to see Verifacto in action.

Future-Proofing Your Portfolio for 2026 and Beyond

The 2026 lending environment doesn’t allow for operational delays or manual blind spots. You’ve seen how integrating your DMS and LMS creates a single source of truth that powers faster recovery. By using real-time insurance tracking as an early warning system, you can engage borrowers before a payment is even missed. This proactive approach is the only way to maintain stability as delinquency rates fluctuate across the country. It’s about working smarter, not harder, to keep your cash flow consistent.

Implementing high-performance auto loan collections software is no longer a luxury; it’s a requirement for survival. Verifacto provides the tools you need to act as a guardian for your assets. With real-time CIMS™ Insurance Tracking, automated CPI solutions, and built-in payment processing for dealers, you can modernize your recovery workflows without adding headcount. Streamline your collections with Verifacto’s integrated LMS & DMS platform today to ensure your portfolio remains protected and profitable. You’ve got the checklist; now it’s time to take decisive action and secure your margins. We’re here to help you navigate these challenges with confidence.

Frequently Asked Questions

What is the most effective way to improve auto loan collection efficiency?

The most effective way to improve efficiency is to unify your DMS and LMS into a single data stream. This integration removes the manual bottlenecks that slow down your recovery team. By using integrated auto loan collections software, you can automate routine tasks and focus your staff on high-priority accounts. This ensures that no delinquent borrower is overlooked due to administrative friction or data silos.

How does automated borrower communication help with loan recovery?

Automated borrower communication helps by reaching borrowers through their preferred channels, such as SMS and email, instantly. It eliminates the need for collectors to manually dial every number, which is often slow and unproductive. Automated systems can send reminders before the due date or immediately after a missed payment. This rapid response keeps your portfolio healthy and significantly reduces the 30-day delinquency rate.

Can insurance tracking really predict a car loan default?

Insurance tracking is a highly accurate predictor of default because borrowers often cut insurance premiums before they stop making car payments. When a policy lapses, it serves as a red flag that the borrower is facing financial distress. Using real-time monitoring allows you to intervene early. This proactive strategy protects your collateral and gives you a chance to resolve issues before they escalate into a total loss.

Is text messaging for collections compliant with 2026 regulations?

Text messaging remains compliant in 2026 as long as you follow specific TCPA and FDCPA guidelines. You must obtain proper consent and provide clear opt-out instructions in every message. Modern auto loan collections software includes built-in compliance guardrails to help you manage these requirements. Staying updated on state-level enforcement is also critical to ensure your digital outreach remains within legal boundaries.

What is the difference between a DMS and an LMS in collections?

A Dealer Management System (DMS) focuses on front-end sales and inventory, while a Loan Management System (LMS) handles back-end servicing and collections. In a collections context, the LMS is the primary tool for tracking payments and managing delinquencies. Integrating the two ensures that borrower information from the point of sale is perfectly synchronized with the servicing ledger, preventing the data errors that often stall recovery efforts.

How does integrated payment processing reduce late payments?

Integrated payment processing reduces late payments by offering borrowers frictionless ways to pay, such as one-click links in text messages. When the payment system is built into the LMS, the ledger updates instantly. This allows you to set up recurring ACH payments that stabilize your monthly cash flow. Removing the need for a borrower to log into a separate portal significantly increases your same-day recovery rates.

Why should I use CPI (Collateral Protection Insurance) for my portfolio?

You should use Collateral Protection Insurance to safeguard your assets when a borrower fails to maintain their own coverage. CPI acts as a safety net that protects the lender’s interest in the vehicle. Automated CPI solutions trigger placement the moment a lapse is confirmed via insurance tracking. This ensures your portfolio remains protected 24/7 without requiring your staff to manually monitor thousands of individual policies.

What are the best practices for auto finance collections in a high-interest economy?

Best practices in a high-interest economy focus on early intervention and data-driven prioritization. You must identify high-risk borrowers before they reach the 60-day delinquency mark. Use real-time data triggers to monitor both payment behavior and insurance status. By acting as a proactive guardian rather than a reactive debt chaser, you can maintain healthy margins even when borrowing costs remain elevated for your customers.