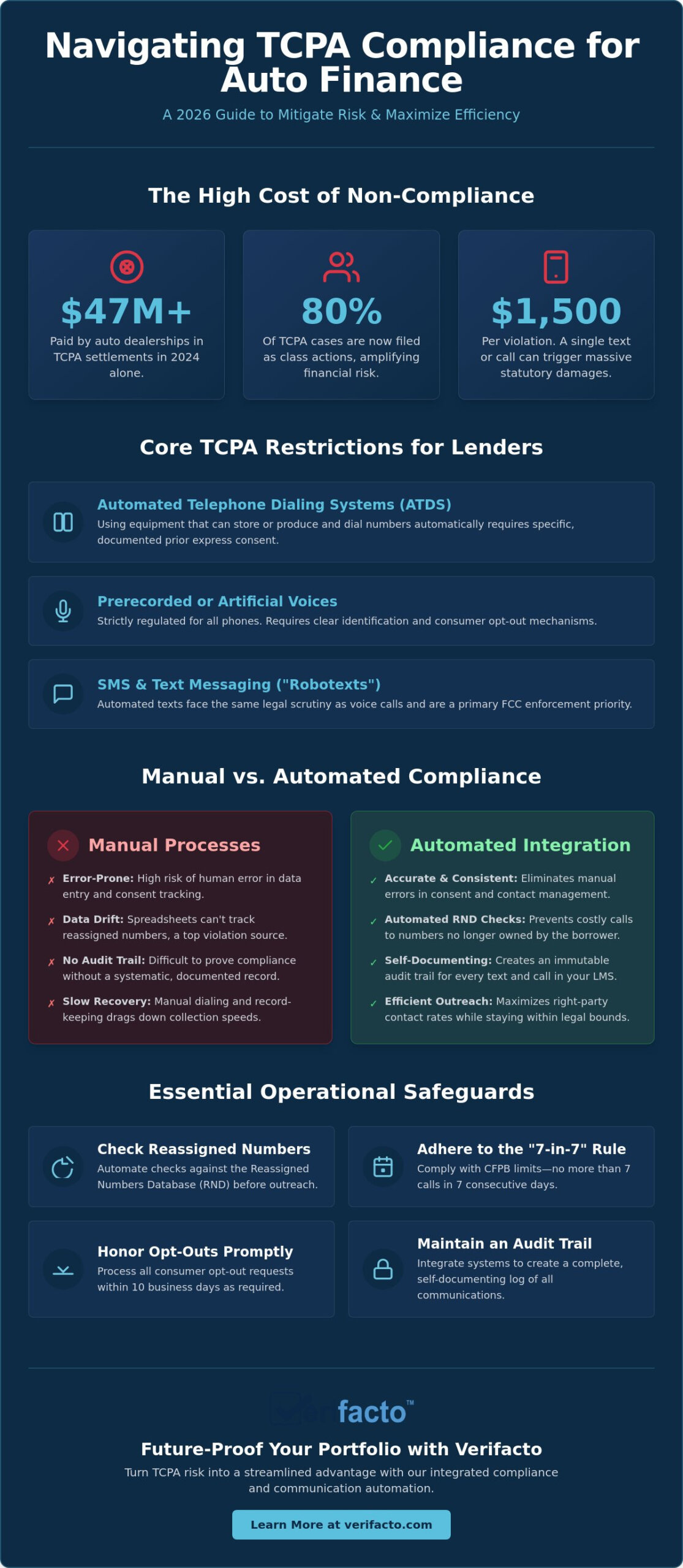

Did you know that automotive dealerships paid over $47 million in settlements for TCPA violations in 2024 alone? With nearly 80% of all cases now filed as class actions, a single oversight in your outreach strategy can escalate into a multi-million dollar liability overnight. Maintaining strict TCPA compliance for auto finance collections isn’t just a legal necessity; it’s a critical component of your operational stability through 2026.

You likely feel the mounting pressure of tracking consent across a massive loan portfolio while manual processes drag down your recovery speeds. It’s a high-stakes balancing act where a single text message can cost you up to $1,500 in statutory damages if your data has drifted. We’re here to help you turn that risk into a streamlined advantage. This article provides a clear roadmap to master the evolving regulatory landscape, ensuring you protect your assets while maximizing collection efficiency. We will examine how integrating automated borrower communication with your LMS eliminates manual errors, secures your audit trails, and drives higher right-party contact rates without the constant fear of litigation.

Key Takeaways

- Understand why auto lenders remain high-priority targets for class-action litigation and how the 2026 regulatory environment shifts the burden of proof.

- Master the “provision of number” doctrine to secure and document prior express consent as a cornerstone of your TCPA compliance for auto finance collections.

- Identify the hidden dangers of “data drift” and learn how automated Reassigned Numbers Database checks prevent costly errors that manual spreadsheets miss.

- Apply operational safeguards like the “7-7-7” rule to maintain high-velocity outreach while strictly adhering to anti-harassment standards.

- Discover how integrating automated borrower communication directly into your LMS creates a self-documenting audit trail for every text and call.

What is TCPA Compliance for Auto Finance in 2026?

The Telephone Consumer Protection Act (TCPA) remains the primary federal statute regulating how businesses communicate with consumers via phone and text. In 2026, TCPA compliance for auto finance collections has evolved into a complex framework where technical execution matters as much as legal intent. While the original law targeted telemarketers, the modern focus has shifted heavily toward automated debt collection and the technology used to facilitate it. You can’t afford to view these rules as mere suggestions; they’re the boundary lines for your entire recovery operation.

Auto lenders are high-priority targets for litigation because of the high frequency of borrower contact required during the loan lifecycle. Between payment reminders, insurance tracking notices, and late-stage collection calls, the sheer volume of outbound communication creates thousands of opportunities for a single technical error to trigger a lawsuit. Unlike general debt collection, auto finance often involves “right to cure” notices and specific state-level disclosures that must be delivered promptly, often tempting lenders to use high-speed automation that skirts compliance boundaries.

The core 2026 restrictions focus on three primary areas:

- Automated Telephone Dialing Systems (ATDS): Using equipment that can store or produce numbers and dial them automatically requires specific, documented consent.

- Prerecorded or Artificial Voices: These are strictly regulated for both landlines and cell phones, requiring clear identification and opt-out mechanisms.

- SMS and Text Messaging: The FCC now treats automated text messages with the same level of scrutiny as voice calls, making “robotexts” a major liability.

It’s vital to distinguish between telemarketing and informational calls. While informational calls, such as collection notices or repo warnings, often have slightly more flexibility than sales calls, they still require “prior express consent” if you’re using automated technology. You don’t have a free pass just because the borrower owes you money.

The 2026 Regulatory Landscape: FCC and CFPB Overlap

The FCC has intensified its focus on automated texting, treating these messages as a primary enforcement priority to protect consumers from unwanted disruptions. Simultaneously, the CFPB’s Debt Collection Rule (Regulation F) sets strict limits on how often you can contact a borrower about a debt. To stay safe, lenders must align their outreach with both agencies’ requirements, including the mandate to honor opt-out requests within 10 business days. The 2026 “One-to-One Consent” rule is now the gold standard for lead generation, requiring that a consumer’s consent applies only to a single specific seller rather than a broad list of “partners.”

The High Cost of Non-Compliance

The financial stakes are staggering. Negligent violations cost $500 per call or text, while willful violations jump to $1,500. For a lender sending automated reminders to a large portfolio, these fines multiply instantly across hundreds of accounts. You also face “vicarious liability” risks; if your third-party repossession agent or skip-tracer violates the TCPA while acting on your behalf, you’re often the one left holding the bill. This risk has fueled a rise in predatory class-action lawsuits targeting small to mid-sized lenders who lack the robust automated safeguards found in modern auto loan management software.

Securing Prior Express Consent in the Auto Loan Lifecycle

Consent isn’t a one-time box to check; it’s a continuous process that begins the moment a borrower walks into the dealership. In the context of TCPA compliance for auto finance collections, “Prior Express Consent” (PEC) means the borrower has explicitly agreed to receive communications at a specific number for account-related purposes. While the “provision of number” doctrine generally allows you to contact a borrower at a number they provided during the application process, relying on this alone is risky. If the borrower’s number changes or is reassigned to someone else, that implied consent doesn’t transfer to the new subscriber. For any communication that could be construed as marketing, you must obtain Prior Express Written Consent (PEWC), which requires a signed agreement with clear, conspicuous disclosures.

Digital loan applications have streamlined the process, but they introduce new requirements for documentation. The E-Sign Act ensures that electronic signatures hold the same legal weight as ink, provided you follow specific protocols. You must verify that borrowers have the technical capacity to access the electronic records they’re signing. Maintaining rigorous TCPA compliance for auto finance collections requires a system that links these digital signatures directly to the borrower’s profile, creating an immutable record of when and how consent was granted.

Capturing Consent at the Point of Sale

Your retail installment contract should include specific, prominent TCPA disclosure language that is easy for the borrower to read and understand. Avoid using pre-checked boxes; an opt-in must be a distinct, affirmative action taken by the borrower to be defensible in court. Don’t forget co-signers. Each person listed on the loan must provide individual consent to ensure your outreach remains protected. Documenting these consents at the point of sale prevents “he-said, she-said” disputes during the collection phase.

Managing Consent Revocation

Borrowers have the right to revoke consent at any time by any reasonable means. This isn’t limited to formal written requests; a simple “stop calling me” during a conversation or a “STOP” reply to an automated SMS is legally binding. Under rules that took effect on April 11, 2025, you must honor these requests within 10 business days. Following FCC guidance on robocalls ensures you respect consumer rights while protecting your portfolio from litigation. A centralized Do Not Call (DNC) list within your LMS is non-negotiable. It prevents manual errors where one department continues calling a number that another department has already marked as revoked. Implementing a modern loan management solution allows you to automate this revocation tracking, ensuring that “STOP” requests instantly update across your entire communication workflow.

Manual vs. Automated Compliance: Why Integration Wins

Relying on spreadsheets to manage TCPA compliance for auto finance collections is a recipe for disaster in 2026. Manual logs are prone to human error, lag behind real-time data, and offer zero protection during a legal audit. Transitioning to cloud-based auto loan management software replaces these fragile processes with hard-coded safeguards. Integration ensures that every call, text, and payment reminder is automatically time-stamped and logged. This creates a bulletproof audit trail that manual entries simply can’t match. When your communication tools “talk” to your ledger, you eliminate the risk of contacting a borrower who just made a payment or revoked consent five minutes ago.

The FCC’s “One-to-One Consent” rule has fundamentally changed lead generation and borrower outreach. You can no longer rely on broad consent shared across multiple “partners.” Consent must be specific to your entity. Automated systems manage these granular permissions at the account level. They ensure your collectors never dial a number that hasn’t cleared this high bar, protecting you from predatory class-action suits that exploit technicalities in consent chains.

The 2026 Efficiency Gap

Manual compliance isn’t just risky; it’s slow. Industry data suggests that manual compliance checks add 5 to 10 minutes to every collection call as agents verify consent dates and phone ownership. This creates a “hesitation factor” where collectors avoid making calls because they’re unsure of the legal standing. By improving collection efficiency auto loans through safe automation, you remove this friction. Automated borrower communication systems handle the background checks instantly. This allows your team to focus on recovery rather than research, significantly increasing your daily right-party contact rates.

Eliminating the “Wrong Number” Trap

The Reassigned Numbers Database (RND) is your most powerful defense against “wrong number” lawsuits. Remember, consent is tied to the person, not the device. If a borrower switches numbers and you call the new owner, you’re liable for up to $1,500 per violation. Integrated systems provide a legal safe harbor by automatically scrubbing your lists against the RND before every outreach attempt. When your DMS and LMS sync in real-time, you ensure that a number updated in one system is instantly verified or restricted across all platforms. This prevents “double-calling” and frequency violations that often occur when departments operate in silos, ensuring you stay well within the boundaries of the law.

Operationalizing TCPA Safety in Your Collection Workflow

Operationalizing TCPA safety requires moving beyond legal theory into daily practice. You must establish a “Compliance First” culture where every collector understands that protecting the portfolio is as important as the recovery itself. This starts with the “7-7-7” Rule, a standard derived from federal call frequency presumptions. You shouldn’t place more than seven calls to a borrower about a specific debt within seven consecutive days. Once you’ve had a conversation, you must wait another seven days before calling again. Managing this manually is nearly impossible in a high-volume environment, but an integrated system handles these countdowns automatically, preventing accidental over-dialing.

SMS communication requires even tighter controls to stay safe. Every text must include a clear opt-out notice, such as “Reply STOP to end,” and stay within character limits to avoid being broken into multiple, potentially harassing messages. Timing is also critical; you must only send messages during “reasonable” hours, typically between 8 a.m. and 9 p.m. in the borrower’s time zone. For non-urgent notices, email often serves as a safer, less intrusive alternative to SMS. While TCPA doesn’t govern email, it helps you maintain TCPA compliance for auto finance collections by shifting high-frequency, non-urgent updates away from the borrower’s phone line. This reduces the perceived “harassment” that often triggers litigation.

TCPA and Collateral Protection Insurance (CPI)

Communicating about insurance lapses is a high-risk area that requires precise execution. You need to know what is collateral protection insurance and how to discuss it without violating outreach rules. When a borrower’s policy expires, your system should use automated triggers to send verification notices. This ensures you’re balancing the “Right to Cure” with TCPA contact restrictions. By automating these triggers within your LMS, you ensure that every insurance-related touchpoint is documented and compliant, reducing the risk of a borrower claiming harassment during a collateral dispute.

Staff Training and Audit Trails

Your collectors are your first line of defense. Every call must be recorded for quality and compliance auditing, providing an objective record if a dispute arises. Use a 2026 auto finance compliance management checklist to regularly spot gaps in your workflow and keep your team sharp. One critical area for training is the use of “Limited-Content Messages” (LCM) for voicemails. An LCM is a specific type of message that doesn’t disclose the existence of a debt to third parties. It contains only your business name, a request for the borrower to call back, and a contact name. Mastering these small details locks down your communication strategy and keeps you out of court.

Protect your portfolio with the industry’s most reliable automation tools. Discover how Verifacto builds compliance into every collection workflow.

Future-Proofing Your Portfolio with Verifacto Automation

Achieving total TCPA compliance for auto finance collections shouldn’t feel like a constant defensive battle. It’s about building a foundation where protection is automatic and recovery is seamless. Verifacto’s integrated DMS/LMS platform transforms compliance from a manual checklist into a hard-coded operational standard. By syncing your dealership management and loan servicing data in real-time, the platform ensures that every communication attempt is backed by verified consent and accurate borrower information. This integration eliminates the data silos that often lead to accidental violations, positioning Verifacto as the reliable guardian of your lending operations.

Beyond simple record-keeping, the platform acts as a secondary layer of risk mitigation through real-time insurance monitoring. When you can track collateral protection status 24/7, you reduce the need for aggressive, high-risk collection tactics. You gain the stability of knowing your assets are protected while your communication remains within legal boundaries. This proactive approach allows you to focus on growth rather than damage control.

Verifacto Automated Borrower Communication

Verifacto’s compliant notification engine offers a “set it and forget it” solution for modern lenders. The system handles the heavy lifting of consent tracking and opt-out management without requiring manual intervention from your staff. If a borrower replies “STOP” to a text message, the platform instantly updates the account across all modules, ensuring no further automated messages are sent. This level of precision is vital for maintaining TCPA compliance for auto finance collections in a high-velocity environment. Additionally, the use of integrated payment solutions for dealers reduces the overall need for collection calls. When borrowers can easily manage their own payments through automated reminders, your team spends less time on the phone and more time on high-value tasks.

Cloud-Based Security and Scalability

Cloud-based systems provide a level of security and scalability that legacy on-premise software can’t match. Whether you operate a single lot or manage a multi-state portfolio, Verifacto maintains a centralized, immutable audit trail for every interaction. This ensures that your compliance documentation is always ready for a sudden audit or legal challenge. The platform’s 24/7 real-time insurance tracking provides a constant pulse on your collateral, triggering automated, compliant notices the moment a lapse is detected. You don’t have to wait for a manual report to take action. This speed and accuracy are what define a modern, future-proofed lending strategy.

Don’t leave your portfolio’s safety to chance. Contact Verifacto today for a platform demo and see how our automation tools can secure your operations through 2026 and beyond.

Securing Your Portfolio for the 2026 Regulatory Shift

Mastering TCPA compliance for auto finance collections is no longer a defensive burden; it’s a strategic pillar of a modern lending operation. By moving away from fragmented spreadsheets and manual logs, you eliminate the human errors that lead to multi-million dollar settlements. We’ve explored how integrating your DMS and LMS creates a self-documenting ecosystem that handles consent revocation and call frequency limits automatically. This transition ensures that your recovery efforts remain high-velocity without crossing legal boundaries.

Verifacto provides the tools you need to maintain 100% collateral visibility while staying protected. Our platform features built-in TCPA-compliant communication tools and real-time insurance tracking, ensuring you always have the data required for safe outreach. You don’t have to choose between collection efficiency and legal security. A seamlessly integrated LMS and DMS platform gives you the control necessary to navigate 2026 with confidence.

Automate your compliance and streamline your collections with Verifacto today. Take decisive action now to build a more resilient, profitable, and litigation-proof future for your lending business.

Frequently Asked Questions

Does the TCPA apply to text messages in 2026?

Yes, the TCPA applies to text messages with the same legal weight as voice calls. The FCC treats automated “robotexts” as a high-priority enforcement area, meaning every text sent to a borrower requires documented consent. If you use automation to send payment reminders or insurance notices via SMS, you must ensure your system tracks opt-outs in real-time. Failing to honor a “STOP” request immediately can lead to significant statutory damages for each message sent.

What is the difference between express consent and express written consent for auto lenders?

Prior express consent (PEC) is generally sufficient for informational or servicing calls, such as notifying a borrower about a late payment or an insurance lapse. However, prior express written consent (PEWC) is a stricter standard required for any communication that includes marketing or promotional offers. PEWC requires a signed agreement with clear, conspicuous disclosures that the borrower agrees to receive automated sales messages. You don’t have the right to use servicing consent to justify marketing outreach.

How many times can I call a borrower about a late payment under the 7-7-7 rule?

You can place up to seven calls regarding a specific debt within a seven-day period. Once you successfully speak with the borrower, you must wait another seven days before placing another call about that same debt. This rule helps prevent harassment claims and ensures your outreach remains within the “presumption of compliance” established by federal debt collection standards. Tracking these windows manually is difficult, so lenders often use an LMS to automate these frequency caps.

Can I use an automated dialer for “informational” debt collection calls?

You can use an automated dialer for informational calls, but you must have prior express consent to stay within TCPA compliance for auto finance collections. Consent is usually established when a borrower provides their phone number on a credit application. However, you should still verify that the number belongs to the borrower before every automated blast. If you dial a number without verified consent, you risk statutory damages of up to $1,500 per willful violation.

What is a “limited-content message” and how does it help with TCPA compliance?

A limited-content message is a specific voicemail format that avoids disclosing the existence of a debt to anyone who might overhear it. It typically includes only your business name, a request for a return call, and a contact name. Using this format protects you from third-party disclosure violations under the FDCPA while still allowing you to maintain a consistent outreach cadence. It’s a vital tool for collectors who need to leave messages without triggering privacy-related lawsuits.

How does the FCC’s one-to-one consent rule affect auto dealers?

The one-to-one consent rule requires that a consumer’s agreement to be contacted applies only to a single, specific seller. You can no longer rely on “partner lists” where a borrower’s consent is shared across dozens of different entities. This rule forces lenders to capture direct, individual consent during the lead generation or loan application process. It ensures that when you call or text a borrower, you have a direct and documented legal right to do so.

Are repo agents required to follow TCPA regulations when contacting borrowers?

Yes, repossession agents are strictly required to follow TCPA regulations when they use automated technology to contact borrowers. As the lender, you face significant vicarious liability risk if your third-party vendors violate these rules. You must ensure your agents use compliant communication tools and maintain their own audit trails. Managing these relationships through a centralized platform allows you to monitor vendor activity and ensure they don’t expose your portfolio to unnecessary legal risks.

What happens if I call a number that has been reassigned to a new person?

Calling a reassigned number is a major violation that can result in fines of $500 to $1,500 per call. Because consent is tied to the person and not the device, your original permission disappears the moment the number is transferred. Maintaining TCPA compliance for auto finance collections requires using an automated system that scrubs your contact lists against the Reassigned Numbers Database (RND). This check provides a legal safe harbor and prevents you from accidentally contacting a stranger.