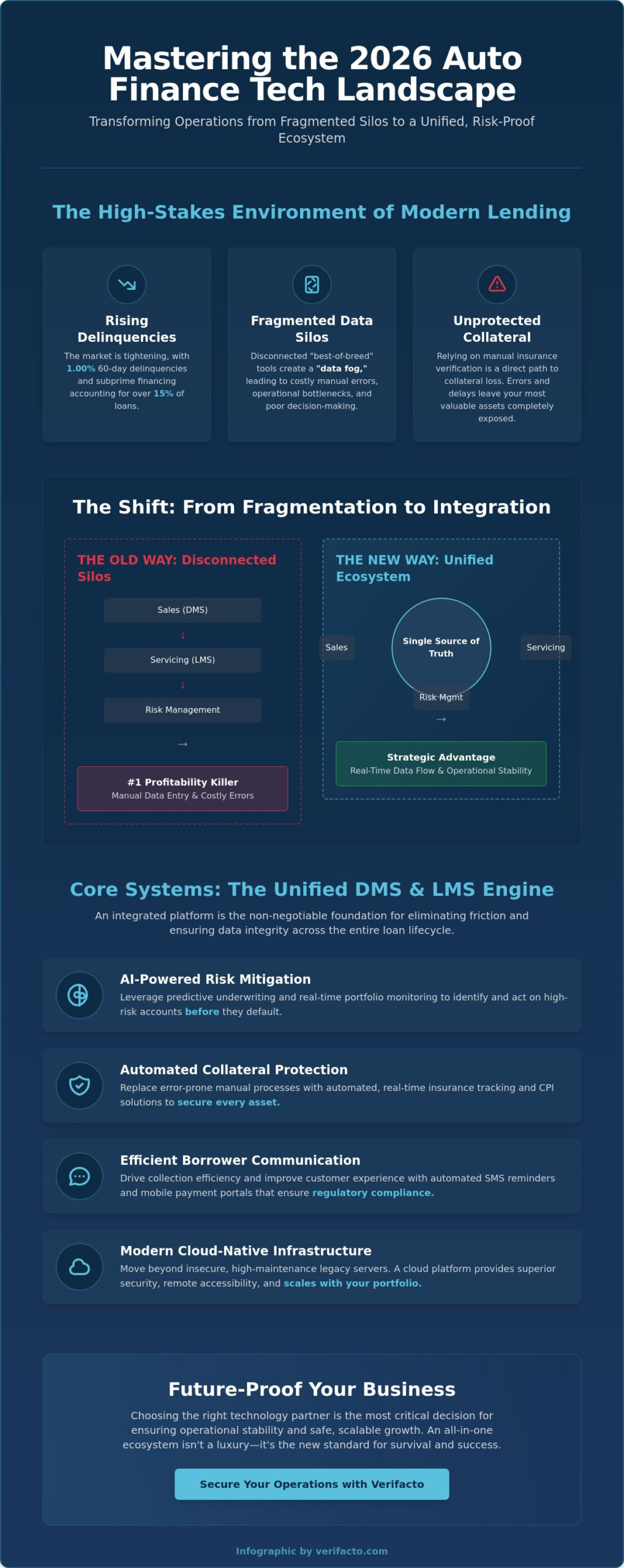

In an era where 60-day delinquencies have climbed to 1.00% and subprime financing accounts for over 15% of the market, simply “digitizing” your workflow isn’t enough to protect your margins. You’ve likely felt the frustration of fragmented data across multiple platforms or the sting of collateral loss because of manual insurance verification errors. It’s a high-stakes environment where traditional methods leave too much to chance. To stay competitive, you need a tech stack that does more than just store data; it must actively mitigate risk.

This article helps you master the 2026 landscape by showing you how the right technology for auto finance companies can transform your operations. We’ll explore how integrated DMS and LMS ecosystems create a single source of truth that eliminates manual bottlenecks and data silos. You’ll discover how to leverage automated insurance tracking and CPI solutions to secure your assets while using automated borrower communication to improve collection efficiency. We are moving beyond broad strategic goals to the specific operational advantages that keep your portfolio stable and your business growing.

Key Takeaways

- Discover why the industry is moving away from fragmented software silos toward unified ecosystems that manage the entire loan lifecycle from a single source of truth.

- Learn how the latest technology for auto finance companies integrates DMS and LMS platforms to ensure seamless handoffs and eliminate operational bottlenecks.

- Identify high-impact methods for protecting collateral through automated insurance tracking and CPI solutions that replace prone-to-error manual verification.

- Explore how shifting to automated borrower communication via SMS and mobile portals drives collection efficiency while maintaining strict regulatory compliance.

- Establish the essential criteria for selecting a tech partner that prioritizes operational stability and provides the scalability needed to grow your portfolio safely.

The 2026 Auto Finance Tech Landscape: From Fragmentation to Integration

The 2026 landscape is defined by speed and absolute data transparency. Auto finance companies are rapidly moving away from the era of disconnected software tools that require constant manual oversight. The modern standard is a cloud-native, mobile-first environment where data flows without friction between departments. This shift toward integrated Financial technology (FinTech) allows lenders to respond to market changes and borrower needs instantly, rather than waiting for end-of-month reports.

Relying on “best-of-breed” silos, where your sales, servicing, and risk management tools don’t talk to each other, is a recipe for operational failure. The winning strategy is the “all-in-one” ecosystem. These platforms handle the entire loan lifecycle from the first credit pull to the final payment. When your systems are integrated, you eliminate the #1 profitability killer: manual data entry. Re-keying information between platforms leads to costly errors, delays funding, and increases the risk of collateral loss. It creates a “data fog” that makes it impossible to see the true health of your business in real time.

AI has moved from a buzzword to a functional necessity. In 2026, predictive underwriting models analyze real-time behavioral data and alternative credit signals to spot potential defaults before they happen. This technology for auto finance companies monitors portfolio health continuously, flagging high-risk accounts based on shifting payment patterns or insurance status changes. It allows you to take proactive steps rather than reacting to a crisis after the borrower has already disappeared. A comprehensive approach to auto loan default management combines these predictive tools with automated workflows to minimize delinquencies before they escalate into charge-offs.

The Death of the Legacy Server-Based DMS

On-premise servers are now a significant security and compliance liability. They are expensive to maintain and difficult to secure against modern cyber threats. Cloud-based systems provide the accessibility your remote teams need while ensuring compliance with evolving data privacy laws like the CARS Act. Transitioning to a subscription model replaces heavy upfront capital expenditure with predictable operational costs, allowing you to scale your portfolio without the hardware headache. For a comprehensive walkthrough of this transition, our cloud based loan management system implementation guide covers every step auto lenders need to modernize their operations in 2026.

Why Real-Time Data is the New Gold Standard

Batch processing is dead. The new gold standard is real-time API connections for credit scoring and vehicle valuations. Instant data access means you can fund contracts faster and reduce the time vehicles sit on “held” status. Understanding What is DMS? in the 2026 context reveals that it’s no longer just a digital filing cabinet. It’s a strategic asset that powers your entire decision-making engine, ensuring that every dealer partner and loan officer is working from the same set of facts.

Core Systems: Evaluating Integrated DMS and LMS Platforms

In 2026, the distinction between Loan Origination Systems (LOS) and Loan Management Systems (LMS) is the difference between starting a race and finishing it. While an LOS focuses on the front-end credit decision, the LMS is the engine that powers the next 48 to 72 months of the loan’s life. For independent lenders, using separate, disconnected platforms creates a dangerous blind spot during the handoff. Adopting integrated technology for auto finance companies ensures that every detail captured during the sale, from borrower income to insurance data, flows directly into the servicing ledger without manual intervention.

A unified DMS/LMS ecosystem provides a significant strategic advantage. It eliminates the friction that typically occurs when a deal moves from the sales floor to the back office. When your DMS and LMS share the same database, you gain a single source of truth for every account. This integration is vital for maintaining consumer protection in auto lending, as it prevents the data discrepancies that often trigger regulatory audits. Key features like built-in payment processing and automated document management further streamline the process, ensuring that every payment is recorded instantly and every contract is stored securely.

The All-In-One vs. Best-of-Breed Debate

Independent lenders often struggle with technical debt, which is the cumulative cost of maintaining multiple software subscriptions that don’t talk to each other. While large captive lenders might choose different vendors for every niche function, smaller operations find that a single-vendor solution offers a much higher ROI. A unified approach simplifies staff training and provides a more reliable support structure. When you choose an integrated platform like Verifacto LMS, you reduce the risk of system failures and ensure your team spends more time managing the portfolio and less time troubleshooting software bugs.

Automated Workflows: Eliminating the Human Error Factor

Manual processes are the primary source of compliance errors and operational delays. Automated workflows solve this by handling repetitive tasks with surgical precision. Workflow automation is the programmatic execution of standard operating procedures to ensure 100% policy adherence. By removing the human guess factor, you ensure that every borrower is treated according to your internal policies and federal regulations. This level of consistency is exactly what’s needed to scale a subprime portfolio safely in the current high-interest environment.

- Auto-Generated Notices: Late notices and payment reminders are sent based on real-time ledger data.

- Ledger Accuracy: Payments are updated across both the DMS and LMS simultaneously to prevent balance disputes.

- Compliance Roadmaps: Every loan follows a pre-set digital path that checks for required disclosures at every stage.

Protecting the Collateral: Real-Time Insurance Tracking & CPI

Insurance lapses represent the single greatest threat to a subprime auto portfolio. In a market where the average used vehicle loan amount has reached $27,528, a single total loss on an uninsured asset can wipe out the profit from dozens of performing loans. Traditional technology for auto finance companies often treated insurance as a secondary concern, relegated to manual spreadsheets and periodic phone calls to agents. This “call-and-pray” method is no longer viable in 2026. Real-time digital verification has replaced manual tracking, allowing lenders to see coverage status changes the moment they happen.

The evolution from manual to automated verification creates a proactive risk management environment. Modern systems connect directly to carrier data, flagging cancellations or non-renewals instantly. This immediate visibility prevents uninsured losses that can otherwise bankrupt a small or mid-sized portfolio. When you automate this process, you move from a reactive posture to one of absolute control. You no longer wait for a repossession or an accident to discover a lapse in coverage; you address the risk before the damage occurs.

Collateral Protection Insurance (CPI) serves as the ultimate safety net in this ecosystem. When a borrower fails to maintain the required coverage, CPI allows you to force-place insurance to protect your financial interest in the vehicle. This mechanism ensures that your collateral remains protected throughout the life of the loan, regardless of the borrower’s actions. It transforms a potential total loss into a manageable administrative event.

The ROI of Automated Insurance Verification

The financial impact of automation is immediate and measurable. By eliminating the need for a dedicated team to make manual follow-up calls, you significantly reduce your operational headcount. Beyond the payroll savings, there is a powerful psychological benefit. When borrowers receive an automated notification the moment their insurance flags, they realize you are actively monitoring the collateral. This awareness often encourages better payment behavior and higher compliance with loan terms. Protecting a $27,000 asset requires more than just hope; it requires a system that never blinks.

Collateral Protection Insurance (CPI) Best Practices

Success with CPI requires a delicate balance between risk mitigation and regulatory compliance. You must provide clear, automated borrower notifications before any insurance is added to the loan balance. This transparency reduces disputes and ensures you remain aligned with state-specific insurance regulations. Verifacto’s integrated Insurance Tracking and CPI solutions provide a seamless loop. The system identifies the lapse, sends the required notices, and places coverage only when necessary. This integrated approach ensures your portfolio stays protected without creating unnecessary friction for your borrowers.

Maximizing Recovery: Communication and Collection Technology

The days of relying solely on outbound phone calls to manage a subprime portfolio are over. In 2026, borrower behavior has shifted decisively toward digital-first interactions. Most consumers now ignore calls from unknown numbers, yet SMS messages boast open rates that far exceed any other medium. This shift in technology for auto finance companies isn’t just a matter of convenience; it’s a fundamental requirement for maintaining recovery rates. When you meet borrowers on the platforms they actually use, you reduce the friction that leads to missed payments and eventual defaults.

Implementing these tools requires a strict focus on legal compliance. Automated communication must align with TCPA and FDCPA regulations to protect your business from costly litigation. Modern platforms manage these complexities by tracking consent and time-of-day restrictions automatically. By leveraging automated payment reminders, you can drastically reduce “forgetfulness” defaults, which account for a significant portion of early-stage delinquencies. For a deeper look at advanced recovery tactics, review our guide on auto loan default management strategies for risk mitigation and recovery in the current high-delinquency environment.

The Power of Multi-Channel Communication

True mastery over collections comes from integrating email, SMS, and IVR into a single, cohesive communication thread. This multi-channel approach ensures that your message reaches the borrower through their preferred medium without creating redundant or conflicting touches. Providing a mobile-friendly borrower portal allows for self-service payment arrangements, giving customers the autonomy to resolve balances without a high-pressure phone call. This digital-first strategy reduces the professional anxiety of your collection teams, allowing them to focus on high-priority accounts that require a personal touch.

Integrated Payment Processing: Reducing Friction

Capturing a payment should never be difficult for the borrower. Utilizing integrated payment solutions for dealers allows you to accept payments 24/7, even when your office is closed. Whether you are processing ACH transfers or card payments, the goal is to balance borrower convenience with your internal processing costs. Encouraging auto-pay enrollment is one of the most effective ways to lower delinquency rates, as it removes the need for manual intervention from both parties. When payment processing is built directly into your LMS, the ledger updates instantly, eliminating the data discrepancies that often lead to borrower disputes.

Ready to modernize your outreach? Implement Automated Borrower Communication today to secure your revenue streams and improve recovery across your entire portfolio.

Future-Proofing Your Business: Choosing the Right Tech Partner

Selecting a partner to manage your portfolio is a high-stakes decision that impacts your stability for years. In a market projected to grow to $76.60 billion by 2026, your choice of technology for auto finance companies must prioritize mastery and stability over flashy, unproven features. You need a partner that understands the “no-nonsense” requirements of daily operations while providing the scalability to grow as your loan volume increases. A platform that feels cutting-edge today but lacks a roadmap for future regulatory changes will quickly become a liability.

During a demo, look past the user interface and ask hard questions about the underlying architecture. Focus on three critical areas: integration depth, data security, and support response times. You must know if the DMS and LMS are truly unified or just loosely connected through unstable patches. Verify how the provider handles sensitive borrower data and what kind of proactive assistance they offer when issues arise. Verifacto stands as the definitive solution for lenders who demand efficiency and protection without the corporate fluff. We provide the tools you need to navigate high-stakes environments safely and profitably.

Transitioning Without the Turmoil

Many lenders hesitate to modernize because they fear the data migration process. However, transitioning to a cloud based loan management system is often easier than anticipated when you have a partner that provides a clear roadmap. Successful migration starts with a structured data audit followed by proactive training for your team. Moving away from legacy systems eliminates the hardware maintenance burden and allows your staff to work securely from any location. We ensure that your historical data is preserved while your new workflows are optimized for 2026 standards.

Conclusion: Building a Resilient Auto Finance Company

The 2026 trend analysis makes one thing clear: integrated technology is no longer optional. To manage the rising risks in subprime portfolios and stay compliant with new regulations like the CARS Act, you must eliminate data silos. A unified tech stack that combines loan management, insurance tracking, and automated communication is the only way to maintain a competitive edge. It provides the “single source of truth” needed to make fast, accurate decisions that protect your capital.

Don’t let fragmented systems and manual errors stall your growth. Modernize your operations and secure your portfolio before your competitors do. Schedule your Verifacto demo today and see how our integrated DMS and LMS solutions can transform your business efficiency.

Modernize Your Operations for the 2026 Market

The transition from fragmented software silos to integrated ecosystems isn’t just a trend; it’s a fundamental survival strategy. By adopting unified technology for auto finance companies, you eliminate the manual errors that drain your profitability and leave your assets exposed. Throughout this analysis, we’ve explored how real-time insurance tracking and automated communication can transform a high-risk portfolio into a stable, predictable revenue stream. You now have the roadmap to move beyond reactive management and into a position of absolute operational control.

Don’t let legacy systems hold your business back while the rest of the industry moves forward. You need a partner that provides cloud-based LMS and DMS integration, real-time automated insurance tracking, and built-in compliant payment processing to handle the complexities of the 2026 landscape. Streamline your operations and protect your collateral with Verifacto; Book a Demo Today. It’s time to take command of your data and secure your portfolio with a solution built for long-term growth. We’re here to ensure your transition is seamless and your future is protected.

Frequently Asked Questions

What is the most important technology for auto finance companies in 2026?

The most important technology for auto finance companies in 2026 is the unified DMS/LMS ecosystem. These platforms eliminate data silos by connecting sales and servicing into a single source of truth. By centralizing operations, lenders can monitor portfolio health in real time and respond to risks like insurance lapses or payment delays before they lead to total losses.

How does integrated DMS and LMS software improve dealership profitability?

Integrated DMS and LMS software improves dealership profitability by eliminating redundant data entry and accelerating the funding process. When information flows seamlessly from the sales floor to the ledger, you reduce administrative overhead and minimize costly clerical errors. This efficiency allows your team to manage a larger volume of loans without increasing headcount or sacrificing data accuracy.

Can automated insurance tracking really reduce loan defaults?

Automated insurance tracking significantly reduces loan defaults by ensuring the collateral remains protected and the borrower stays compliant with loan terms. When a system identifies a coverage lapse instantly, it triggers automated reminders that prompt the borrower to act. This constant monitoring creates a culture of accountability that often translates into better overall payment behavior across the portfolio.

Is cloud-based auto finance software secure enough for sensitive borrower data?

Modern cloud-based technology for auto finance companies is typically more secure than legacy on-premise servers. These platforms use advanced encryption and regular security updates to protect sensitive borrower data against evolving cyber threats. Additionally, cloud systems simplify compliance with data privacy regulations by centralizing security protocols and providing detailed audit trails for every transaction.

What are the compliance risks of using automated borrower communication?

The primary compliance risks involve the Telephone Consumer Protection Act (TCPA) and the Fair Debt Collection Practices Act (FDCPA). Lenders must ensure they have proper consent for SMS messages and adhere to strict rules regarding the timing and frequency of contacts. Using a platform with built-in compliance guardrails helps mitigate these legal vulnerabilities by managing opt-outs and contact windows automatically.

How much does it cost to implement a modern auto loan management system?

Implementation costs for a modern auto loan management system vary based on your portfolio size, the number of users, and the specific features you require. Most vendors use a subscription-based model that scales with your business volume. You should request a custom quote to understand the total investment needed for your specific operational requirements and growth goals.

What is the difference between an LOS and an LMS in auto finance?

A Loan Origination System (LOS) handles the front-end process of credit application and approval. In contrast, a Loan Management System (LMS) manages the entire lifecycle of the loan after it’s funded, including payment processing and collections. While the LOS starts the relationship, the LMS is responsible for the long-term servicing and profitability of the account throughout its duration.

How does Collateral Protection Insurance (CPI) work within a DMS?

Collateral Protection Insurance (CPI) works as an automated safety net that triggers when a borrower’s primary insurance lapses. The system identifies the lack of coverage and automatically issues the required notices before force-placing a policy. This integration ensures that your financial interest in the vehicle is never left exposed to uninsured losses, even if the borrower fails to maintain their own policy.