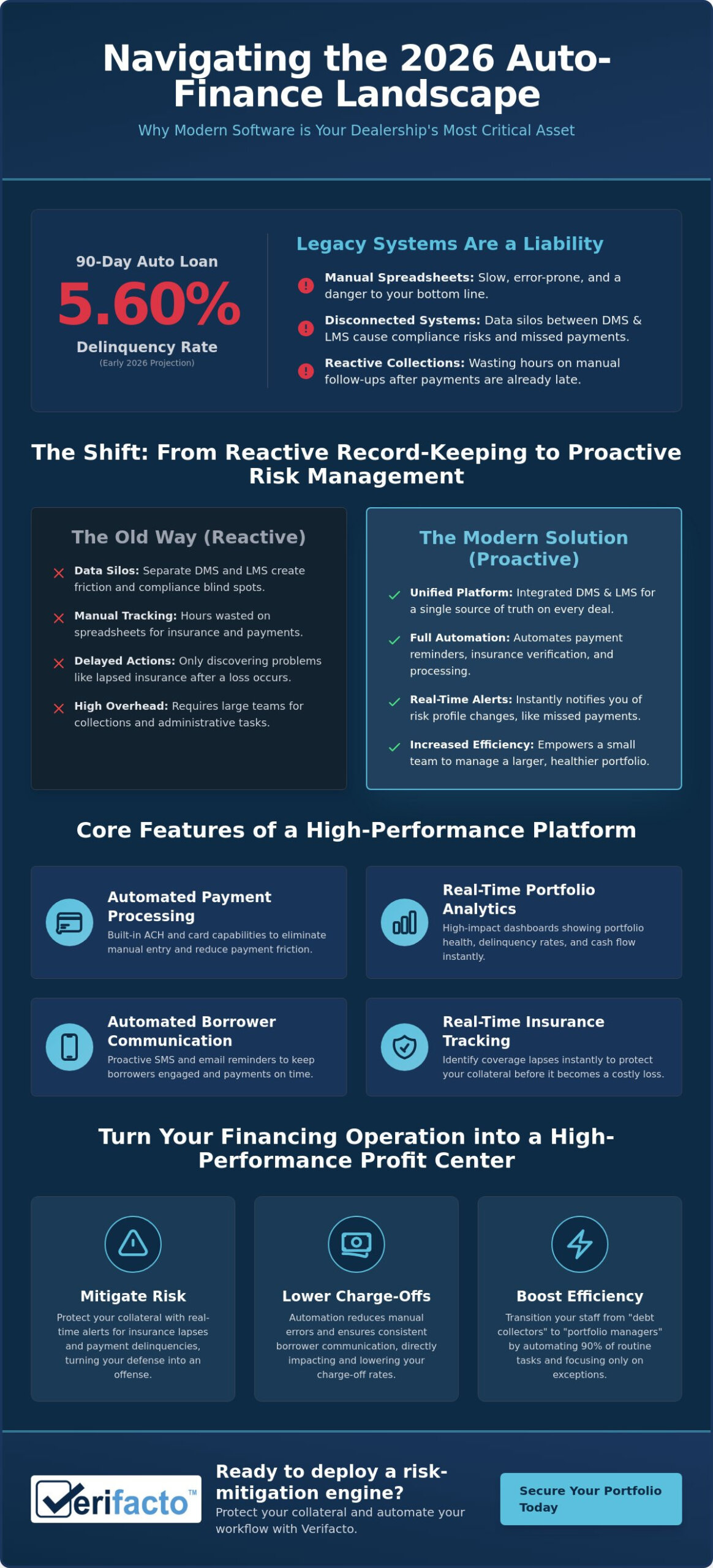

With the 90-day auto loan delinquency rate hitting 5.60% in early 2026, the margin for error in your portfolio is thinner than ever. You already know that manual spreadsheets and disconnected systems aren’t just slow; they’re dangerous to your bottom line. Selecting the modern software for in-house financing car lots is no longer about finding a simple digital ledger. It’s about deploying a risk-mitigation engine that protects your collateral and automates your workflow before a loss occurs.

It’s exhausting to lose track of borrower insurance coverage or waste hours on manual payment processing while subprime delinquency rates climb. You need a solution that alleviates compliance anxiety and provides total control over your assets. This guide will help you discover how to select the right in-house financing software to automate collections, track insurance in real-time, and protect your BHPH portfolio from rising industry risks.

We’ll explore the critical shift toward cloud-based systems that bridge the gap between your DMS and LMS. You’ll learn how to leverage automated borrower communication and real-time verification to lower charge-off rates and turn your financing operation into a streamlined, high-performance machine.

Key Takeaways

- Modern software for in-house financing car lots must unify DMS and LMS functions to eliminate data lag and operational friction across your entire dealership.

- Real-time insurance tracking is the most effective way to protect your collateral by identifying coverage lapses before they become costly losses.

- Automation in payment processing and borrower communication reduces manual errors and helps lower charge-off rates by maintaining consistent contact.

- Cloud-based platforms provide the agility needed for 2026, offering secure access to portfolio analytics and compliance tools from any location.

- Shifting from legacy systems to a proactive risk-management engine turns your financing operation into a high-performance, results-oriented profit center.

The Shift in Software for In-House Financing Car Lots

The landscape of auto finance has changed. In 2026, relying on legacy desktop systems is a liability. Modern software for in-house financing car lots must be a unified platform that merges Dealer Management Systems (DMS) with Loan Management Systems (LMS). This shift isn’t just about moving to the cloud; it’s about moving from reactive record-keeping to proactive risk management. You need a system that doesn’t just store data but actually uses it to protect your investment.

The in-house financing business model relies on liquidity and collateral protection. When your data is trapped in manual spreadsheets or outdated local servers, you’re flying blind. Manual tracking is the number one threat to your dealership’s liquidity because it creates delays in recognizing delinquency and insurance lapses. In a market where 90-day delinquency rates have hit 5.60%, speed is your only defense. Data-driven decision making is no longer a luxury for big banks; it’s a survival requirement for every independent lot.

LMS vs. DMS: Why You Need Both Integrated

A Dealer Management System (DMS) handles the front-end operations like inventory management, sales contracting, and initial deal structure. It’s the engine that drives your sales floor. A Loan Management System (LMS) manages the back-end, focusing on payment processing, borrower communication, and collections. Most dealerships treat these as two separate worlds, but that’s a mistake that costs money.

Data silos between these systems lead to compliance errors and missed opportunities. If your LMS doesn’t know what your DMS promised in the contract, or if your DMS doesn’t reflect the current payment status from the LMS, you risk violating state usury laws or federal transparency regulations. Integrated software ensures that a single source of truth exists for every vehicle and every borrower, reducing the friction that typically leads to missed payments.

The Role of Automation in Modern BHPH

Automation is the great equalizer for independent lots. It replaces the need for massive, expensive collection departments by handling routine tasks like payment reminders and insurance verification. Instead of reacting to a missed payment two weeks late, automated systems alert you the moment a risk profile changes. This allows your team to focus on the high-risk accounts that actually require a human touch. Proactive management turns a struggling portfolio into a predictable revenue stream.

This shift allows you to manage a larger portfolio with a smaller, more focused team. You can transition your staff from “debt collectors” to “portfolio managers” who handle high-value exceptions while the software manages the rest. Integrated auto finance software is the backbone of dealership scalability.

Core Features of High-Performance In-House Financing Software

High-performance software for in-house financing car lots goes beyond basic record-keeping. It acts as a digital guardian for your assets. In a climate where subprime 60-day delinquency rates reached 5.49% in May 2026, you can’t afford to wait for a borrower to call you. You need a system that initiates contact, processes payments automatically, and provides an instant health check of your entire portfolio. These tools allow you to move from a defensive posture to a strategy of proactive growth.

The right platform transforms your daily operations by focusing on four critical pillars:

- Automated Payment Processing: Built-in ACH and credit card capabilities that eliminate manual data entry and human error.

- Real-Time Analytics: High-impact dashboards that show you exactly where your money is at any given second.

- Automated Communication: SMS and email reminders that keep your dealership top-of-mind for borrowers before a payment is missed.

- E-Contracting: Secure, paperless document management that speeds up the closing process and reduces physical storage costs.

Streamlining Payments and Collections

Friction is the enemy of a healthy BHPH portfolio. If it’s difficult for a borrower to pay, they won’t. This is why integrated payment solutions for dealers are essential for modern operations. By scheduling recurring payments, you stabilize your monthly cash flow and remove the forgetfulness factor that often leads to early-stage delinquency. A self-service borrower portal provides 24/7 access, allowing your customers to settle their accounts on their own schedule without tying up your staff on the phone. This level of convenience isn’t just a perk; it’s a proven method for lowering charge-off rates.

Compliance and Reporting

Regulatory scrutiny is intensifying across the country. In March 2026, the FTC issued warning letters to 97 dealer groups regarding price transparency and mandatory fees. Your software must include robust tools for auto finance compliance management to ensure you’re meeting all current federal consumer protection regulations. High-performance systems automate Metro 2 reporting to credit bureaus and generate audit-ready reports for state examiners. When your software handles the technical details of Regulation Z and Regulation B, you can focus on scaling your business with confidence. If you’re ready to see these features in action, consider streamlining your workflow with Verifacto to secure your dealership’s long-term stability.

Mitigating Risk with Insurance Tracking and CPI

Uninsured collateral is the single biggest hidden cost for in-house lenders. While delinquency is a visible problem, a total loss on an uninsured vehicle represents a permanent hit to your dealership’s liquidity. High-performance software for in-house financing car lots must address this vulnerability directly. Research indicates that Buy Here Pay Here loans are 16.63 times more likely to be in active repossession status than traditional loans. If those vehicles aren’t protected by a valid insurance policy, your portfolio is exposed to catastrophic risk that can’t be recovered.

Real-Time Insurance Verification

Calling insurance agents once a month is an obsolete and dangerous practice. In the time it takes for your staff to cycle through a list of phone calls, a borrower could cancel their policy or let it lapse, leaving you with zero protection for weeks at a time. Modern auto loan management software monitors coverage 24/7 by integrating directly with insurance carrier databases. This technology reduces the “gap time” from weeks to hours. When a policy is canceled, the system knows instantly and can automatically trigger borrower notices via text or email, demanding immediate proof of new coverage before the vehicle leaves the driveway.

Automating Collateral Protection Insurance (CPI)

When a borrower fails to maintain their own policy despite multiple reminders, you need a reliable safety net. Understanding what is collateral protection insurance is key to maintaining your dealership’s financial health. CPI allows you to force-place coverage on a vehicle to protect your lienholder interest. This process isn’t just about protection; it’s about staying within the lines of the law. You must navigate the FTC’s Motor Vehicle Dealers Trade Regulation Rule, which demands transparency regarding add-on products and financing terms.

Advanced software for in-house financing car lots automates the entire CPI workflow from start to finish. It identifies the lapse, sends the required legal notices, and adds the premium to the borrower’s account balance without manual intervention. This ensures you remain compliant with state regulations while keeping your collateral secure. By removing the human element from insurance tracking, you eliminate the risk of oversight and ensure every asset in your portfolio is backed by a financial guarantee. It’s a proactive approach that turns a major vulnerability into a managed operational standard.

Evaluating ROI: How Automation Reduces Charge-Offs

Many dealers view technology as a monthly expense. This perspective is a mistake. High-performance software for in-house financing car lots is actually a revenue protector that pays for itself by preventing the losses that sink a dealership. When you consider that BHPH loans are nearly 17 times more likely to be in active repossession status than traditional loans, the cost of the software is negligible compared to the cost of a single unrecovered vehicle. By automating the most labor-intensive parts of your business, you shift your resources from chasing debt to growing your portfolio.

The real ROI of automation isn’t just found in what you gain; it’s found in what you don’t lose. Charge-offs and repossessions are the silent killers of dealership liquidity. Every time a car is towed back to the lot, you lose the remaining interest, the mechanical value of the asset, and the cost of the recovery itself. Early intervention through automated systems stops this cycle before it starts. It turns your financing operation from a defensive cost center into a high-performance profit engine.

Calculating the Cost of Manual Collections

Manual collections are a drain on your dealership’s most valuable resource: time. A staff member might spend 40 hours a week making manual phone calls, leaving voicemails that are never returned, and documenting notes in legacy systems. Automated SMS payment reminders do this work in seconds with a much higher response rate from modern borrowers who prefer text over talk. Legacy DMS systems often suffer from high error rates due to manual data entry, leading to missed payments and compliance headaches that require even more time to fix. Every hour saved on admin is an hour spent on selling more inventory.

Reducing Default Rates Through Better Communication

Subprime borrowers often juggle multiple financial obligations simultaneously. Your loan needs to stay “top of mind” to ensure it gets paid first. Automated borrower communication systems provide gentle, consistent nudges that feel less confrontational than a traditional collection call. This psychological shift is powerful. It maintains a positive relationship with the customer while securing the payment through consistent, professional contact.

By improving collection efficiency auto loans, you directly impact your bottom line. Dealers often see a 20-30% reduction in delinquency after switching from disconnected tools to an integrated LMS. This reduction in early-stage delinquency prevents the “snowball effect” that leads to full defaults and expensive repossession fees. If you’re ready to see how these efficiencies can protect your specific portfolio, explore how Verifacto automates your risk management to secure your dealership’s future.

Why Verifacto is the Modern Solution for In-House Financing

Verifacto isn’t just a digital filing cabinet. It’s a sophisticated risk-management engine designed for the high-stakes environment of 2026. While other platforms offer basic accounting, Verifacto DMS and Verifacto LMS provide a unified, cloud-based solution that prioritizes the security of your capital. Selecting the best software for in-house financing car lots requires looking beyond the sales contract to the long-term health of the loan. Our platform is built on a no-nonsense philosophy that removes technical friction so you can focus on moving inventory and scaling your operations.

Our approach is grounded in the reality that manual processes are the primary cause of portfolio leakage. By integrating payment processing directly into the system, we eliminate the data lag that often leads to missed collection opportunities. We provide a partner-like reassurance by delivering the tools you need to maintain total control over your portfolio from any location. This isn’t just about modernization; it’s about building a business that is resilient to market fluctuations and rising delinquency rates.

The Verifacto Advantage: Insurance-Centric Lending

We believe that a loan is only as good as the collateral behind it. Verifacto closes the loop between loan servicing and collateral protection by integrating real-time insurance tracking directly into your daily workflow. This isn’t a secondary feature; it’s the core of our “reliable guardian” approach. Our system acts as a constant watchman, using automated borrower communication to handle the heavy lifting of collections and insurance proof requests. When a policy lapses, the system reacts instantly, protecting your assets while your team focuses on high-value tasks. This proactive stance ensures that your software for in-house financing car lots is working as hard as you are to prevent losses.

Ready to Modernize Your In-House Financing?

The shift to cloud-based, integrated systems is no longer optional for dealers who want to stay competitive. If your current process involves manual spreadsheets or calling agents to verify coverage, you’re carrying hidden risks that jeopardize your liquidity. It’s time to audit your current operations and see where the gaps are. Switching to a unified platform reduces administrative overhead and provides the real-time data needed to survive in a high-delinquency environment. Schedule your Verifacto demo today to secure your portfolio and transform your dealership into a modernized, risk-resistant profit center.

Secure Your Portfolio and Scale with Confidence

The auto finance industry in 2026 demands a shift from reactive collections to proactive risk management. Success now depends on your ability to unify sales data with loan servicing while maintaining a constant watch over your collateral. You’ve learned that automation isn’t just a convenience; it’s a fundamental shield against the rising delinquency rates currently impacting the market. Choosing the right software for in-house financing car lots is the difference between struggling with manual errors and running a high-performance profit engine.

Verifacto stands as your reliable guardian in this high-stakes environment. Our platform delivers real-time insurance tracking integrated alongside automated CPI solutions to ensure your assets are never left vulnerable. With cloud-based accessibility, you can manage your portfolio with precision from any location, regardless of scale. It’s time to eliminate compliance anxiety and take full control of your dealership’s financial future.

Don’t let uninsured losses or manual inefficiencies hold your business back. Request a Demo of the Verifacto LMS & DMS Platform today to see our results-oriented technology in action. You’ve built a strong foundation, and we’re here to help you protect it and grow.

Frequently Asked Questions

What is the difference between DMS and LMS for car lots?

A Dealer Management System (DMS) focuses on the front-end of your business, managing inventory, sales, and initial contracting. A Loan Management System (LMS) handles the back-end servicing, including payment processing, borrower communication, and collections. Modern software for in-house financing car lots should unify these two systems into a single platform to eliminate data silos and prevent compliance errors that occur when information is manually transferred between disconnected tools.

How does insurance tracking software work for auto lenders?

Real-time insurance tracking software integrates directly with carrier databases to monitor policy status 24/7. Instead of relying on your staff to make manual phone calls to agents, the system receives an instant notification the moment a policy is canceled or lapses. This immediate feedback allows the software to trigger automated notices to the borrower, significantly reducing the dangerous window of time where your collateral is unprotected on the road.

Is cloud-based software safe for storing borrower financial data?

Cloud-based platforms utilize advanced encryption and secure data centers that typically exceed the security capabilities of local dealership servers. These systems provide automated backups and real-time security updates, ensuring your borrower data is protected against physical hardware failure or localized cyber threats. This modern approach gives you secure, authorized access to your portfolio from any location without compromising the integrity of sensitive financial information.

Can I integrate my existing payment processor with in-house financing software?

Most modern software for in-house financing car lots offers built-in payment processing to ensure seamless data flow, though many platforms can integrate with external providers. Using an integrated solution is generally recommended because it automatically updates loan balances and payment histories without any manual entry. This reduces human error and ensures your records are always audit-ready, providing a clear trail for every transaction in your portfolio.

How does automated borrower communication improve collections?

Automated communication improves collections by providing consistent, professional nudges via text and email before a payment is actually missed. These reminders keep the loan top of mind for subprime borrowers who are often managing multiple financial obligations simultaneously. By removing the friction and confrontation of manual phone calls, your team can focus on resolving high-risk accounts while the software handles the routine follow-ups that maintain steady cash flow.

What is Collateral Protection Insurance (CPI) and do I need it?

Collateral Protection Insurance (CPI) is a safety net that protects your lienholder interest when a borrower fails to maintain their own full-coverage insurance. You need it because it ensures your capital remains protected even if a borrower lets their policy lapse. High-performance software can automatically force-place this coverage according to state regulations, safeguarding your portfolio from total losses after an accident or theft occurs.

Will this software help with Metro 2 credit bureau reporting?

High-performance financing software automates the generation and submission of Metro 2 files to the major credit bureaus. This eliminates the need for manual data entry and ensures your reporting remains consistent and compliant with federal transparency regulations. Accurate credit reporting is essential for maintaining a professional operation and provides a powerful incentive for borrowers to prioritize their payments to your dealership.

How long does it take to migrate data from a legacy BHPH system?

Data migration timelines vary based on the complexity of your current records, but most transitions are completed within a few days to a few weeks. A professional software provider handles the heavy lifting by mapping your existing borrower and inventory data into the new system to ensure a smooth transition. This process is designed to minimize operational downtime so your daily sales and collection activities continue without interruption.